Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Takeaways:

- Active equity fund performance depends on the stock picking skill of the investment team as well as current market conditions.

- Recent academic research confirms that returns to stock picking skill rises in tandem with increased stock return cross-sectional dispersion and skewness, along with greater market volatility.

- Active equity opportunity (AEO) is estimated using these measures to show how active the emotional crowds are at driving stock return dispersion.

- Returns-to-skill is strongly influenced by the current market environment as captured by Active Equity Opportunity.

- The impact of AEO on stock picking is largely independent of where we are in the business cycle.

- Returns-to-skill varies positively with the degree to which a fund is truly active, as measured by conviction, tracking error and size of assets under management.

- It may be beneficial to allocate more to stock picking funds and less to market exposure funds as AEO rises.

- When AEO is low, it still does not make sense to invest in closet indexers, since, while they outperform their truly active counterparts, their average alpha remains negative.

At the core of the active-passive debate is the question of whether active equity managers are skilled enough to cover costs. A large number of studies show the average fund underperforming a passively managed portfolio, revealing that stock-picking skill is on average insufficient to offset fees.

On the other hand, many studies demonstrate truly active funds, as contrasted to closet indexers, do outperform. Truly active funds are those with high active share, low R-squared with respect to the fund’s benchmark, smaller AUM (generally less than $1 billion), strategy consistency and large positions in best-idea stocks, among other identified fund characteristics. Unfortunately, distribution incentives strongly encourage funds to grow excessively large and become closet indexers, leading to the average industry underperformance, as closet indexers far outnumber truly active funds.

In recent years, however, many truly active funds have underperformed as well. This begs the question of whether the returns to stock-picking skill varies over time. Indeed, there is considerable anecdotal evidence that stock picking is effective in certain market environments and not in others.

Recent academic research confirms this evidence. In particular, several studies (here, here and here) show increasing cross-sectional stock dispersion (the cross sectional standard deviation of returns from either individual stocks or a portfolio of stocks), and VIX are predictive of increasing returns-to-skill. This study shows that positive skewness (the asymmetry of a probability distribution in which the curve appears distorted or skewed to the right) plays a major role in portfolio and market performance.

To help understand this relationship, consider a fishing analogy. A skilled fly fisherman knows the best time of day to fish, which fly to use given the conditions and where in the river to cast. But regardless of how skilled the fisherman is, if the fish are not biting, few, if any, will be caught. Successful fly fishing is a combination of skill and opportunity. Skill is the result of the fisherman’s talent and experience while opportunity is largely outside his control. Using the number of fish caught as an indication of skill is problematic.

Active equity opportunity

The studies above provide a basis for measuring how favorable or unfavorable the current market environment is for stock picking. They paint a picture in which the returns-to-skill rises in tandem with increased stock return cross-sectional dispersion and skewness, along with greater market volatility. That is, high levels of cross-sectional and longitudinal volatility is the “fish are biting” scenario preferred by stock pickers.

In order to estimate the impact of market conditions on stock picking returns, I propose active equity opportunity (AEO), a measure of how active the emotional crowds are driving individual stock-return dispersion. The more active the crowds, the greater the returns-to-skill are and vice versa. Active equity managers who build a strategy for harnessing a specific set of behavioral factors prefer a higher level of AEO, since it is more likely their high conviction picks will outperform. On the other hand, a low AEO foretells a period in which it will be difficult for even the most talented to beat their benchmark.

In order to estimate the impact of market conditions on stock picking returns, I propose active equity opportunity (AEO), a measure of how active the emotional crowds are driving individual stock-return dispersion. The more active the crowds, the greater the returns-to-skill are and vice versa. Active equity managers who build a strategy for harnessing a specific set of behavioral factors prefer a higher level of AEO, since it is more likely their high conviction picks will outperform. On the other hand, a low AEO foretells a period in which it will be difficult for even the most talented to beat their benchmark.

