The 2018 Software Survey, conducted by Advisor Perspectives, Joel Bruckenstein at T3, and my firm, Inside Information, offered by far the most comprehensive data on the advisor tech landscape ever collected. In all, we received 1,554 useable responses, representing firms very small to very large, across a broad spectrum of experience in the business.

You can read the full report here.

The survey started by examining market share data – that is, the percentage of the total respondents who are using each of more than 300 different software programs and web-based services, broken down into 13 different categories:

All-In-One Programs (led by Morningstar Office and Envestnet/Tamarac)

Risk Tolerance Instruments (Riskalyze and FinaMetrica)

Portfolio Management Tools (PortfolioCenter, Envestnet/Tamarac, Morningstar Office, Orion Advisor Services)

Trading/Rebalancing Tools (iRebal, Envestnet/Tamarac)

Financial Planning Tools (MoneyGuidePro, eMoney)

CRM Tools (Wealthbox, Junxure, Redtail, Salesforce)

Document Management/Processing Tools (DocuSign, LaserApp)

Online Portfolio Management (“robo”) Tools (Schwab Intelligent Portfolios, Envestnet, Betterment Institutional, Folio Institutional)

Investment Data and Stress Testing Tools (DFA Returns; Riskalyze Stats/Scenarios)

Investment Data/Analytics Tools (Morningstar, fi360, YCharts)

Custodial Custody and Trading Platforms (numerous)

Cloud Hosting and Cybersecurity Providers (Rightsize Solutions, Entreda, True North Networks)

Miscellaneous Tools (SS Analyzer, MaxMyInterest, i65, WhealthCare)

In addition, we asked each user to rate the software tools and services they were using on a scale of 1 (probably replace) to 10 (highly recommend to my friends). The report provides average ratings for each software program and average category ratings, to see how satisfied users were with what they were using, and in general how satisfied the community is with each category.

A surprising number of programs/services scored above 7.0, which suggests that advisors today are generally satisfied with the functionality and feature set of their tech tools. A few programs achieved extraordinary average ratings at 8.00 or more, including iRebal (TDA free version) in the rebalancing category (8.32); Advyzon in the all-in-one category (8.08); eMoney in the financial planning group (8.00); Concenter Services/XLR8 among the CRM tools (8.65); DocuSign among the document management tools (8.21); and the trio of Kwanti/Portfolio Lab (8.56), the Bloomberg Terminal (8.52) and FactSet (8.03) in the investment data and analytics category.

The highest overall category rating (7.73) was found in the cloud hosting/cybersecurity group, where the highest rated services were True North Networks (8.83), and Rightsize Solutions (8.33).

Finally, we asked the survey participants which programs/services they’re looking at adding in the next 12 months – on the theory that this would provide us with an early warning system as to who will soon be gaining market share in their categories.

The programs and services that appear to be on the rise include:

Envestnet/Tamarac and Oranj (all-in-one)

Riskalyze and FinaMetrica (risk tolerance)

Orion Advisor Services (both portfolio management and trading/rebalancing)

eMoney, MoneyGuidePro and Right Capital (financial planning)

Redtail and Salesforce (CRM)

DocuSign (document management)

Schwab Intelligent Portfolios (online portfolio management)

Riskalyze Stats/Scenarios (investment data and portfolio stress testing)

YCharts (investment data and analytics)

True North Networks (cloud hosting/cybersecurity)

Whealthcare, SS Analyzer and MaxMyInterest (miscellaneous)

All of this information should be helpful to the advisor community as you sort through the bewildering range of options available to your firm, especially since so many of today’s options are either new or dramatically upgraded from the last time you viewed a demo. But bigger picture, what were some of the most surprising nuggets to be pulled out of this data?

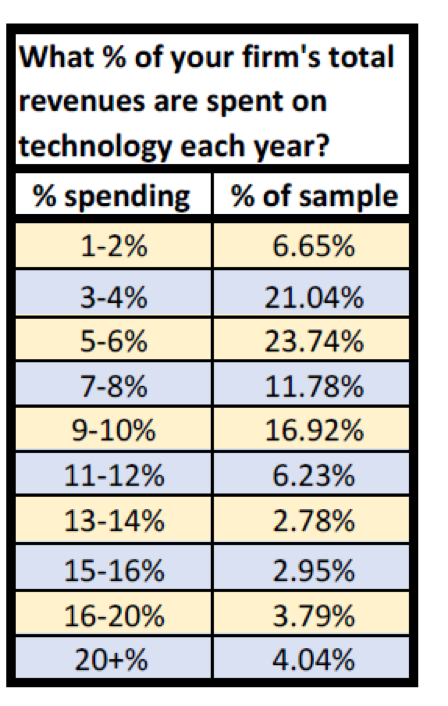

One thing that advisors might find surprising is the average “tech spend” in the industry. This result was not included in the survey writeup, but we asked survey participants to estimate how much of their total revenues are spent on technology (which includes hardware costs, software license fees and consultant fees) each year. The idea was to help the community determine roughly what their peers are spending, and whether their own expenditures are normal or within industry averages.

