So-called “smart-beta” strategies hasn’t been all that smart lately – at least not for the last five years. This article will examine why, whether it was predictable and the likelihood it will work better going forward.

Factor tilting, quantitative strategies that are weighted by something other than market capitalization, such as size and value, have been around for decades. They were first popularized by Nobel laureate and University of Chicago finance professor Eugene Fama and Dartmouth College finance professor Kenneth French. Often lost in their work was the fact that they never said those two factors were a free lunch that invalidated the efficient market hypothesis (EMH). Thus, I don’t agree with anyone referring to factor investing as “arbitrage,” since arbitrage is a riskless excess return based on inefficient markets.

Value and small-cap are expected to deliver excess long-term return as compensation for taking on more risk. One way of measuring that risk is with standard deviation, though few would argue that historic volatility adequately measures risk. While value may have a lower historic standard deviation than the broader market, those companies are typically weaker and riskier.

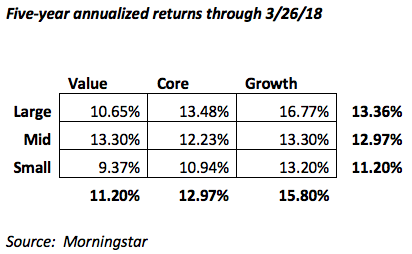

According to Morningstar, during the past five years, virtually the opposite of what would be expected over the long-run actually occurred. Large-cap bested mid- and small-cap while growth trounced value. In fact, large-cap growth turned in a 16.77% annualized return while small-cap value earned only 9.37%. That translates to a five-year 117% cumulative return for large-cap growth, or more than twice the 56% return for small-cap value.

Today there are many more factors than the original beta, size and value. According to Rich Wiggins, there are now more than 300 published factors and over 4,200 smart-beta indexes. More than 40 new factors are discovered annually. Morningstar refers to these smart-beta funds as strategic beta, and, according to Ben Johnson, director of global ETF research for Morningstar, the majority of strategic-beta ETFs have failed to deliver over the past one to three years.

Why smart-beta underperformance was predictable

Several years ago, I couldn’t attend an investing conference without the term “smart-beta” being mentioned every five minutes. Yet, I never heard once that this wasn’t a free lunch. Now there are smart-beta conferences where past performance is touted using back-tested data on new funds that didn’t actually exist over that period. As a result, money poured into those funds at a much faster rate than what I term as “dumb beta,” or basic market-cap-weighted index funds. Even Vanguard recently announced the launch of its own factor funds. Of course, whenever money pours into any one part of the market, it drives valuations up. And those higher valuations make future performance, relative to the overall market, less likely to keep up.

For those who think I’m using hindsight here, I’ve been on the record as embracing “dumb beta” for many years. I’ve also been critical of robo advisors with smart-beta tilts, and correctly predicted the Schwab Intelligent portfolio would underperform robos with equivalent lower cost cap-weighted portfolios.

Even the godfather of smart beta, Research Affiliate’s Rob Arnott, warned that smart beta can go horribly wrong. He noted “many investors are performance chasers who in pushing prices higher create valuation levels that inflate past performance, reduce potential future performance, and amplify the risk of mean reversion to historical valuation norms.”

In fact, the practice of data mining to find past outperformance to predict future outperformance is badly flawed. In the world of big data, it’s child’s play to come up with strategies that worked in the past and to use hindsight to come up with a plausible explanation as to why it worked and will in the future. Unfortunately, mean reversion combined with high fees make it unlikely future outperformance will continue. I’ve argued the process should be reversed and wrote about my fictitious new ETF called FAIL.

The failure of smart-beta tilting was predictable, though not a certainty – more like a meteorologist stating a 60% chance of rain. It’s not a case of once a factor is discovered, the premium immediately goes away. Rather, as money pours into that premium and it’s incorrectly viewed as a free lunch, failure is the more likely outcome. In other words, following the herd ends poorly. I did not predict it would underperform as much as it has, however, so it’s more like I predicted a 60% chance of showers and we got major flooding instead.

Will factor tilting work going forward?

I’m more optimistic about the future of smart-beta performance. Valuations in factors, such as size and value, are now more attractive as a result of past underperformance. And, Morningstar shows that cap-weighted index funds are seeing greater growth than smart-beta funds.

Over the next five years, I’m at least 95% certain small-cap-value will do better relative to large-cap growth than the shortfall size and value have had over the past five years. I even think it has a 50% chance of besting the overall market after costs. That is to say the expected premium, as compensation for taking on more risk, may cover its extra costs. Low-cost factor-tilted smart-beta funds are a viable active strategy, though one I don’t recommend.

I’m continuing to own and recommend market-cap weighted funds because I’ve found the guarantee that comes with market-cap indexing is powerful. William Sharpe’s simple paper, The Arithmetic of Active Management, proves an ultra-low-cost, broad market-cap-weighted portfolio must outperform active portfolios as a whole in the same asset class because of lower costs. Telling our clients that their cap-weighted total U.S. stock index fund must beat the average of other investors’ U.S. stock portfolios has psychological and financial value.

Smart beta can’t do that.

I tell clients that owning the entire market has enough risk and there is no need to take even more. Thus, I consider the original, simple, ultra-low-cost tax-efficient market-cap weighted index funds to be “brilliant beta” funds which may be more intelligent than smart beta!

If I haven’t convinced you, I can live with that. Factor tilting is an active strategy and active investors keep markets efficient. That efficiency allows cap-weighted indexes to have the true free lunch.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth