Wall Street’s Foolish War on Passive Investing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

This article originally appeared on ETF.COM here.

Wall Street has ridiculed passive investing for decades. The reason is obvious: Its profits – and for many firms, their very survival – are at stake. The criticism reached an absurd level when a team at Bernstein called passive investing “worse than Marxism.” The authors of the note wrote: “A supposedly capitalist economy where the only investment is passive is worse than either a centrally planned economy or an economy with active market led capital management.”

Another example of such criticism was an article titled “What They Don’t Tell You About Passive Investing.” Produced by Morgan Stanley, the thrust of the paper was that “the exodus from active to passive funds may be reaching bubble-like proportions, driven by an exaggerated critique of active management.”

The basic argument of these and other critiques is that the popularity of indexing (and the broader category of passive investing) is distorting prices as fewer shares are traded by investors performing the act of “price discovery.” Let’s examine the validity of such claims.

Before doing so, it’s worth noting the irony that if indexing’s popularity was actually distorting prices, active managers should be cheering, not ranting against its use, as it would provide them easy pickings, allowing them to outperform. (Note that if money flowing into passive funds distorts prices, it could still make it difficult for active managers while it is occurring, as distortions could persist as long as the flow continued. Eventually, though, the opportunity would manifest itself.) In reality, the rise of indexing has coincided with a dramatic fall in the percentage of active managers outperforming on a risk-adjusted basis.

Supporting research on manager skill

The study “Conviction in Equity Investing” by Mike Sebastian and Sudhakar Attaluri, which appeared in the Summer 2014 issue of The Journal of Portfolio Management, found that the percentage of skilled managers was about 20% in 1993. By 2011, it had fallen to just 1.6%. This closely matches the result of the 2010 paper “Luck versus Skill in the Cross-Section of Mutual Fund Returns.” The authors, Eugene Fama and Kenneth French, found only managers in the 98th and 99th percentiles showed evidence of statistically significant skill. On an after-tax basis, that 2% would be even lower.

In our book, “The Incredible Shrinking Alpha,” Andrew Berkin and I present evidence, as well as the reasons, for the dramatic decrease in active investors’ outperformance on a risk-adjusted basis.

In addition to the evidence on the failure of active management to persistently generate risk-adjusted alpha, it’s easy to check whether increased flows to index funds are causing price distortions. If that were the case, all securities in an index would be rising/falling by about the same percentages, as cash is invested based purely on market capitalization.

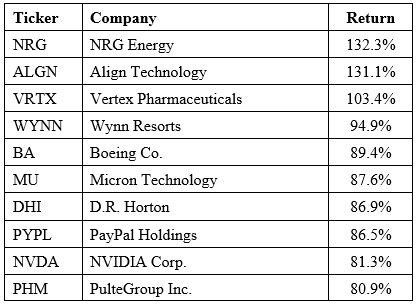

As I pointed out in my annual look at lessons the markets teach investors, the S&P 500 Index returned 21.8% in 2017, including dividends. In terms of price-only returns, 182 of the 500 stocks were up more than 25%, 49 were up at least 50%, 10 were up at least 80.9%, and three more than doubled in value. The following table shows the 10 best returners:

On the other hand, 125 stocks within the index, on a price-only basis, were down for the year; 59 lost at least 10%, 20 were down at least 25% and the 10 largest losers (see the following table) lost at least 44.2%:

Another example that demonstrates the exaggerated claims about passive investing’s effect is the year-to-date returns of Amazon (AMZN) and General Electric (GE), both of which are in the S&P 500 Index. Through May 1, AMZN had risen 34%, while GE had fallen 18%. If passive investing were driving prices and destroying the price discovery function, we would not have seen such wide disparity in returns. Clearly, active investors engaged in price discovery are still trading, and their activity must be what is setting prices.

One final example. Every day on cable financial news networks, we observe how stock prices jump (decline) immediately after companies announce better-than-expected (worse-than-expected) earnings. Because index funds do not trade at all on earnings announcements, it must be the price discovery actions of active investors moving prices, correcting the prior prices to account for the new information. Just how quickly prices adjust is testament to the market’s efficiency.

How much activity is enough?

While no one knows exactly how much active security selection is needed to assure markets are efficient (that is, providing the best estimate of the “right” price), it doesn’t take all that much activity to ensure that is the case. Consider that, 60 years ago, there were less than 100 mutual funds, and just a small number of hedge funds. Yet markets were pretty efficient, as the first studies on the performance of active managers showed. At that time, trading volume was a small fraction of what it is today.

More than 40 years ago, Richard Posner, a leading figure in the field of law and economics, contemplated the question of how much activity is needed to keep markets efficient.

In an article co-authored with John Langbein, “Market Funds and Trust-Investment Law II,” which was published in the American Bar Foundation Research Journal, he wrote: “No one knows just how much stock picking is necessary in order to assure an efficient market, but comparisons with other markets suggest that the required amount is small. In markets for consumer durables, homes and other products, unlike the securities markets, the amount of search is highly variable across consumers, many of whom do little or none; trading may not be frequent; products may not be homogenous (no two homes are as alike as all the shares of the same common stock); bids and offers may not be centrally pooled so as to maximize the information available to buyers and sellers. Yet these markets are reasonably efficient, albeit less so than the securities markets.”