As you can see from the chart above, the industry in general exhibits a pretty wide spectrum of tech spending, but the sweet spot seems to be between 3% and 10% of top-line revenues, with no clear center of gravity within that range. Some firms are clearly more tech-reliant than others; a nontrivial 7.83% of respondents say they’re spending more than 16% of their revenues on technology-related costs, while at the other end of the spectrum, an abstemious 6.65% are spending between 1% and 2% of top-line revenues.

To get a closer look at this data, we broke the tech spending responses down by size of firm, and as you look at the next chart, you can see one explanation for those big spenders. Look to the upper right of the chart, and you see that the very smallest firms in the survey, with less than $100,000 in annual revenues (very small indeed, but surprisingly representing 10% of our respondents) have by far the highest percentage of big tech spenders. This almost certainly represents firms in the start-up phase, where they’re bringing in few revenues and spending everything they can muster to build out their tech stack.

For smaller firms generally, the expenditure sweet spot extends from 3% to 12%, with generally higher expenditures across the board. The largest firms, with over $4 million in revenues, huddle closer in the 3-8% range, with the center of gravity being around 4-6%. Only 11.43% of these larger firms are spending as much as 9-10% of revenues on technology, compared with roughly 20% of firms with under $500,000 in revenues. Some of the disparity can be attributed to economies of scale and buying power, but one might also expect that smaller firms are less inclined to stick with legacy systems, and are more likely to switch providers and look for new solutions as they come along.

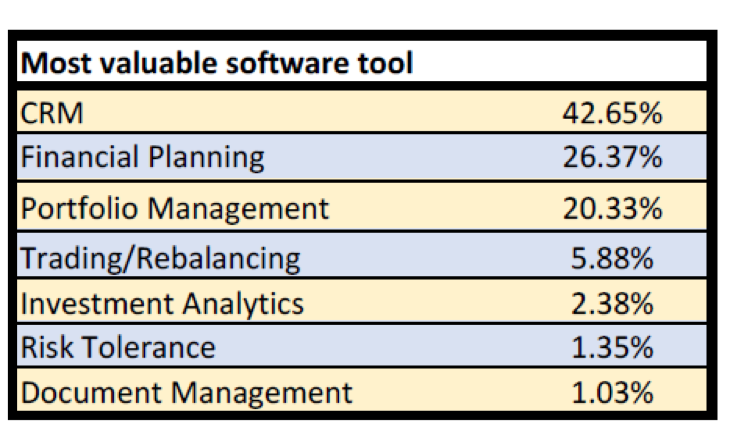

One of the most interesting questions to ask is: Which category of software is most valuable to you and your firm? As you can see from the graphic, 42.65% of our respondents view their CRM program as the all-important hub of their businesses. Financial planning finished second in this horse race, with 26.7% of respondents naming it the most important tool in their toolbox, while 20.33% view their portfolio management software as the key to their business. (The other categories finished distantly behind.)

Here again we took a deeper look at the responses, and found some surprising results. When the software preferences are correlated with experience – that is, with the number of years in the business – the picture looks very different for different cohorts. Advisors with more than six years tenure voted with the consensus; they view CRM as their most important tool. But notice in the chart that of advisors with 1-5 years in the business, only 22.44% feel the same way. Their program of choice: financial planning software, with 50.64% of the vote.

Interestingly, financial planning software has become increasingly less important to advisors as they age in the business, while portfolio management software exhibits the opposite trend.

What can we make of this? The data, from a robust sample, confirms anecdotal reports that younger advisors are more planning-focused and less interested in providing asset-management services than their older peers. Indeed, the Gen X/Y planning cohort has increasingly given up the AUM revenue model in favor of monthly or quarterly fees billed out of a client’s credit card or bank account. Portfolio management software therefore becomes much less relevant to their service model. Meanwhile, advisors with more time in the business are overwhelmingly working with older, wealthier clients, managing client assets and billing their revenues through their portfolio management software – which makes it more relevant.

But how can we explain the disparity in CRM usage? Younger (or newer) advisors may be more involved in onboarding new clients than maintaining client relationships. Financial planning software is by far the most important component of a new client onboarding process, while CRM’s value doesn’t fully manifest until an advisor is trying to stay on top of 150 longstanding relationships.

This raises the question: Is the chart reflecting disruptive trends in the industry, or is it an artifact of where advisors are in their professional careers? It will be interesting to see if today’s younger advisors, as they acquire clients and shift to relationship-maintenance mode, will value CRM more. And as their (probably younger) clients become wealthier and start to have portfolios to manage, will the portfolio management software become a more critical part of their business model? We may know more after the next survey. Or the one after that.

We want to thank the members of the Advisor Perspectives community who lent their time and perspective to our survey, and most importantly, we hope the community can benefit from the data and analysis that we’re able to provide. Staying on top of the ever-changing, ever-evolving software landscape is a challenge that you shouldn’t have to do in a vacuum.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com.

Read more articles by Bob Veres