Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In the past month, two well-known and highly respected money managers have made confident assertions about the markets. Their comments would lead one to believe that the future path of the market in the coming months is known. Sadly, many investors put blind faith in the words of high-profile, accomplished professionals and do little homework of their own. While we certainly respect the background, knowledge and success of these and many other professionals, we take exception with their latest advice.

Before the election In November 2016, were there investment professionals who claimed a Donald Trump victory would drive equity prices significantly higher? There were (very) few, they certainly were not publicly discussing it, and the broad consensus was overwhelmingly negative. In March of 2009, which professional investors were pounding the table claiming that the next decade would produce some of the greatest market returns in history? Again, while some may have thought valuations were fair at the time, few if any were raging bulls.

The two examples are not unique. More often than not, investor expectations fail to accurately anticipate the future. This is not about individual investors; it applies to the best and brightest. Despite the urge to heed the sage advice of the “pros,” we must remain objective, especially when everyone seems so certain about what will happen next.

The known future

Until the recent market volatility, the message from Wall Street analysts, media gurus and most investors was that stock prices will undoubtedly go up for the foreseeable future. Unbridled optimism about corporate earnings offer one point of fundamental justification for such views, but in large part those forecasts were predominantly based on the simple extrapolation of prior price trends. In late January 2018, a few esteemed Wall Street analysists actually raised their year-end S&P 500 price forecast from what they were only weeks prior. Although rationalized by stronger estimates of earnings expectations and an improving economic prognosis, the fact that January’s market rally had the S&P 500 already approaching their year-end forecast also played a meaningful role.

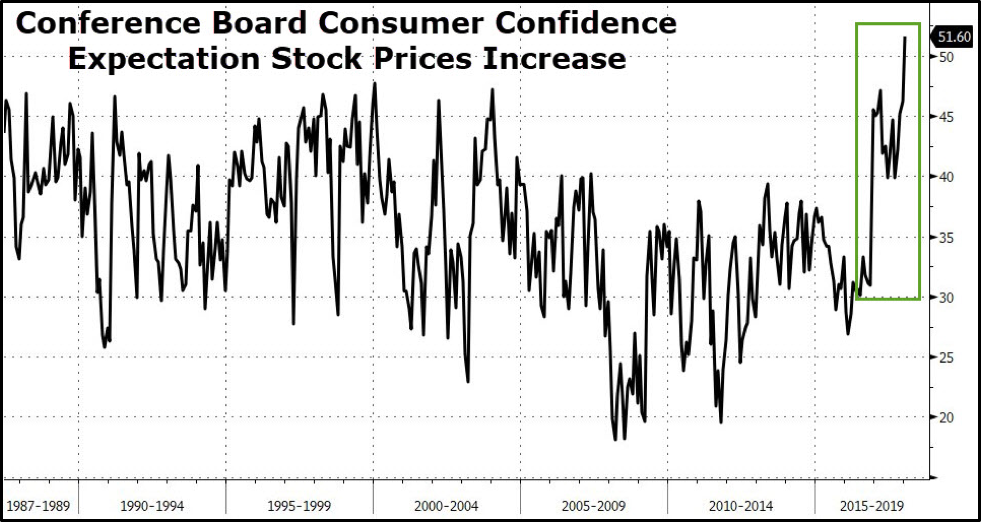

Basing future expectations on the most recent price activity is a great method of forecasting returns, until the trend changes. Wall Street analysts are not the only ones who were convinced that the recent trend would continue in the months ahead. The graph below shows that expectations for stock-price increases were higher than at any time since at least 1987.

This second table from Ronnie Stoeferle at Incrementum provides a broad gauge of the excessive bullishness in the markets.

While there are a slew of technical reasons to suspect the recent market dip may be a speed bump on the way to higher prices, there are some serious fundamental warnings along with geopolitical concerns that argue downside risks are being grossly ignored. We would avoid using the word certainty to describe a market or economic forecast, and given the juxtaposition of risks and excessive valuations, relying on the certainty of others is not a prudent way to build wealth.

Ray Dalio

The following quotes came from a recent interview with Ray Dalio:

- “We are in this Goldilocks period right now. Inflation isn't a problem. Growth is good, everything is pretty good with a big jolt of stimulation coming from changes in tax laws.”

- "There is a lot of cash on the sidelines. ... We're going to be inundated with cash," ... "If you're holding cash, you're going to feel pretty stupid.”

- Finally, he said he expects to see “a market blow-off” despite the economy being in the last legs of the economic growth cycle.

What could go wrong? Dalio, the billionaire founder of the world’s largest hedge fund, Bridgewater Associates, warns us that taking a conservative posture will make you “feel pretty stupid.”

There are four problems with these comments. First of all, does Dalio really believe that there is “cash on the sidelines”? For every buyer there is a seller. The concept of “money on the sidelines” does not hold in a free market economy. This is one of Lance Robert’s seven myths of investing.

Second, neither he nor anyone else knows what the future holds. Third, even if we presume him to be correct concerning the market, will he let you know when it’s time to sell stocks and hold cash? Keep in mind that wealth is compounded most effectively by not chasing markets higher but by avoiding large losses. Finally, Dalio almost certainly has hedges in place so that, even if he is wrong, his portfolio will have some cushion. Again, although we respect his insight and he may well be correct, it is concerning to hear a person of such influence potentially mislead investors into thinking the future is certain, and, worse, mocking those taking precautionary measures.