AEO is estimated using four components, listed here from most to least important:

- Individual stock cross-sectional standard deviation

- Individual stock cross-sectional skewness

- CBOE Volatility Index (VIX)

- Expected small stock premium1

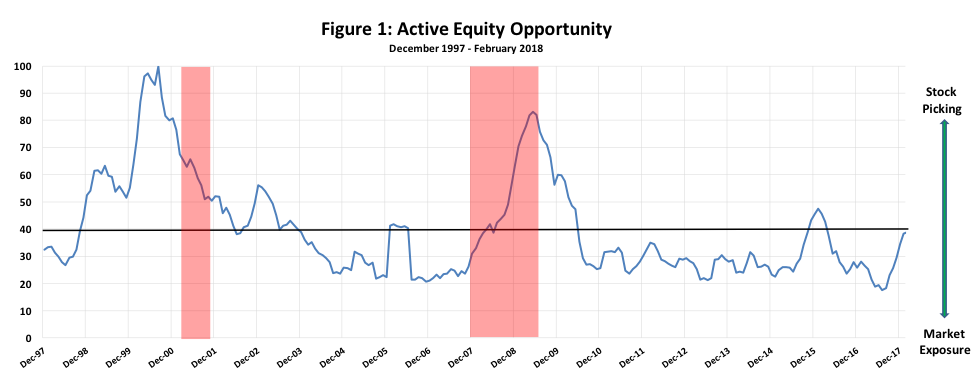

The resulting monthly values for AEO from December 1998 through February 2018 are presented in Figure 1. The average over this time-period is 40, which means values greater than 40 signal a better environment for stock picking while lower values signal a worse environment. During this 20-year time sample, 1998 through 2006 and 2008 through 2010 favored stock picking. Of particular interest is that since 2010, AEO has mostly been below average, declining to a low of 18 in mid-2017. It has since rebounded to 39 in early February 2018. This study, based on cross-sectional dispersion going back nearly 50 years, reveals that the mid-2017 AEOs were among the lowest in a half century. Going on eight years, stock pickers have faced a difficult environment in which to succeed. That is, fish have been biting less and less in recent years.

Sources: Morningstar and AthenaInvest

The red shaded areas represent NBER (National Bureau of Economic Research, the official arbitrator of business-cycle turning points) recessions. While there seems to be a relationship between recessions and higher levels of AEO, this study, based on a longer 1972 through 2013 fund sample, concludes that, “Overall, these results suggest that periods of elevated dispersion have a positive effect on alpha for the fund sample as a whole, beyond that coming from recessions. Further, the positive relation between fund activeness and performance is driven by return dispersion, as opposed to business cycle fluctuations.” In other words, the impact of AEO on stock picking is largely independent of where we are in the business cycle. Thus, trying to time portfolio changes in active equity fund holdings based on the business cycle alone is ineffective.

AEO impact on active equity performance predictors

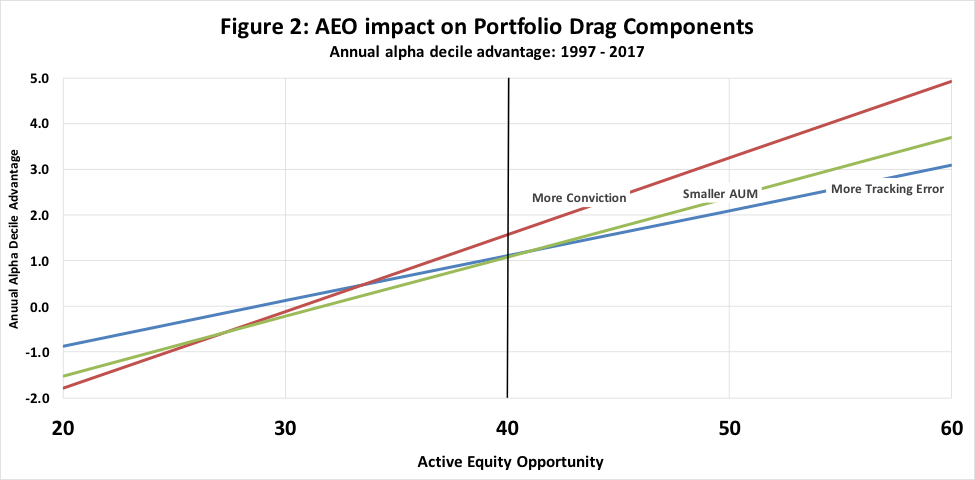

My previous research, reported here, presented criteria for identifying funds that are likely to outperform in the future, regardless of past performance. Figure 2 reports the impact of AEO on those criteria: conviction, asset size and tracking error. Conviction is measured as the portion of the portfolio invested in the top 10 relative-weight stocks (see here for information on how to calculate relative weights). For this exercise, the conviction range displayed is determined by sorting, each month, the fund universe into 10 deciles according to conviction, then taking the decile 10 conviction (highest conviction) average fund alpha (net of fees and benchmark return) minus the decile 1 (lowest conviction) average fund alpha.

