“I have never seen a U-Haul parked next to a hearse.”

You can’t take your material possessions with you to your grave, as the above quote reminds us. On the heels of the recent tax reform, there seemed to be a frenzy to make charitable donations before bidding farewell to 2017. People who already had a donor-advised fund (DAF) might have found giving their 2018 donations ahead of the New Year a bit easier because they didn’t have to think about which charity would be the recipient of their gift. It’s taking the next step that will prove more challenging.

Here’s how to use DAFs to help clients use their wealth in the most meaningful way.

Clients don’t establish DAFs exclusively for the tax benefits. But that advantage is often why an advisor recommends a DAF. The driving force behind charitable vehicles is the desire to give. DAFs are for people who already have a philanthropic edge.

Yet, in speaking with actual or would-be donors, I hear a recurring question: “How do I decide who gets my money?” I have heard different answers to this question, like “think about whom or what made a difference in your life” and “look at who is asking and find out why.”

That’s solid advice, but there is more to it than that. Much more.

DAFs are ideal for people who want to give but haven’t decided where to give. Choosing among almost 1.1 million public charities and 1.5 million tax-exempt organizations in the U.S. is a daunting task. The numbers prove it. There was $85.15 billion sitting in DAFs at the end of 2016. That is after $15.75 billion went to charities – a significant amount. Yet there are so many people in need, so many important and necessary causes that need support; the dollars left in DAFs could resolve pressing problems addressed by the non-profit sector – everything from poverty and emergency relief to supporting health and education programs.

Enriching the client experience

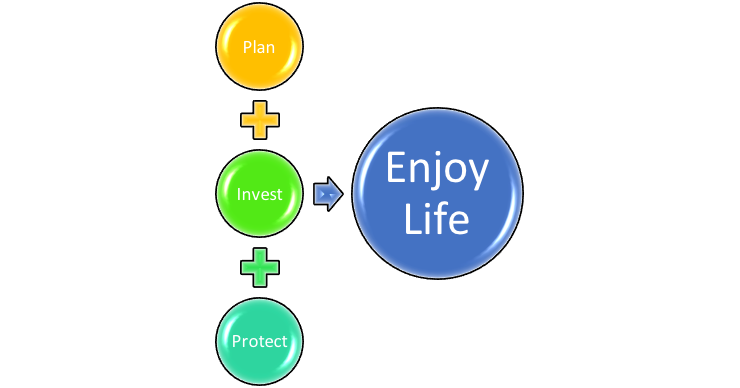

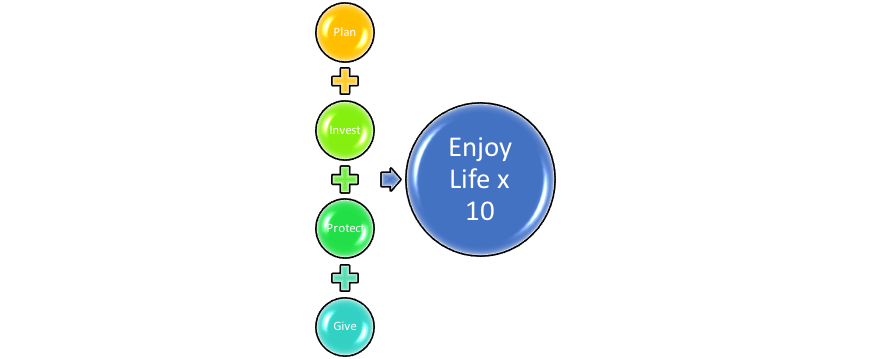

A positive client experience is key to our success. There are many ways to enhance our clients’ experience, from the scope of services we provide to how we deliver them. Yet, I have found that helping clients be intentional in everything related to finances, including their giving, goes far beyond the client-service experience to making a difference in the client-life experience. Even more so, helping clients identify the power giving can have in their life experience is one of the most significant things we can do for them. Figures 1 and 2 represent this in its most simple form.

Figure 1. Results-oriented planning and investment work

Figure 2. Intentional--oriented planning and investment work

A case study

Let’s say your clients, Susan and John Smith, are in their 50s. They have raised two children who are in their mid-20s who are pursuing successful careers of their own. The Smiths are on the verge of selling a business they built from scratch and to which they dedicated years of hard work. Their financial outlook is very positive, but they are anxious about how their lives are going to change once they are not working in the business. They will not only have substantial financial wealth; they will also have free time. Lots of it.

