Global Trade and the Unsustainability of Federal Debt

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“We are addicted to our reserve currency privilege, which is in fact not a privilege but a curse.” -James Grant, Grant’s Interest Rate Observer

Trade negotiations and the threat of global tariffs are contributing to significant volatility in the financial markets. Although applicable in many ways, the Smoot-Hawley protectionist act of 1930 is unfairly emphasized as the primary point of reference for understanding current events.

In 1944, an historic agreement was forged amongst global leaders that would shape worldwide commerce for decades. The historical precedence of post-WWII trade dynamics offers a thoughtful framework for understanding why trade negotiations are so challenging. This article uses that period as a means of improving the clarity of our current lens on complex and fast-changing trade dynamics.

Folklore states that Robert Johnson went down to the crossroads in Rosedale, Mississippi and made a deal with the devil in which he swapped his soul for musical virtuosity. In 1944, the United States and many nations made a deal in Bretton Woods, New Hampshire. The agreement, forged at a historic meeting of global leaders, has paid enormous economic benefits to the United States, but due to its very nature, has a flawed incongruity and a dear price that must be paid.

In 1960, Robert Triffin brilliantly argued that ever-accumulating trade deficits, the flaw of hosting the reserve currency and the result of Bretton Woods, may help economic growth in the short run but would kill it in the long run. Triffin’s theory, better known as Triffin’s Paradox, is essential to grasp the current economic woes and, more importantly, recognize why the path for future economic growth is far different from that envisioned in 1944.

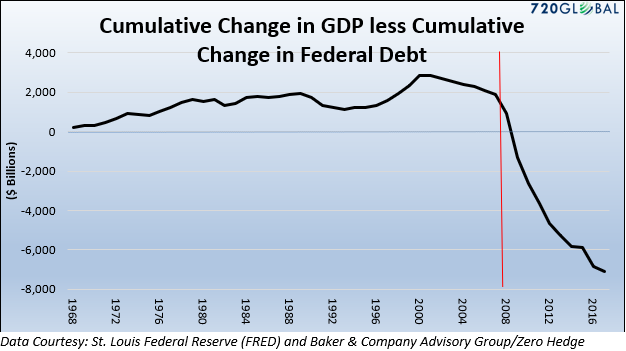

The financial crisis of 2008 was likely an important warning that years of accumulating deficits and debts associated with maintaining the world’s reserve currency are finally be reaching their tipping point. Despite the last nine years of outsized fiscal spending and unprecedented monetary stimulus, economic growth is well below the pace of recoveries of years past. In fact, as shown below, starting in 2009 the cumulative amount of new federal debt surpassed the cumulative amount of GDP growth going back to 1967. Said differently, if it were not for a significant and consistent federal deficit, GDP would have been negative every year since the 2008 financial crisis.

Bretton Woods and dollar hegemony

By decree of the Bretton Woods Agreement of 1944, the U.S. dollar supplanted the British pound and became the global reserve currency. The agreement assured that a large majority of global trade was to occur in U.S. dollars, regardless of whether or not the United States was involved in such trade. Additionally, it set up a system whereby other nations would peg their currency to the dollar. This arrangement is somewhat akin to the concept of a global currency. This was not surprising, as a few years prior John Maynard Keynes introduced a supranational currency by the name of “Bancor.”

Within the terms of the historic agreement was a supposed remedy for one of the abuses that countries with reserve-currency status typically commit: the ability to run incessant trade and fiscal deficits. The pact established a discipline to discourage such behavior by allowing participating nations the ability to exchange U.S. dollars for gold. In this way, other countries that were accumulating too many dollars, the side effect of American deficits, could exchange their excess dollars for U.S.-held gold. A rising price of gold, indicative of a devaluing U.S. dollar, would be a telltale sign for all nations that America was abusing her privilege.

The agreement began to fray after only 15 years. In 1961, the world’s leading nations established the London Gold Pool with an objective of maintaining the price of gold at $35 an ounce. By manipulating the price of gold, a gauge of the size of U.S. trade deficits was broken and accordingly the incentive to swap dollars for gold was diminished. In 1968, France withdrew from the Gold Pool and demanded large amounts of gold in exchange for dollars. By 1971, President Richard Nixon, fearing the U.S. would lose its gold if others followed France’s lead, suspended the convertibility of dollars into gold. From that point forward, the U.S. dollar was a floating currency without the discipline imposed upon it by gold convertibility.

The Bretton Woods Agreement was, for all intents and purposes, annulled.