Month-ahead alpha differences are calculated from January 1998 through May 2017 and regressed on the beginning of the month AEO in order to estimate the results displayed in Figure 2. All active equity mutual funds that existed in any month from January 1998 through May 2017 are included in the sample, resulting in over 230,000 fund-month observations. AUM and tracking error, the latter measured using benchmark R-squared, ranges are estimated in a similar way, except decile 10 alpha is subtracted from decile 1 so that all three measures display a positive AEO relationship.

Data sources: Morningstar, Lipper, Thomson-Reuters, and AthenaInvest.

Over the entire period, each of the three measures is predictive of future fund performance as evidenced by the positive average return advantage at the average AEO of 40. That is, funds with higher conviction, smaller AUM, and more tracking error outperform those at the opposite end of each scale. It is also the case that each return advantage varies with AEO, with predictive ability increasing as AEO increases and vice versa. Since each of these predictors is driven by stock picking skill, the observed variation is the result of AEO proxying for the returns-to-skill.

As AEO approaches 60, each of the predictors show strong intra-decile performance, ranging from 2.0% for high tracking error funds versus low, to 5.0% for the highest conviction funds. That is, the highest decile conviction funds outperform the lowest decile conviction funds by 5.0% when AEO is 60.

On the other hand, each of the three measures’ predictive ability reverses at some point as AEO drops. At AEO = 20, less convicted, larger AUM, and index-tracking funds outperform their opposite counterparts. So, what works for predicting fund performance when AEO is high is reversed when AEO is low. Again, this makes sense if each measure proxies for stock picking skill and as AEO declines, so does the returns-to-skill. The 20 to 60 range captures 85% of monthly AEO values over this 20-year period.

More direct measure of skill and returns-to-skill

The three measures just discussed represent proxies for stock picking skill as they capture the impact on equity fund performance and not, per say, the returns to the stocks held by a fund. A stock rating system, which I refer to as the best ideas of best funds (see here for details), provides a more direct measure of skill and returns-to-skill.

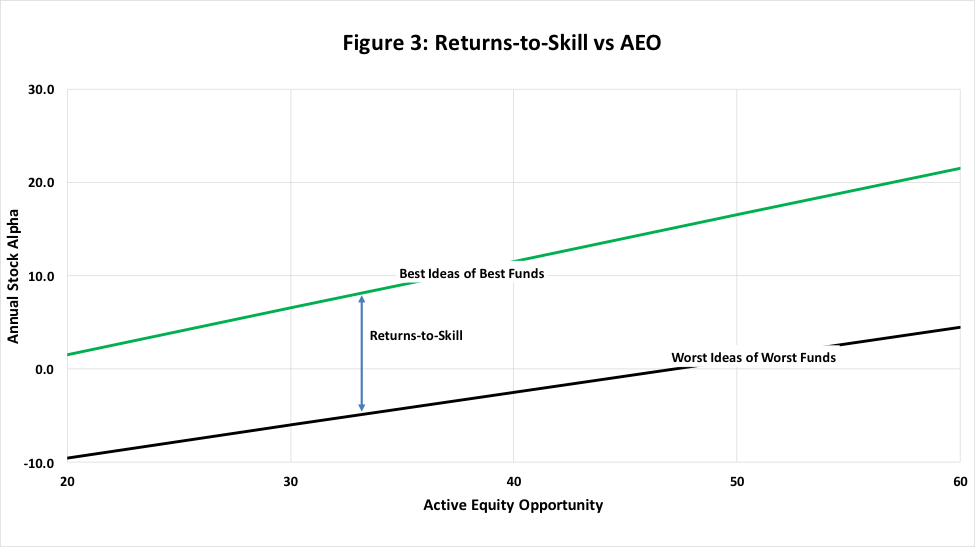

Figure 3 presents the impact of AEO on stock alpha (net of Fama and French market return) for the best ideas of the best funds (i.e. truly active) as well as the worst ideas of the worst funds (i.e. closet indexers). The best (about 10% of all stocks held by active equity funds) are those most held by strategy consistent, high conviction funds, while the worst are those most held by strategy inconsistent, low conviction funds. (See here for how strategy consistency and conviction are calculated). These measures focus on the desirable behaviors of fund managers and do not include past performance. Best and worst idea stocks are identified by aggregating fund relative holdings.

