Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A recent article summarized the predictions of 500 advisors for the 10-year returns for a number of asset classes. If advisors construct portfolios based on those forecasts, they will destroy significant portions of their clients’ wealth.

Specifically, advisors expect large U.S. stocks to average 5% over the next 10 years (half of the long-term average of 10%). Fewer than 5% of advisors expect the next 10-year return to be equal to or greater than the 10% long-term performance of the stock market. (I will use nominal returns – before inflation – throughout this article.)

To further put this in perspective, for the nearly 70 years from 1950 through 2017, the stock market has experienced eight (14% of the total) rolling 10-year periods in which returns averaged less than 5%. Four of these were driven by the stagflation of the 1970s (none were negative) and four were prompted by the Bernanke-driven 2008 market crash (two were small negative and two were small positive).

On the other hand, 21 (36% of the total) of the rolling 10-year periods averaged returns greater than 15%. That is, it is nearly three times more likely to earn a 10-year return greater than 15% than it is to earn a return of less than 5%. Yet advisors are, on average, forecasting a 10-year return of 5%!

This begs the question of what horrific economic and market events do these advisors foresee to justify such a dour 10-year outlook for the stock market.

It’s the economy!

The history of stock returns reveals that regardless of whether we are primarily agrarian (early to mid-1800s), industrial (late 1800s to mid-1900s), or service/information (mid 1900s to present), the average annual return has been right around 10%. The reason is that during each of these periods, economic growth varied little, allowing stocks to generate the same average return in each of these dramatically different time periods.

Economic growth provides the guidewire around which market prices fluctuate. The stock market goes up over time because the economy grows over time. Furthermore, the most economically successful companies generate the highest long-term returns. An investment in the stock market is a bet on the future success of the underlying economy.

What do advisors see regarding the economy that would lead them to believe the next 10 years will be so dismal? It turns out not much. The economy is booming, with strong growth as indicated by both purchasing manager indices (PMIs) at or above 60 and inflation remaining low. Interest rates are expected to rise, but this is normal for a strengthening economy. The current quarter saw the largest uptick in expected earnings in a decade, driven by a tax reduction and technology tailwinds. This strong earnings growth will more than offset the negative impact of rising rates on stock prices.

Many point to the currently high CAPE and overall average P/E ratio as an indication that the market has gotten ahead of the economy. At AthenaInvest, we focus on the median-forward P/E, as it avoids the well-known problems associated with including 2008 in 10-year earnings estimates and the bias from including high P/Es for companies with earnings near zero when calculating an average P/E. The current S&P 500 median-forward P/E is a bit above its long-term average, indicating some but not worrisome overvaluation.

At AthenaInvest, we also focus on behavioral market measures. Our three market barometers, which capture deep behavioral currents in the U.S. large-cap, U.S. small-cap, and international developed stock markets, are all indicating expected returns of approximately 10%. Our technical measures, which capture short-term behaviors, are showing normal strength as well.

Based on current economic, valuation and behavioral data, I am hard-pressed to come up with a narrative to support the pessimistic return outlook captured by the advisor survey. Unless advisors are anticipating major, adverse events years in advance, there is little in the current environment that justifies anything other than a normal return forecast for the next 10 years.

Historical stock returns

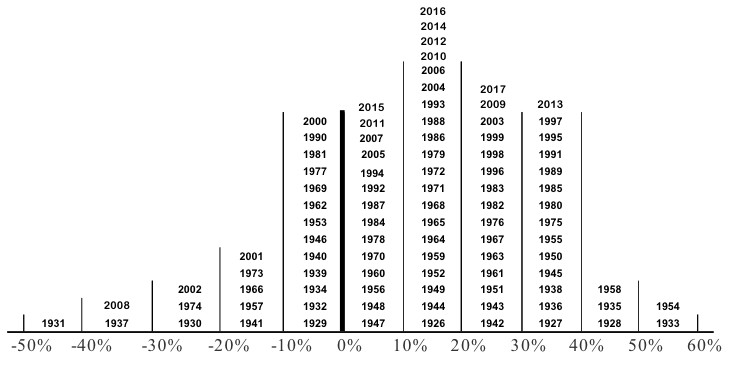

History reveals that annual U.S. stock market returns are adequately modeled as a random draw from a distribution such as that displayed in figure 1 below for the S&P 500. Year-to-year returns are uncorrelated; what happened the previous year is not predictive of the following year’s return. As a result, the best one can do is use the mean of the distribution as a forecast: 12% simple average or 10% compound return. While this sounds rather boring, 10% will have the lowest average forecast error for next year’s return and for the year after that and for the year after that. History reveals it is unnecessary to come up with a new return forecast each year!