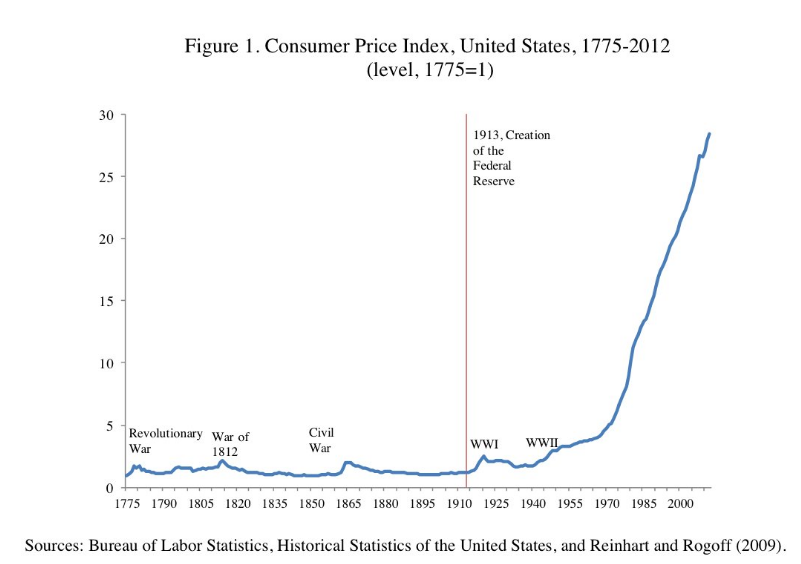

The following 10 years were marked by double-digit inflation, persistent trade deficits and weak economic growth, all signs that America was abusing its privilege as the reserve currency. Other nations grew increasingly uncomfortable with the dollar’s role as the reserve currency. The first graph below shows that, like clockwork, the U.S. began running annual deficits in 1971. The second graph highlights how inflation picked up markedly after 1971.

By the the late 1970s, to break the back of crippling inflation and remedy the nation’s economic woes, then Chairman of the Federal Reserve, Paul Volcker, raised interest rates from 5.875% to 20.00%. Although a painful period for the U.S. economy, his actions not only killed inflation and ultimately restored economic stability but, more importantly, satisfied America’s trade partners. The now floating-rate dollar regained the integrity and discipline required to be the reserve currency despite lacking the checks and balances imposed upon it by the Bretton Woods Agreement and the gold standard.

As an aside, my article, The Fifteenth of August, discussed how Nixon’s “suspension” of the gold window unleashed the Federal Reserve to take full advantage of the dollar’s reserve-currency status.

Enter Dr. Triffin

In 1960, 11 years before Nixon’s suspension of gold convertibility and essentially the demise of the Bretton Woods Agreement, the economist Robert Tiffin foresaw this problem in his book, Gold and the Dollar Crisis: The Future of Convertibility. According to his logic, the extreme privilege of becoming the world’s reserve currency would eventually carry a heavy penalty for the U.S. Although initially his thoughts were generally given little consideration, Triffin’s hypothesis was taken seriously enough for him to gain a seat at an obscure congressional hearing of the Joint Economic Committee in December the same year.

What he described in the book, and his later testimony, became known as Triffin’s Paradox. Events have played out largely as he envisioned it. Essentially, he argued that reserve status affords a good percentage of global trade to occur in U.S. dollars. For this to occur the U.S. must supply the world with U.S. dollars. In other words, to supply the world with dollars, the United States would always have to run a trade deficit whereby the dollar amount of imports exceeds the dollar amount of exports. Running persistent deficits, the United States would become a debtor nation. The fact that other countries need to hold U.S. dollars as reserves tends to offset the effects of consistent deficits and keeps the dollar stronger than it would have been otherwise.

The arrangement is as follows: Foreign nations accumulate and spend dollars through trade. To manage their economies with minimal financial shocks, they must keep excess dollars on hand. These excess dollars, known as excess reserves, are invested primarily in dollar-denominated investments ranging from bank deposits to U.S. Treasury securities and a wide range of other financial securities. As the global economy expanded and more trade occurred, additional dollars were required. Further, foreign-dollar reserves grew and were lent back, in one form or another, to the U.S. economy. This is akin to buying a car with a loan from the automaker. The only difference is that trade-related transactions occurred with increasing frequency, the loans are never paid back, and the deficits accumulate (Spoiler alert – the auto dealer would have cut the purchaser off well before the debt burden became too onerous).