The Smiths have expressed an interest in giving back to their community and to helping people in need. This is a unique chance to take your relationship with the clients to a higher level. By going beyond needs and wants, you can help them live their legacies with intention.

The crossroad where Susan and John are in their lives is an ideal time to establish a DAF because they will protect some of the windfall from Uncle Sam and because charity is already part of the vernacular when they think about this new phase of their lives.

As their advisor and/or planner, you know Susan and John better than their other service professionals. That puts you in a unique position to help them find answers to their questions around giving back. But remember that the “how do I decide where my money goes” question is not a money question.

Decisive living

The giving question is one about making decisions that have impact. Life is a series of decisions we make and the outcomes or consequences of those decisions. Like with investments, where we choose to invest our time, attention and money, will give us the results we want if we are thoughtful and informed about how we will invest. This is what I call “decisive living” and why making smart decisions about giving matters.

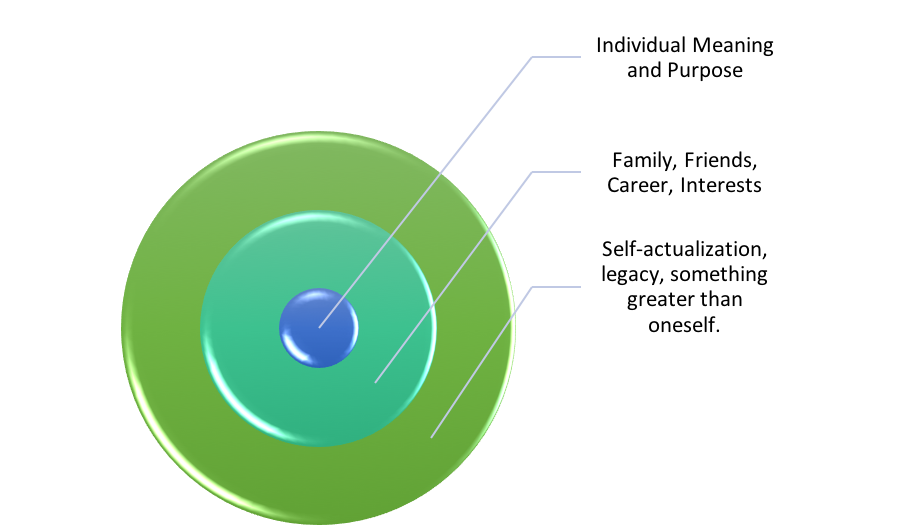

To begin understanding decisive living, let’s look at the ecosystem under which it operates.

Figure 3. Decisive living – The ecosystem

In Figure 3, you can see that decisive living is an interconnected system that involves different matters, participants and stages of life. The first requirement is the ability to make decisions, which is related to age and education. The second is to have options. Clients have both. This is important because planning is all about using the opportunity to make decisions to meet one’s goals and wants.

Those who don’t have a plan have made a decision too. They made the decision to hope for the best.

What does this have to do with making a difference and with giving? Everything. Because having a plan is where and how the introspective process of decisive living begins. I will take a quick step back, however, to acknowledge that the why has already been established. Within the ecosystem the answer to “why” is stated in many ways, like “to those who much has been given, much is expected,” “I believe in giving back,” “I want to make a difference because: “I seek self-actualization,” “I want to define my own legacy,” and/or “I believe that there is something greater than myself.” The latter gets into the spiritual aspects of giving back, but that is something for another time.

What kind of a plan am I talking about when I say planning is where decisive living begins? A giving plan? A making-a-difference plan? It is much more than that, yet simpler than it sounds. It is a life and legacy plan.

That means it is a plan for clients to maintain their lifestyles and fulfill their dreams. Sounds corny? Trite? Only if you have more than one life. And, by the way, if you do, please get back to me with your secret.

People plan for everything. Weddings are planned 12 to 18 months in advance. Planning for vacations, purchasing a new home a new car, another home, a boat and on and on it goes, is commonplace. Why, then, wouldn’t planning for how one lives make sense?

