Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Tax Cuts and Jobs Act (TCJA) has created a media frenzy and widespread confusion. With that in mind, I will provide a brief overview of the new provisions, followed by some practical ideas on ways to reduce taxes.

The bill slashes corporate tax rates and cuts individual tax rates – especially for high-income taxpayers. The corporate reductions are permanent while the individual tax cuts expire after 2025. Over the next decade, these provisions are expected to add about $1.5 trillion to the U.S. deficit. What advisors need to know is this: Some people will benefit from TCJA, while others will find their tax liabilities increased.

Below are the individual tax changes at a high level followed by some observations:

-

Highest tax bracket is reduced to 37% versus the prior 39.6%.

- Remember that material reductions don’t occur until income levels are over $75,000 for singles and $150,000 for married couples.

-

The standard deduction is doubled to $12,000 for singles and $24,000 for married couples.

- We may see fewer people itemizing deductions.

-

Alternative Minimum Tax (AMT) exemptions are increased.

- As a result, fewer high income people will be subject to AMT and, if subject to AMT, will pay less.

-

The estate tax exemption is doubled to almost $11 million per person.

- This means that fewer estates will be subject to estate tax.

-

Personal exemptions are eliminated.

- This elimination essentially offsets benefits from the standard deduction increase.

-

The mortgage interest deduction for new purchases of main and second homes is now limited to a maximum principal of $750,000 – and deductions for home-equity interest are eliminated.

- This could depress residential housing prices for higher price-tag homes and encourage “grandfathered” homeowners to not sell their homes.

-

Miscellaneous itemized deductions, including tax-preparation fees, investment-management fees, employee business expenses and professional dues, have been eliminated.

- This does not impact those subject to AMT.

Some practical ideas

1. Watch withholding

New withholding tables reflect lower tax rates under the new law. While individuals might feel good about getting a larger check each payday, the tables might not represent their particular tax picture. Therefore, individuals should be wary of fast money in their pockets and focus on tax planning. This can avoid unhappy surprises come April 2019.

2. Determine whether you will itemize or claim standard deduction

Many traditional itemized deductions are no longer allowed, and the standard deduction has been doubled. What this means is that many more taxpayers will be claiming the standard deduction – even if they itemized in the past. As of 2018, allowable itemized deductions will be the total of:

- Medical expenses in excess of 7.5% of AGI

- Home mortgage interest on principal of up to $1 million for pre-TCJA homes or $750,000 for newly acquired loans

- Charitable contributions

- Maximum $10,000 of state, local, and property taxes combined

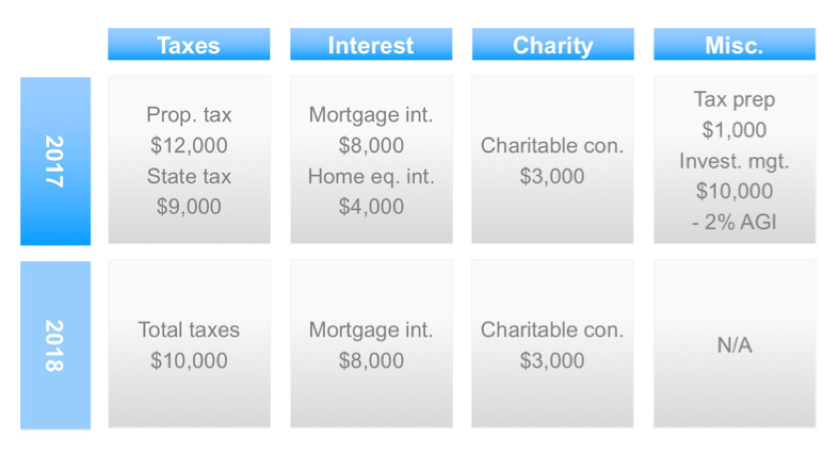

For example, we can compare a married couple's allowable itemized deductions for 2017 versus 2018 in the table below:

Assuming AGI of $150,000, this couple's 2017 itemized deductions would have totaled $44,000. The same expenses would result in allowable itemized deductions of only $21,000 in 2018. Without deducting home equity interest, miscellaneous itemized deductions and state/local/property taxes above $10,000, this couple will now be forced to claim the standard deduction of $24,000.

It is important for individuals to know if they will be itemizing or claiming the standard deduction because this can significantly impact planning moves.

3. Consider bunching deductions

Just because one claims standard deduction in one year doesn't mean they can't qualify to itemize in another year. Remember that claiming the standard deduction will get no tax benefit from paying state/local/property taxes, mortgage interest, charitable deductions or medical expenses in excess of 7.5% of AGI.

Some people will not qualify to itemize every year, and in that case, consider bunching deductions every other year. In the above example, let's say that the couple makes their January 1st mortgage payment in December and prepays their 2019 charitable commitment by the end of 2018. Additionally, let's assume that the couple pays an orthodontist bill by the end of 2018, leaving $2,000 of medical expenses in excess of 7.5% of AGI. Based on this, the couple's 2018 total itemized deductions will be $26,600 – greater than the $24,000 standard deduction.

4. Consider a donor-advised fund1

A donor-advised fund (DAF) can provide further opportunity to bunch charitable deductions without immediately distributing funds to specific charities. A DAF is like a “charitable IRA.” The client gets an immediate tax deduction. The DAF invests the money until the investor decides to make grants to the charities of their choice and there is no tax on growth while the funds are invested. The investor can even contribute appreciated securities for a greater tax benefit. The deduction is claimed for the full value of the shares–and the investor doesn’t pay tax on the gain!

5. Pay attention to other tax-saving strategies

Be sure to remember other tax-saving strategies as applicable. These can include:

- IRA, SEP or other retirement plan contributions and/or Roth conversion

- Self-employed health insurance and/or health savings accounts (HSAs)

- 529 college-saving plans

- Tax-advantaged portfolio management, such as: tax-loss harvesting, tax-lot accounting, location optimization

- Retirement withdrawal strategies

Although much has changed under the TCJA, many of the "tried and true" planning strategies can still prove beneficial. The new tax proposals will have a major impact on taxpayers as well as the U.S. economy. You can become even more valuable to your clients by helping them understand how the new law will affect them personally.

Sheryl Rowling, CPA, is head of rebalancing solutions for Morningstar. In this role, she focuses on tax-efficient portfolio management strategies for Morningstar’s Total Rebalance Expert (tRx) software and serves as a subject-matter expert on tax-efficient investing, portfolio rebalancing, and advisor practice management.

Morningstar, Inc. and its affiliates do not provide tax, legal or accounting advice.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

1 Please consult with your investment professional about the benefits as well as limitations of a donor-advised fund prior to opening an account. Limitations of a donor-advised fund includes, but not limited to, money contributed to a donor-advised fund account is irrevocable and money within the account cannot be inherited by the donor’s beneficiaries. Donor-advised funds often require a minimum initial contribution amount and are subject to administrative and other types of fees. For information about a specific donor-advised fund including its board of directors please review its IRS Form 990.

Read more articles by Sheryl Rowling