Don’t Abandon International Diversification

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. This article originally appeared on ETF.COM here.

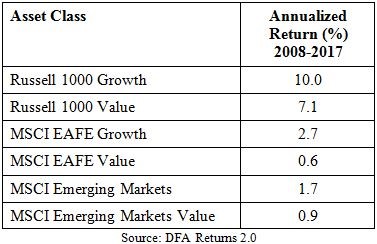

For the 10-year period 2008 through 2017, a very wide dispersion in returns has existed in markets. As the following table shows, U.S. stocks far outperformed international stocks, and growth stocks outperformed value stocks.

Given these results, it’s no surprise I have been getting lots of queries about international equity investments. Any time an asset class does poorly – even for a few years, let alone a decade – a significant number of investors will question why they own that asset.

One particular inquiry I received involved the fact that international equities not only had underperformed domestic equities since 2009, but they crashed in 2008. Just when the benefits from diversification were needed most, they failed to materialize. As a result, the advisor in this case doubted the reason for including international equities in his portfolio.

The recency problem

Among the errors discussed in my book, “Investment Mistakes Even Smart Investors Make and How to Avoid Them,” is one called recency. Recency is the tendency to overweight recent events/trends and ignore long-term evidence.

This leads investors to buy after periods of strong performance (when valuations are higher and expected returns are now lower) and sell after periods of poor performance (when prices are lower and expected returns are now higher). This results in the opposite of what a disciplined investor should be doing: rebalancing to maintain their portfolio’s asset allocation.

The problem created by recency is compounded when international stocks underperform, greatly increasing the risk that an investor will commit a mistake. This occurs because of another common error: confusing familiarity with safety, which leads to the well-documented, global phenomenon known as home-country bias.

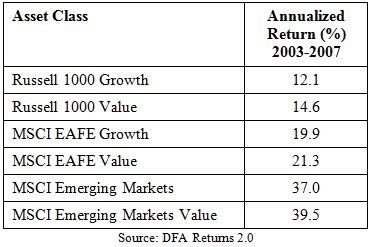

To address questions about where the benefits of international investing can be found, we don’t have to look too far back in time. The problem is that investor memories can be very short, often much shorter than is required to be a successful investor. The period we’ll examine is the five years from 2003 through 2007, the period just before the Great Financial Crisis.

As you can see, results in this period (2003-2007) were just the reverse of what they were in the period following it (2008-2017), with international stocks far outperforming U.S. stocks and value stocks outperforming growth stocks. As Spanish philosopher George Santayana famously warned, “Those who cannot remember the past are condemned to repeat it.”

In general, dramatic outperformance (underperformance) is accompanied by rising (falling) valuations, which generally leads to reversion in returns – higher valuations predict lower future returns, and vice versa.

Forward-looking return estimates

The academic research shows that, while valuations are poor predictors of short-term returns (and thus should not be used to time markets), they are the best predictor we have of future returns. At year-end 2017, the Shiller CAPE 10 earnings yield, as good a predictor of future real returns as any available, was 3.1% for the U.S., 5.1% for non-U.S. developed markets and 6.3% for emerging markets.

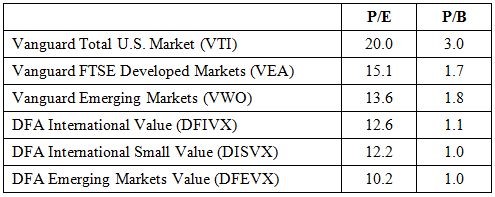

There are other valuation metrics we can observe. The table below shows the current price-to-earnings (P/E) ratio and price-to-book (P/B) ratio for three of Vanguard’s funds – Total (U.S.) Stock Market ETF (VTI), FTSE Developed Markets ETF (VEA) and FTSE Emerging Markets ETF (VWO) – and three Dimensional Fund Advisors (DFA) international value funds – International Value (DFIVX), International Small Cap Value (DISVX) and Emerging Markets Value (DFEVX).