Figure 1: S&P 500 Annual Returns: 1926-2017

Indexes are unmanaged and cannot be invested in directly.

Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

The term “expected return” refers to the mean of the distribution shown in figure 1. The yearly deviations from this mean are largely unforecastable, so the best we can do is use the mean as a forecast. The actual return will deviate from the mean due to unforeseen events during the year.

Robert Shiller’s research, for which he was awarded the 2013 Nobel Prize in economics, confirms this, showing that annual market volatility, as measured by standard deviation, has little to do with changing economic fundamentals, while having everything to do with investor emotions. Subsequent deviations from expectations are unpredictable as they are the result of collective emotional decisions.

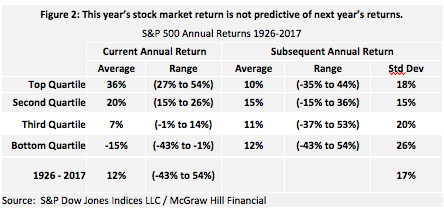

Figure 2 below provides additional evidence regarding the lack of return correlation from year-to-year and thus the futility of using last year’s return as a starting point for next year. It shows that regardless of whether the previous year’s return was awful or wonderful or simply run of the mill, the average return for the subsequent year is right around the 90-year average of 12%. If you take volatility drag into account, the expected annualized compound return is 10%, the number I provide when asked my opinion regarding the upcoming year’s market expectation.

Wisdom of crowds or groupthink?

There are two takes on the effectiveness of group predictions. The first, often referred to as the wisdom of crowds, has the collective efforts producing better outcomes than if individuals function alone. It works best when individuals provide their forecasts to the group sight-unseen by the other members of the group. The theory behind this approach is that each forecast is based on a common set of information, with each individual reaching a different conclusion due to random differences. When results are averaged, individual differences offset one another and the underlying “truth” is revealed.

But when individuals are able to communicate with one another prior to providing their estimates, the pernicious emotional force of groupthink develops. Wishing to be socially accepted, individuals alter their opinions to match those of others in the group. Strong personalities dominate and instead of random individual errors, the group ends up with a common error that does not washout when results are averaged. Research shows that in the face of groupthink (also referred to as consensus or herding), the quality of group estimates deteriorates rapidly.

The survey results are a dramatic example of the damage inflicted by groupthink. As I argued in an article last year, market gurus participate in a race to the bottom with respect to predicting market returns. They are loathe to be wrong on the downside and are cognizant that low forecasts garner more press coverage, so they fudge their numbers lower, making it more likely they will be picked up by the press as well as more likely to be wrong on the upside after the fact. These gamed predictions are widely reported and advisors, falling into the group-think trap as well, accept them as the starting point, even dropping their predictions further.

After multiple layers of emotional herding, we end up with the hard to reconcile return predictions reported by the survey. Unfortunately, this happens every year, with predictions often badly underestimating actual stock market returns. But like those weather forecasters who are so often wrong, even for a few days in advance, we are hooked on return predictions and take them seriously, even though the forecasting record is terrible.

Destroying long-horizon wealth

This would not be a problem if advisors did not take their own return forecasts seriously. But if they do, and construct retirement portfolios based on them, clients will be underinvested in stocks relative to bonds and long-horizon wealth will be destroyed. To illustrate, the survey reported a 10-year stock-bond return spread of 1%, when historically this spread has been five- to six-times larger.

Groupthink is dangerous to one’s wealth!

Like the 10-day-ahead weather forecast, beginning of the year return forecasts and surveys should not be taken seriously. The powerful emotions of groupthink destroy their usefulness for making investment decisions.

C. Thomas Howard is an Emeritus Professor of Finance at the University of Denver and Chief Investment Officer at AthenaInvest of Greenwood Village. He is the author of Behavioral Portfolio Management.

Read more articles by C. Thomas Howard, PhD