The sample upon which Figure 3 is based includes all stocks held by at least five active equity mutual funds from January 1998 through May 2017. The resulting sample comprises about half of stocks traded in the US and tens of millions of stock-fund-month observations. The reported results are from a regression of subsequent month stock alpha averages on month beginning AEO.

Data sources: Morningstar, Lipper, Thomson-Reuters, and AthenaInvest.

I define returns-to-skill as the difference between best idea alpha and worst idea alpha for each value of AEO. Note that for even low levels of AEO, skill remains strong, with differences averaging over 10%. Returns-to-skill increases as AEO increases, reaching 15% at AEO of 60. So regardless of AEO, fund managers display significant stock-picking skill.

However, as AEO drops, more and more stocks held by funds generate negative alpha. At AEO of 20, only the best ideas (top 10%) generate positive alpha while the other 90% sport a negative alpha.

This is one of the reasons why fund-predictor performance turns negative in Figure 2 at low AEO.

The fact that fund managers purchase stocks they know will likely generate negative alphas is the collateral damage inflicted by a fund distribution system demanding low tracking error, low volatility and small drawdowns. These incentives are the reason why so many truly active funds turn themselves into closet indexers.

Stock-picking skill is robust

Stock-picking skill and the returns to that skill exist no matter the current state of the economy and the market. As a result, investing in truly active funds over time produces a positive alpha. Once again, relying on criteria that reflects a fund’s true level of active management is important, and paying particular attention to the criteria that has proven to be predictive of future outperformance is especially important.

When AEO is low, it still does not make sense to invest in closet indexers, since, while they outperform their truly active counterparts, their average alpha is negative. On the other hand, there may be a benefit to allocating less to stock picking and more to market exposure as AEO declines. Holding tactical allocation equity funds that can adjust to market changes avoids the need to hold several market index funds that need to be traded as AEO changes. This study provides a test of portfolio timing using a measure of cross-sectional dispersion.

Returns-to-skill varies positively with the extent to which a fund is truly active and is strongly influenced by the market environment as captured by AEO. As AEO declines, even truly active funds struggle to beat their benchmarks, confirming the anecdotal evidence that stock picking is effective in certain markets while not in others.

C. Thomas Howard, PhD, is a professor emeritus at the Reiman School of Finance, University of Denver, and CEO and Chief Investment Officer of AthenaInvest, Inc.

1 Calculated as the difference between the small and large stock expected returns. See this study for more details.

Read more articles by C. Thomas Howard, PhD

In order to estimate the impact of market conditions on stock picking returns, I propose active equity opportunity (AEO), a measure of how active the emotional crowds are driving individual stock-return dispersion. The more active the crowds, the greater the returns-to-skill are and vice versa. Active equity managers who build a strategy for harnessing a specific set of behavioral factors prefer a higher level of AEO, since it is more likely their high conviction picks will outperform. On the other hand, a low AEO foretells a period in which it will be difficult for even the most talented to beat their benchmark.

In order to estimate the impact of market conditions on stock picking returns, I propose active equity opportunity (AEO), a measure of how active the emotional crowds are driving individual stock-return dispersion. The more active the crowds, the greater the returns-to-skill are and vice versa. Active equity managers who build a strategy for harnessing a specific set of behavioral factors prefer a higher level of AEO, since it is more likely their high conviction picks will outperform. On the other hand, a low AEO foretells a period in which it will be difficult for even the most talented to beat their benchmark.

Data sources: Morningstar, Lipper, Thomson-Reuters, and AthenaInvest.

Data sources: Morningstar, Lipper, Thomson-Reuters, and AthenaInvest.