Will Re-Defaults of Mortgage Modifications Undermine Housing Markets?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMuch has been written about residential mortgage modifications, yet hardly anything has been said about the problem of re-defaults on modified mortgages. In large part, this is due to the paucity of accurate data about borrowers re-defaulting. It is time to clearly lay out how extensive this problem really is, what it means for mortgage markets and the dangers it poses for investors.

The basics of mortgage modifications

Millions of borrowers having trouble making regular mortgage payments have been given a mortgage modification by the servicer as an alternative to foreclosure. In their latest report, the consortium known as HOPE NOW shows a cumulative total of 8.4 million permanent modifications since the end of 2007. This includes the government's HAMP modification program begun in 2009, proprietary modifications offered by non-government lenders and the GSEs' modification programs.

Under a modification, permanent changes are made to the original mortgage via 1) reductions in the interest rate; 2) stretching out of the amortization period; 3) adding the interest arrears to the principal owed (known as capitalization); or 4) reduction in the principal amount owed.

Although this is a lot of foreclosure avoidance, it does not include any of the temporary solutions offered by lenders. The two main ones are known as forbearances and repayment plans. Millions of borrowers who may not qualify for a permanent modification have been provided a temporary reduction or deferment of the scheduled payment until their financial condition improves.

How many temporary solutions have been granted? HOPE NOW reports a cumulative total of 16.4 million under the category “other workout plans.” These temporary plans are not reported under modification data. Unlike a permanent modification, these temporary plans do not change the terms of the original mortgage. They merely defer or reduce the monthly payments until the borrower's financial condition improves. As with permanent modifications, the borrowers given temporary workout plans are considered current. Take a good look at this HOPE NOW table to see what I am talking about.

What is the big deal?

Some of you may wonder why this modification re-default matter is important. Fair enough. Let me explain. In 2009, regulators such as the FDIC had become terrified that the housing and commercial real estate collapse might engulf the entire financial system. So they encouraged mortgage lenders and their servicers to find alternatives to foreclosure of seriously delinquent borrowers. As early as 2009, more than 1.2 million permanent modifications had been initiated. That number grew to 1.75 million in 2010 – the peak year of modifications.

2010 was also the peak year for completed foreclosures – slightly more than one million. As home prices continued their sharp decline in 2009 and 2010, panicked lenders and their servicers decided that they could stop the bleeding if they drastically reduced the number of repossessed properties placed on the active housing market. That is exactly what happened.

Actually, RealtyTrac began reporting as early as April 2009 that most foreclosed properties were being held off the market. They estimated that as many as 600,000 repossessed houses had not been put on the market. Roughly 80,000 homes in California alone had been kept off the market. This had apparently begun in California as early as 2007.

By the summer of 2012, an important article entitled “Shadow REO” reported that as many as 90% of all foreclosed properties were being withheld from sale. This was the best estimate of both RealtyTrac and CoreLogic. Since 2010, I have been reporting that this was definitely the case throughout the NYC metro.

Lenders and their servicers were not selling many of their foreclosed properties since the housing crash began. How does this relate to their mortgage modification strategy?

It was not sufficient for the lenders and their servicers to restrict the supply of foreclosed properties thrown onto the marketplace. There were simply too many delinquent borrowers whose homes had not even been foreclosed. Mortgage modifications were seen as an integral part of the foreclosure avoidance solution. If millions of delinquent mortgages could be modified, this would drastically reduce the number of homes that would have to be repossessed. This two-pronged strategy succeeded in artificially pushing up home prices and fooling everyone into thinking that the worst was over.

Why re-defaults are the key to everything

When they began, mortgage modifications were seen as a temporary solution that would, over time, enable delinquent homeowners to recoup the lost equity in their homes. Given the massive number of modifications that have been implemented since 2009, whether they succeed beyond merely delaying a default depends entirely on the extent to which those owners with modifications re-default.

Let's start with Fannie Mae modifications. We have fairly complete data from Fannie's quarterly Credit Supplement. In the third and fourth quarters of 2012, 24% of borrowers with modifications had re-defaulted after 12 months. By the last quarter of 2017, that percentage had climbed to 37%. Even worse, 30% of borrowers with 2017 modifications had re-defaulted within three months. That has soared from only 15% in the last quarter of 2012.