Decisive living is accomplished with a thorough plan for life that is flexible enough to adapt to ever-changing circumstances and has plenty of room for spontaneity. It ties the goal-setting aspect with the legacy aspect of a truly comprehensive life and legacy plan. As you set goals, you think about your purpose and how the goals fit into the greater picture of your life.

I often use what has become known at my office as “the boat example.” Having the goal of purchasing a boat for a couple to get together and have fun with their busy young adult children on weekends keeps in mind the greater picture. In this case, it is the importance of spending time as a family. The same goal within the scope of a hobby and having fun can also be part of the greater picture because hobbies and fun are key to a good life. However, having a goal of purchasing a boat to keep up with the Joneses is, well, just a goal.

Let me bring this back to the giving aspect of decisive living and how a DAF fits into the picture:

- Identifying what the greater picture or primary objectives of one’s life is up to each person. It’s about purpose, mission, la raison d’être, and not waiting for an unfortunate event to trigger the “why am I here” or “what’s the point” question.

- Setting goals is based on individual needs, wants, experiences, beliefs and outlooks.

- Making a difference is defined by one’s primary objectives. It will reveal the things that matter to each person.

- A DAF is a vehicle for making thoughtful giving tied to the greater picture (point 1).

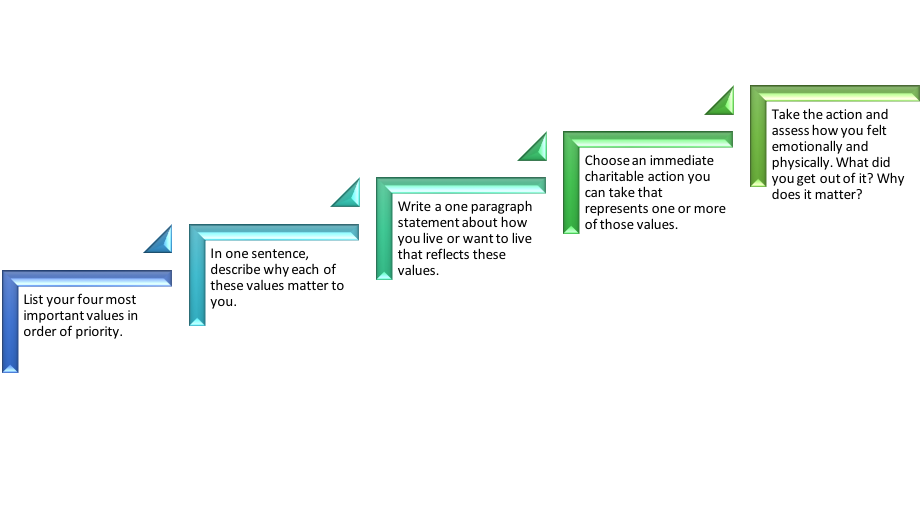

Most clients have noble purposes in life, which usually include things like having a good family life, educating their children and having a successful career. Yet there are so many more dimensions to each client’s life. A life event usually triggers thoughts of deeper meaning and self-actualization. This is where the process of decisive living plays a major role. For purposes of giving, the steps look something like this.

Figure 4. Instructions for clients to help them with their charitable interests.

Other steps follow, but describing how a client wants to live their legacy is the most personal aspect of the process. We must help clients recognize that legacies are to be lived. In simple terms, a living legacy is about living with intention and putting thought into our actions. In essence, much more than what one leaves behind, legacies are about things people do and how it makes others feel.

Here is an example of how someone, let’s say Susan, could describe her living legacy if she prioritizes the values of kindness and of validating others: “I like that people remember how you made them feel even if they don’t remember what you said. I want to be kind to others and for them to feel acknowledged when they are around me. I believe kindness goes a long way in a world of so many battles at so many levels.”

If John’s values were respect and hard work, his living legacy statement might sound more like this: “With hard work and respect for others people get very far. Work builds character and respect demonstrates you have character. This is something I have taught my children and I want others to know that too.”

These are simple yet powerful statements that together guide their giving not only in terms of how they direct their DAF, but also in how they spend their newly found “free time.”

Marcel V. Quiroga, RMA® is the founder and CEO of TQM Wealth Partners, a Massachusetts-based Registered Investment Advisor.

Sources:

National Philanthropic Trust, 2017 Donor-Advised Fund Report

National Center for Charitable Statistics, Quick Facts About Non Profits

Read more articles by Marcel Quiroga