Jeremy Grantham

Grantham, also a very successful investment manager, has made similar comments as to how this bull market ends.

- “I recognize on one hand that this is one of the highest-priced markets in U.S. history. On the other hand, as a historian of the great equity bubbles, I also recognize that we are currently showing signs of entering the blow-off or melt-up phase of this very long bull market.”

- “A melt-up or end-phase of a bubble within the next six months to two years is likely, i.e., over 50%.”

Grantham has a perfect track record of calling out the equity bubbles of 2000 and 2008 well in advance. Further, he has stated unequivocally that equity valuations are excessive and investors should expect flat to negative returns over the longer term. Currently, his firm GMO is forecasting annualized inflation-adjusted returns of -4.4% for U.S. large-cap stocks over the next seven years. Despite the prospects of negative returns and wealth losses, he feels confident influencing others to chase a “melt-up” bubble that may last from six months to two years.

Dalio/Grantham wisdom

Both highly successful investors and thought leaders are telling the story of tenable market risks but tempting investors with the possibility of a grand finale worth chasing.

No one knows how this current bull market will end. Dalio and Grantham may be correct, and it may end with a melt-up, blow-off rally for the ages. On the other hand, it may have ended last week with the blow-off rally having occurred over the last year.

To put a historical perspective on how this market may top, the following charts compare the death of the NASDAQ 100 bull market in 2000 and the end to the S&P 500 bull market in 2007.

As shown, the topping of the last two bull markets took vastly different paths. Whether a blow-off rally as seen in the late 1990s, the one advocated by Grantham and Dalio, is the right call or a more frustrating rounded top of 2008 is the answer, we do not know. Left for consideration is whether the 37% rally since Trump's election was the blow-off top and, if so, has it reached its apex?

Summary

Dalio and Grantham’s ideas about how this ends have zero certitude. If their minds change, we will almost assuredly be the last to know. Although a cynical premise, could they be propping the market up with talk of a magnificent rally so they can reduce their own risk? There is abundant evidence this occurred in 2007 as the mortgage meltdown progressed, albeit with different protagonists. It is a fair question to ask in this instance.

Given current valuations, the risks are significant, and if history is any indication, we can be assured that this bull-run will end sooner rather than later. This is not a message encouraging you to ignore the thoughts of Dalio, Grantham or other successful investors. Rather, we remind you that you are solely responsible for the risks you take. Being a good fiduciary and worthy steward of wealth mandates that we understand the risks as highlighted by Dalio and Grantham and avoid being influenced by the consensus groupthink that often has an ulterior motive. We all know how that ends.

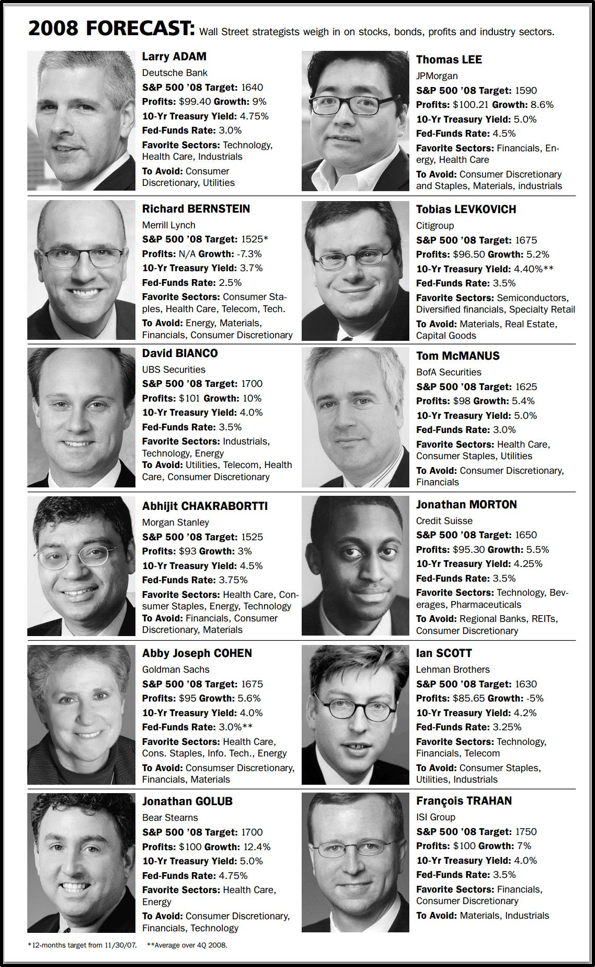

We leave you with the S&P 500 price projections from Wall Street’s best and brightest in 2008. For those who want to keep score, the S&P 500 closed at 902.4 at the end of 2008; profits were $17.45; the 10-year Treasury yield was 2.46%.

Michael Lebowitz is the founding partner of 720 Global, an investment consultant specializing in macroeconomic research, valuations, asset allocation and risk management. Our objective is to provide professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and marketing. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. 720 Global research is available for re-branding and customization for distribution to your clients. For more information about our services please contact us at 301.466.1204 or email [email protected].

Read more articles by Michael Lebowitz