Fitch Ratings provides more thorough information on Fannie Mae modifications. In July 2016, Fannie Mae released an enormous loan-level data set that Fitch used for its report on the growing risk in mortgage loan modifications. In the report, Fitch analyzed nearly 700,000 Fannie Mae modifications undertaken between 2010 and 2015.

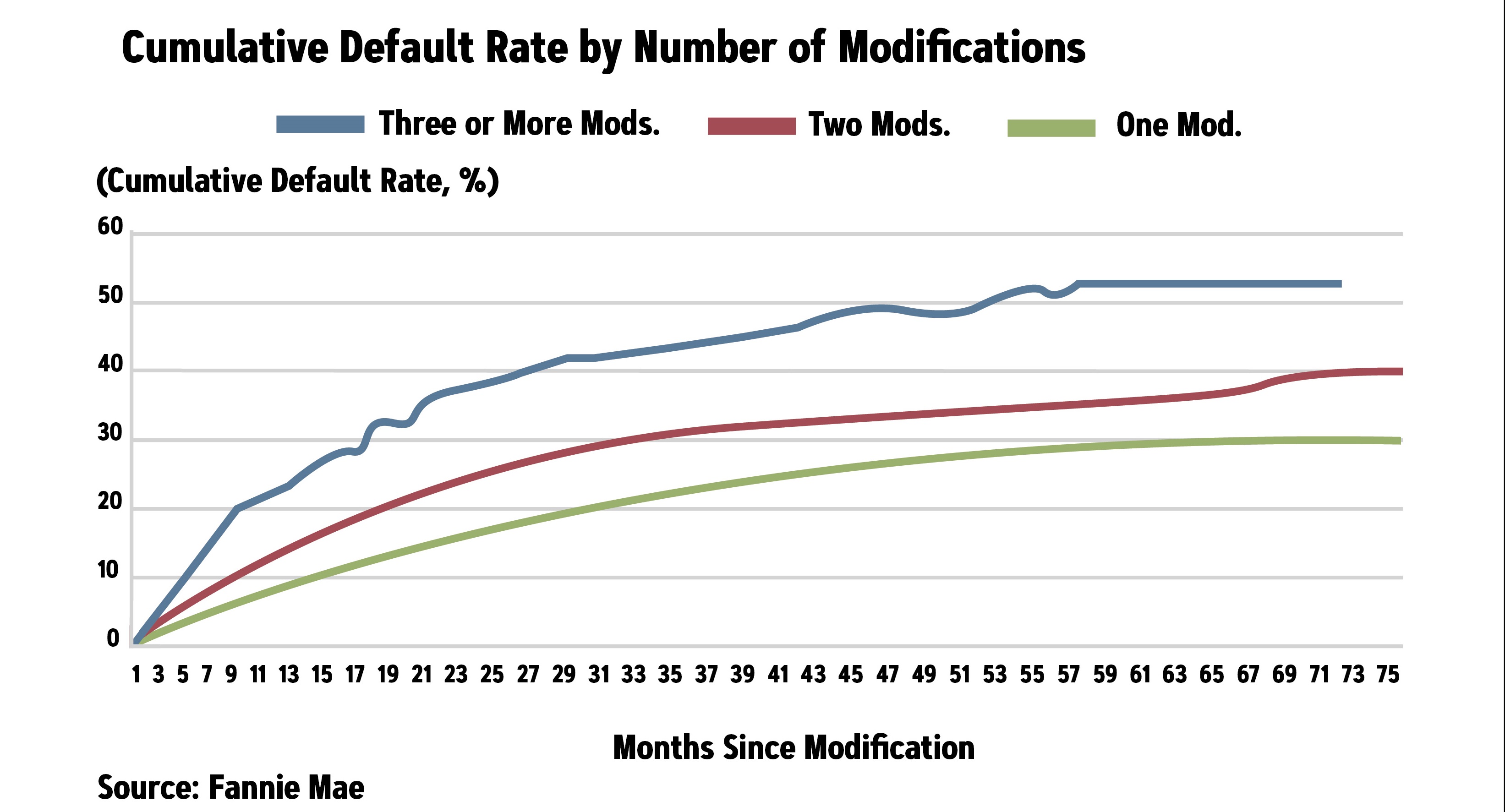

Since 2010, a steadily rising percentage of newly-modified loans were second or third modifications. Here is the really shocking number from this report. By 2015, fully one-third of new modifications were on properties which were previously modified and whose owners had then re-defaulted.