Although Posner didn’t hypothesize exactly how much active management is necessary to make prices fair, it’s likely far less than what we currently observe in markets. Why? Consider an auction for art with 1,000 unsophisticated participants and just two sophisticated art historians bidding on behalf of wealthy individuals. Will the two sophisticates be able to buy a Picasso at a cheap price because there are so many unsophisticated buyers? Or, is it more likely that the two experts will engage in a bidding war and set the price at a fair market value? You don’t need many experts to set prices efficiently.

In this example, it’s also possible that one of the 1,000 unsophisticated participants could bid well over what a Picasso was worth and the two sophisticates would not be able to keep this particular market efficient.

Anomalies persist

However, in the stock market, sophisticated investors can short stocks, driving their prices to the “correct” level. With that said, we also know arbitrage limits prevent sophisticated investors from fully correcting prices, allowing some anomalies to persist even after discovery. Yet despite the existence of these anomalies, active management remains a loser’s game.

Economic theory suggests the marginal cost of searching for mispriced securities should equal the marginal profit associated with exploiting pricing errors. Thus, if assets invested in index funds increase to the point where mispricing becomes easy to identify and profit from, then active investors would re-enter the market until the marginal benefit of active investing once again does not exceed the marginal cost.

In addition to the price discovery activities of active investors, issuers of stock play an important role in maintaining market equilibrium/efficiency. If companies believe their stock is too highly valued, they can issue more shares because capital is cheap. Recall the late 1990s. When companies believe their stock is undervalued, they can engage in stock buybacks.

Winner’s game: Passive investing

One reason passive management is the winning strategy is that markets are efficient at processing information, making it difficult to gain a competitive advantage. Active managers also bear the burden of the greater costs they incur in the pursuit of outperformance: operating expenses, transaction costs, market impact costs, the drag of low returns on cash holdings and, for taxable accounts, taxes. That’s John Bogle’s “costs matter” hypothesis.

With the historical evidence supporting the view that active management is the loser’s game, the trend to passive management among individuals and institutional investors has not only been growing, the pace has accelerated. In light of this, I am often asked: What would happen if everyone indexed?

First, we are a long way from that happening, with perhaps 40% of institutional assets and nearly 20% of individual assets invested in passive strategies. Second, there will always be some trading activity from the exercise of stock options, estates, mergers and acquisitions and, as previously mentioned, from new issuance and buybacks, cash flow needs of investors and so on.

With that in mind, let’s address the issue of the likelihood of active managers either gaining or losing an advantage as the trend toward passive management marches on.

Let’s first tackle the issue of information efficiency. With less active management activity, there would be fewer professionals researching and recommending securities. Active management proponents argue it would be easier to gain a competitive advantage. This is the same argument they currently make about “inefficient” small-cap and emerging markets.

Unfortunately, their underperformance against proper benchmarks has been just as great in these asset classes. The reason is that less efficient markets are characterized by lower trading volumes, resulting in less liquidity and greater trading costs. I recently presented the evidence on active management in emerging markets.

As more investors move to passive strategies, it’s logical to conclude trading activity would decline. Yet while we have seen a shift to passive management by individuals and institutions, trading volumes have continued to set new records as the market’s remaining active participants are becoming more active.

However, if, as investors shifted to passive management, trading activity fell, liquidity would decline and trading costs would rise. The increase in trading costs would raise the already-substantial hurdle active managers must overcome. Based on the evidence we’ve seen from the “inefficient” small-cap and emerging markets, any information advantage gained by a lessening of competition would be offset by an increase in trading costs. Remember, the costs of implementing an active strategy must be small enough that market inefficiencies can be exploited, after expenses.

There is another interesting conclusion to draw about the trend toward passive investing – one discussed in “The Incredible Shrinking Alpha.” For active managers to win, they must exploit the mistakes of others. It seems likely those abandoning active management in favor of passive strategies are investors who have had poor experience with active investing.

This seems logical, because it’s not likely that an investor would abandon a winning strategy. The only other logical explanation I can come up with is that an individual simply recognized they were lucky. That conclusion would be inconsistent with behavioral studies showing individuals tend to take credit for their success as skill-based, and to attribute failures to bad luck.

Thus, it seems logical to conclude the remaining players are likely to be those with the most skill. Therefore, we can conclude that, as the “less skilled” investors abandon active strategies, the remaining competition, on average, is likely to get tougher and tougher.

Summary

As sure as the sun rises in the east, the proponents of active management will continue to attack passive investing. The reason is simple: It threatens their livelihood. Thus, their behavior should not come as a surprise.

A fitting conclusion is this quotation from perhaps our greatest economist, Paul Samuelson: “[A] respect for evidence compels me to incline toward the hypothesis that most portfolio decision-makers should go out of business – take up plumbing, teach Greek, or help produce the annual GNP by serving as corporate executives.”

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All