The world has grown dependent on this arrangement as there are benefits to all parties involved. The U.S. purchases imports with dollars lent to her by the same nations that sold the goods. Additionally, the need for foreign nations to hold dollars and invest them in the U.S. has resulted in lower U.S. interest rates, which further encourages consumption and at the same time provides relative support for the dollar. For their part, foreign nations benefited as manufacturing shifted away from the United States to their nations. As this occurred, increased demand for their products supported employment and income growth, thus raising the prosperity of their respective citizens.

While it may appear the post-Bretton Woods covenant was a win-win pact, there is a massive cost accruing to everyone involved. The U.S. is mired in economic stagnation due to overwhelming debt burdens and a reliance on record-low-interest rates to further spur debt-driven consumption. The rest of the world, on the other hand, is her creditor and on the hook if and when those debts fail to be satisfied. Thus, Triffin’s paradox simply states that with the benefits of the reserve currency also comes an inevitable tipping point or failure.

Looking forward

The two questions that must be considered are as follows:

- When can our debts no longer be serviced?

- When will foreign nations, like the auto dealer, fear such a day and stop lending to us (i.e., transacting in U.S. dollars and recycling those into U.S. securities)?

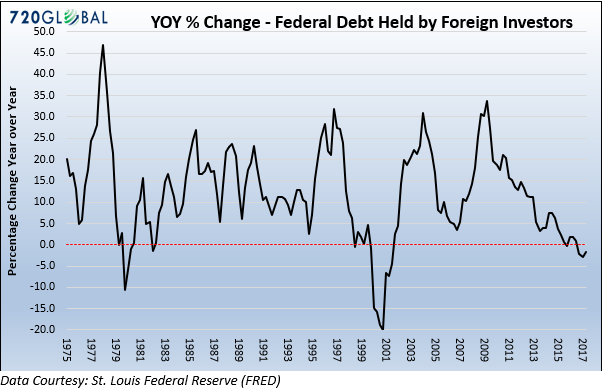

It is very likely the financial crisis of 2008 was an omen that America’s debt burden is unsustainable. Further troubling, as shown below, foreign investors have not only stopped adding to their U.S. investments of federal debt but have recently begun reducing them. This puts additional pressure on the Federal Reserve to make up for this funding gap.

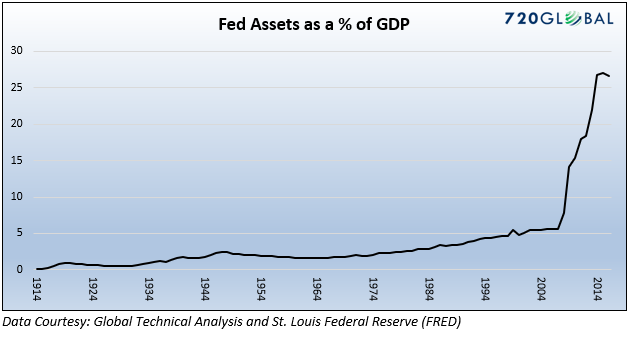

Assuming these trends continue, America must contend with an ever-growing debt balance that must be serviced. There are two likely end scenarios. Either the resolution of debt imbalances occurs naturally via default on some debt and paying down of other debts, or the Federal Reserve continues to “print” the digital dollars required to make up for the lack of funds the debt servicing and repayment requires. Given the Fed has already printed approximately $4 trillion to arrest the slight deleveraging that occurred in 2008, it does not take much imagination to expect this to be its modus operandi in the future. The following graph helps put the scale of money printing in proper historical context.

Summary

In a 2013 interview, Yanis Varoufakis, economist, academic and the Greek minister of finance during the most recent Greek debt crisis, mentioned a manuscript that he had recently read. The document, written in 1974 by Paul Volcker was directed to his then-boss, Secretary of State Henry Kissinger. Volcker stated that the U.S. need not manage its deficit as would be typical. Instead, he opined that it is our job to manage the surplus of other countries.

America’s ability to run deficits and accumulate massive debt balances for over 40 years, while maintaining its role as the global reserve currency, is a testimony to the power of our politicians and central bankers to “manage the surplus of other countries.” The questions to consider are:

- How much longer can the United States manage this tall and growing task?

- What is the tolerance of foreign holders of U.S. dollars in the face of dollar devaluation?

- Is the post-financial crisis “calm” the result of a durable solution or a temporary façade?

If in fact 2008 was a first tremor and signal of the end of this arrangement, then we are in the eye of the storm and future disruptions promise to be more significant and game-changing.

This concept has far-reaching implications well beyond economics and investing. Future articles will extend the analysis on this topic and shed further light on how and when Triffin’s paradox may climax. I will also offer investment strategies to protect and grow your wealth during what may be tumultuous times ahead.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All