The newest Fannie Mae program – called Streamlined Modification – does not require the borrower to show any financial hardship. It seems that Fannie Mae no longer cares why homeowners want a modification as long as the loan is seriously delinquent. This new program accounts for the highest rate of Fannie Mae re-defaults. The streamlined program allows up to three additional modifications. This graph from Fitch's report shows that the re-default rate rises substantially with each new modification.

How many Fannie Mae modifications are outstanding? Its latest 10-Q report for the first quarter of 2018 reveals $152 billion of single-family loan modifications which are called “troubled debt restructurings (TDRs).” Of this total, an unpaid balance of $144 billion are classified as “individually impaired loans.” These are modified loans which Fannie Mae deems unlikely to collect all the contractual amount owed.

Although Fannie Mae stated in its report that 72% of these TDRs are accruing interest, the reality is far different. While the impaired loans were credited with $1.5 billion in recognized interest income for the first quarter of 2018, a mere $159 million of that was interest income “recognized on a cash basis.” What this accounting sleight-of-hand means is that the vast majority of borrowers with modified loans considered accruing were not paying any interest on their loans. The only reasonable inference to draw is that a huge majority of these modified loans had re-defaulted. Fannie Mae seems to be in no hurry to foreclose on these re-defaulted loans.

Is the high percentage of modification re-defaults limited to Fannie Mae loans? Absolutely not. What does the re-default rate look like for FHA loans in Ginnie Mae pools? A 2014 study reviewed nearly 3.3 million FHA loans modified between 2008 and the middle of 2013. It found that less than 43% were still current in 2013. Hence roughly 57% of these 3.3 million modified FHA insured loans had re-de-faulted. Think what might have happened if these re-defaulted loans had been foreclosed.

The Office of the Comptroller of the Currency (OCC) regulates national banks and issues a quarterly Mortgage Metric Report for the big banks that service large numbers of mortgages. Its report for the first quarter of 2013 included roughly 55% of all mortgage loans serviced in the US. Out of all the FHA loans in Ginnie Mae pools which had been modified, nearly 60% had re-defaulted within 36 months.

In its January 2018 Single Family Loan Performance Trends report, FHA revealed that it currently insures slightly more than 8 million residential mortgages. Forty per cent of these borrowers had FICO scores low enough to be considered subprime. Nearly 12% of the 8 million insured loans were past due by more than 30 days. Yet fewer than 37,000 of these delinquent loans were foreclosed and sold in 2017. The report says nothing about modified loans or re-default rates.

How about some of the too-big-to-fail banks? The most recent JPMorgan Bank 10-Q report for the fourth quarter of 2017 shows that 46% of all their troubled debt residential mortgage restructurings (TDRs) had re-defaulted and were seriously delinquent again. Nearly two-thirds of these re-defaulted loans were placed in “non-accrual” because the bank did not expect to recover the entire principal owed. A year earlier, their re-default percentage was only 39%.

For the nation's largest banking institution – Bank of America -- the TDR re-default percentage for the fourth quarter of 2017 was 45%. For the nation's ninth largest bank – PNC Bank – the figure is a whopping 57%. Wells Fargo – the third largest bank – showed a re-default percentage of only 35%.

What about the worst of the bubble-era mortgages – the private, non-guaranteed loans with the poorest underwriting? The best database of these mortgages was sold by BlackBox Logic to Moody's at the end of 2015. To date, I have not seen any report or study by Moody's which makes use of this database.