Note that the research shows the current P/E has about the same explanatory power as the CAPE 10 ratio. Data is the latest available from Morningstar, with Vanguard data as of December 2017 and DFA data as of November 2017. (Full disclosure: My firm, Buckingham Strategic Wealth, recommends DFA funds in constructing client portfolios.)

Once again, we see that U.S. equity valuations are substantially higher than in developed markets and, especially, emerging markets. Of course, that’s a result of the vast outperformance by U.S. stocks over the prior 10 years. We also see wide spreads between the P/E and P/B ratios of value portfolios relative to market portfolios. Before summarizing, I’ll review an interesting paper on the importance of book-to-market ratios.

Book-to-market ratio importance

Michael Keppler and Peter Encinosa, authors of the study “How Attractive Are Emerging Markets Equities? The Importance of Price/Book-Value Ratios for Future Returns,” which appears in the Spring 2017 issue of The Journal of Investing, provide us with some further insights as to the returns we might expect from emerging markets.

For the period January 1989 through October 2016, they found that the P/B ratio of the MSCI Emerging Markets Index ranged from a low of 0.90 in January 1989 to a high of 3.02 in October 2007 and averaged 1.75. Note the current P/B ratio of VWO is 1.8 and for DFEVX it is just 1.0 (near the very bottom of the range). Keppler and Encinosa then divided the P/B range into three intervals and found:

- For 10 observations in the first interval, the P/B ratio was below 1.22. The average annual return in U.S. dollars in the four years that followed was 12.9% and never fell below zero.

- For 273 observations in the second interval, the P/B ratio fell between 1.22 and 2.76. The average annual return in the four years that followed was 9.4%.

- For four observations in the third interval, the P/B ratio exceeded 2.76. The average annual return in the four years that followed was -5.1%, and was always negative.

Keppler and Encinosa concluded there has been a negative relationship between the P/B ratio and future returns in emerging markets. They also warn investors that focusing on average returns hides a wide dispersion of outcomes.

For example, while the authors’ regression analysis led them to forecast a return of 12% per year for emerging markets over the ensuing four years, data from the previous 28 years indicate that the extreme outcomes lay between an annual loss of 8.8% and an annual gain of 36.9%.

Keppler and Encinosa found the same negative relationship between the P/B ratio and returns over the subsequent four years in developed markets. Over the period 1970 through October 2016, they found the developed markets’ lowest P/B ratio was l.01 in July 1982, the highest was 4.23 in December 1999, and the average was 2.06.

Note the current P/B ratio of VTI is 3 (near the top of the range) and 1.7 for VEA (well below the midpoint). Again, dividing the period into three intervals, they found:

- For 169 observations in the first interval, the P/B ratio was below 1.70. The average annual return in U.S. dollars in the four years that followed was 15.4%, and never below zero.

- For 319 observations in the second interval, the P/B ratio was between 1.70 and 3.46. The average annual total return four years later was 7.2%.

- For 27 observations in the third interval, when the P/B ratio was above 3.46, the average annual return over the next four years was -5.6%, and always negative.

The bottom line is that, currently, expected returns among emerging market equities, particularly emerging market value stocks, are much higher than they are for U.S. stocks (as well as for other developed markets, though to a lesser degree). Additionally, the expected returns of non-U.S. developed-market stocks are higher than they are for U.S. stocks.

With emerging markets now making up more than half of global GDP and about one-eighth of global equity capitalization, an emerging market allocation of one-eighth of your portfolio’s equity allocation is a worthwhile starting point to consider. Non-U.S. developed markets make up about three-eighths of the global market cap. That, too, is a good starting pointing for determining your allocation.

With that said, let’s examine the case for building such a globally diversified portfolio.

Global diversification case

Diversification rightly has been called the only free lunch in investing. A portfolio of global equity markets should be expected to produce a superior risk-adjusted return to any one country or region held in isolation. However, the benefits of global diversification came under attack as a result of the financial crisis of 2008, when all risky assets suffered sharp price drops as their correlations rose toward 1.