That Black Box Logic's database of non-guaranteed securitized loans (known as non-agency mortgages) is no longer available is unfortunate. These loans were the worst of bubble-era junk and are where the bulk of the sub-prime mortgages are found. According to the Securities Industry and Financial Markets Association (SIFMA), there are still more than $700 billion of them outstanding.

Fortunately, there is a study published in September 2016 which had access to the BlackBox Logic database before it was sold. The study analyzed roughly 176,000 of these subprime loans which had been modified and tracked their performance through 2013. The author found that 44% of them had re-defaulted within a year and 60% within two years. This is quite consistent with these other re-default statistics.

I also have recent data from TCW which publishes a monthly Mortgage Market Monitor. Its latest report with data through March 2018 reveals that prime, subprime and Alt-A securitized mortgages have been delinquent for an average of more than two years before the major servicers modify the loan. Since the report shows that most of these modified loans had the delinquent interest added to the amount of principal owed, most of them are still badly underwater.

I used to correspond regularly with the person in charge of BlackBox Logic's comprehensive database for these non-agency loans. In 2015, he informed me that one-third of all these loans had already been modified. The percentage for California loans modified was more than 40%. He did not say how many of them had re-defaulted.

There is only one plausible conclusion we can draw from these worsening re-default numbers: Mortgage modification has failed as a solution to the mortgage delinquency problem. Millions of borrowers continue to become delinquent regardless of their financial situation.

Why can't the perpetual delaying game continue indefinitely?

I am asked this question regularly. If re-defaults are growing, why haven't the lenders and their servicers been compelled to start foreclosing on more long-term deadbeats? The regulators are certainly not putting pressure on them to do this. Since continuing this game has helped lenders and servicers to completely turn around housing markets, what could possibly force them to end it?

Banks, mortgage servicers and the GSEs have been able to pull off this charade because hardly anyone knows how bad the re-default situation really is. Even mortgage pros don't really know that there is a problem. How could they? I am not aware of another analyst writing about this looming disaster. The re-default numbers you see in this article have been buried where few people can find them.

Why can't the banks and servicers continue to do what they've been doing since 2010?:

- not foreclosing on long-term deadbeats or those who continue to re-default on their modified mortgages; or

- not selling previously repossessed properties in their inventory

If it has worked up until now, why change course?

Is the NYC metro where we are heading?

There is one major market where we can see most clearly how large is the horde of delinquent homeowners who have no desire to pay their mortgage. It is the largest metro in the nation – New York City.

Since 2009, a New York state statute has compelled all mortgage servicers to send what it called a pre-foreclosure notice to any owner-occupant who is at least 30 days delinquent on the mortgage payment. They are also required to send figures to the NY State Department of Financial Services (DFS) on how many have been sent out. Two reports were put out by DFS in 2010, but nothing has been published since then.

Since 2011, I have been in contact with a key person at the DFS and have been receiving unpublished but very accurate quarterly updates on these pre-foreclosure notice figures for New York City and the two Long Island counties of Nassau and Suffolk. A cumulative total of 1.17 million notices have been sent to delinquent homeowners in just these seven counties since the program began in 2010 and nearly 2.3 million in all of New York state.

My contact has repeatedly assured me that roughly 60% of these notices are first-time and 40% are repeat notices. Repeat notices are second or third notices sent to long-term deadbeats who have neither cured the delinquency nor lost the property through foreclosure.

I have been asked by skeptical readers over the years how many of these notices are duplicates. In his latest update for the first quarter of 2018, my contact reported for the first time that slightly under 20% of the totals in both this update and the previous one were duplicate notices. When I queried him about this, he suggested that it was due to the carelessness and laziness of the reporting mortgage servicers. Notwithstanding these duplicate notices, the cumulative total sent out since 2010 is still severe for the NYC metro and for the entire state.

The word has spread throughout the NYC metro that mortgage servicers are not foreclosing on seriously delinquent homeowners. Knowing this, tens of thousands of owners decide each month to simply stop paying their mortgages and take their chances. The odds favor them. That is why so many of these delinquent homeowners have not made mortgage payments in five, six, seven years or longer.

It is clear from the updates I receive that the vast majority of these delinquent mortgages have not been modified by servicers. I am at a loss to explain why.

Who are the losers in this game of chicken? It is the owners of these mortgages – investors large and small who own instruments such as mortgage-backed securities (MBS) are not being re-paid. I suspect that they are baffled about what is going on in the NYC metro and in all of New York state. If these loans are still held inside a MBS, there is little that the owner can do.

So what does this have to do with the re-default problem? Plenty. Homeowners who have re-defaulted one or more times on their mortgage modification(s) have one thing in common with those deadbeats in the NYC metro who simply haven't paid in years. They have no intention of repaying the mortgage.

What do RIAs need to tell their clients?

There are millions of modified mortgage loans around the country that are now delinquent again. Will their mortgage servicer decide to do what servicers in the NYC metro have been doing for years – just leave them alone and do nothing? That is no solution, but at least the servicer does accrue servicing fees and late fees which can eventually be collected when the loan is foreclosed. These accrued fees will come out of the principal repayments owed to the lender at the time of final liquidation.

How does this mortgage re-default issue affect your clients? Let me suggest several ways.

- They may own a Ginnie Mae MBS that holds FHA-insured loans. Here is what they almost certainly don't know: FHA-insured loans originated in 2005-2009 now show delinquency rates in excess of 20%. Loans from 2010 have a delinquency rate of nearly 15%. As I explained earlier, FHA has been foreclosing on fewer than 4% of delinquent loans. Those loans foreclosed are the smallest of the insured loans with an average outstanding balance of $120,000 in 2017. Because average losses on foreclosed home sales were roughly 55%, FHA does not want to take the income hit were it to foreclose on more expensive insured loans.

The price your client paid for Ginnie Maes does not reflect these modification re-defaults, high delinquency rates or losses on foreclosed properties. When FHA is finally compelled to foreclose on large numbers of defaulted loans, the price of Ginnie Maes will almost certainly plunge. The time to unload them is now, unless your analysis shows that the price of the security already reflects this risk.

- Many RIA clients own non-agency residential mortgage-backed securities (RMBS) either directly or through investing in total-return funds which own substantial amounts of these RMBS tranches. If you own these funds, ask the manager how much is held in securities that contain non-performing loans, and ask whether the market price for those securities properly reflects the default risks I have identified in this article. As with the Ginnie Maes, prices of these bond funds will almost certainly decline when the mortgage servicers finally have to foreclose on large numbers of these deadbeat homeowners.

RIA clients may own mortgage REITS such as Two Harbors (TWO), American Capital Agency (AGNC), and Invesco Mortgage Capital (IVR) which own substantial amounts of non-agency RMBS tranches. I discussed them in detail three years ago in an article about mortgage REITs. Unwary investors look only at the dividend yield when evaluating these REITs. As I have explained, the delinquency and re-default problems with these non-agency loans continue to deteriorate, yet investors are completely uninformed about the risks they face.

- Some RIA clients may have purchased Fannie Mae shares before the crash and were unable or unwilling to sell out before the stock price collapsed. Or perhaps they may have purchased either Fannie Mae common shares or junior preferred shares on the chance that the U.S. Treasury Secretary will actually act on the widespread speculation that he might end the conservatorship and return Fannie Mae to a privately-owned company.

RIA clients need to be informed that $116 billion of Fannie Mae's retained mortgage portfolio consists of the worst junk. As I explained earlier, these are impaired whole loans which have been modified and have re-defaulted. Many borrowers have not paid a nickel for years. Fannie Mae has been selling off these loans for several years to hedge funds who thought they got a good discounted price. Don't believe that for a second.

Conclusion

The real mortgage delinquency situation around the nation is much closer to what is occurring in the NYC metro than what you can read every month in the Mortgage Bankers Association's monthly delinquency survey. Let my analysis in this article serve as a warning to investors and their advisors.

Keith Jurow is a leading real estate analyst and former author of Minyanville's Housing Market Report. His Capital Preservation Real Estate Watch provides in-depth analysis and media interviews covering the entire real estate space.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All