When that happened, many investors surmised that global diversification doesn’t work, because it fails when its benefits are needed most. That is wrong on two fronts.

First, the most critical lesson investors should have learned is that, because correlations of risky assets tend to rise toward one during systemic global crises, their portfolios should be sufficiently allocated to the safest bond investments (investments such as U.S. Treasury bonds, FDIC-insured CDs and municipal bonds rated AAA/AA). The overall portfolio should reflect one’s ability, willingness and need to take risk.

At the time it’s needed the most, during systemic financial crises, the correlations of the safest bonds to stocks, which average about zero over the long term, tend to turn sharply negative. They benefit not only from flights to safety, but also from flights to liquidity.

The second lesson that many investors failed to understand is that, while international diversification doesn’t necessarily work in the short term, it does work eventually. This point was the focus of a paper from Clifford Asness, Roni Israelov and John Liew, “International Diversification Works (Eventually),” which appeared in a 2011 issue of the CFA Institute’s Financial Analysts Journal.

The authors explained that those who focus on the fact that globally diversified portfolios don’t protect investors from short systematic crashes miss the greater point that investors whose planning horizon is long-term (and it should be, or they shouldn’t be invested in stocks to begin with) should care more about long, drawn-out bear markets, which can be significantly more damaging to wealth.

Diversification for the long term

In their study of 22 developed-market countries during the period 1950 through 2008, the authors examined the benefit of diversification over long-term holding periods. They found that, over the long run, markets don’t exhibit the same tendency to suffer or crash together.

As a result, investors should not allow short-term failures to blind them to long-term benefits. To demonstrate this point, the authors decomposed returns into two components: (1) those due to multiple expansions (or contractions); and (2) those due to economic performance.

They found that, while short-term stock returns tend to be dominated by the first component, long-term stock returns tend to be dominated by the second. They explained that these results “are consistent with the idea that a sharp decrease in investors’ risk appetite (i.e., a panic) can explain markets crashing at the same time. However, these risk aversion shocks seem to be a short-lived phenomenon. Over the long-run, economic performance drives returns.”

They further showed that “countries exhibit significant idiosyncratic variation in long-run economic performance. Thus, country specific (not global) long-run economic performance is the most important determinant of long-run returns.”

For example, in terms of worst-case performances, the authors found that, at a one-month holding period, there was very little difference in performance between home-country portfolios and global portfolios.

However, as the horizon lengthened, the gap widened. The worst cases for the global portfolios are significantly better (their losses were much smaller) than the worst cases for the local portfolios. The longer the horizon, the wider the gap favoring the global portfolios becomes.

Demonstrating the point that long-term returns are more about a country’s economic performance and that long-term economic performance is quite variable across countries, the authors found that “country specific economic performance dominates long-term performance, going from explaining about 1% of quarterly returns to 39% of 15-year returns and rising quite linearly in time.”

Summary

Forecasting returns is a largely futile effort. Thus, the prudent investment strategy is to build a globally diversified portfolio. But that’s simply the necessary condition for success. The sufficient condition is to possess the discipline to stay the course, ignoring not only clarion cries from those who think their crystal balls are reliable, but also cries from your own stomach to GET ME OUT! As Warren Buffett explained, “The most important quality for an investor is temperament, not intellect.”

To help you stay disciplined and avoid the consequences of recency, I offer the following suggestion: Whenever you are tempted to abandon your well-thought-out investment plan because of poor recent performance, ask yourself this question: Having originally purchased and owned this asset when valuations were higher and expected returns were lower, does it make sense to now sell the same asset when valuations are currently much lower and expected returns are now much higher?

The answer is obvious. If that’s not sufficient, remember Buffett’s further advice to never engage in market timing, but if you cannot resist the temptation, then you should buy when others panic.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits