Most research on retirement strategies assumes that people have saved adequately. But data on household savings shows that many households fall short, and will need to call on relatives or other sources for support. This raises questions about the best withdrawal or annuity strategies when savings are insufficient. It turns out that which strategy works best is different than for adequately funded retirements.

The motivation for this article came from an Advisor Perspectives commentary by Don Bennyhoff of Vanguard on estimating the return needed to achieve client retirement goals, and deciding on an appropriate asset allocation. In the APViewpoint discussion of the commentary, Larry Swedroe proposed an example of a financially constrained retirement and made the argument for a higher equity allocation to best meet retirement goals. In this article, I’ll use a slight variation of Swedroe’s example and test various asset allocations, as well as options that utilize annuities.

The example

The particular example I use is for a 65-year-old female with a remaining life expectancy of 25 years. I assume that she has $500,000 in retirement savings and will be receiving $30,000 per year from Social Security. I assume her living expenses are $60,000 per year. The analysis will be pre-tax and all dollar figures are in 2017 dollars.

I have deliberately designed this example to have a high probability of failure. I assume her savings are her only source for generating income – she cannot utilize home equity and she doesn’t have options for generating additional income or reducing expenses. An inflation-adjusted single-premium immediate annuity would not provide enough income to fill the $30,000 gap between Social Security and her living expenses, and we’ll see below that systematic withdrawal approaches run a high risk of failure. So unlike most retirement research where we look for ideal solutions, here we will try to find the “least-bad” alternative. I’ll assume that retirement shortfalls will need to be funded by relatives. This will broaden our focus beyond the retiree, since we need to evaluate financial consequences for the contributing relatives.

Stock allocation

If we assume that future stock returns will exceed bond returns, a solution might be able to tilt the asset allocation significantly to stocks. This relates to a required-return approach, as discussed in the Bennyhoff article mentioned above. But, in addition to average returns, the sequence of returns is also important, and raising the stock allocation also increases the volatility of outcomes. Another complicating consideration is that we don’t know how long the retiree will live. Given this mix of factors, let’s evaluate outcomes by doing some modeling.

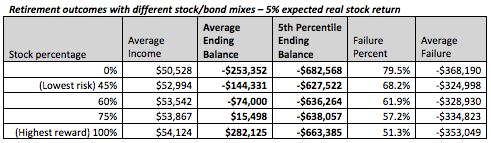

The chart below shows projected outcomes at different stock allocations. I’ve assumed that the individual in the example withdraws an inflation-adjusted $30,000 per year to cover living expenses and that such withdrawals continue until death or the funds run out. I ran 10,000 Monte Carlo projections for each asset allocation assuming arithmetic-average real-returns for stocks of 5% and 0% for bonds. These are lower than historical averages, reflecting my subjective assessment of current investment market conditions. (Standard deviations of annual returns were assumed to be 20% for stocks and 7% for bonds.) I also applied Monte Carlo analysis to longevity; the average age at death is 90, but that varies for each of the Monte Carlo runs in accordance with a mortality table.

Average income from the Monte Carlo runs fell below $60,000, reflecting instances where savings are depleted before death and income drops to the $30,000 of Social Security. The assumption is that relatives make up any shortfalls. Average ending balance is the measure I use for expected outcomes for relatives. Some of the Monte Carlo runs produce positive ending balances (bequests), while others generate negative balances that can be thought of as the total contributions from relatives. These positive and negative outcomes are combined into an overall average ending balance.

The 5th percentile ending balance is my risk measure. There’s a 5% chance that contributions from relatives will need to be more than this amount. As supplementary risk measures I also show the percentages of Monte Carlo runs that failed (resulted in a negative ending balance) and the average ending balance for those cases that failed.

As we would expect, increasing the stock allocation and thereby increasing expected returns, improves the average ending balance. With high stock allocations of 75% or 100% the mathematical expectation is that relatives would not have to contribute and would receive positive bequests. But we also have to evaluate risks by examining the 5th percentile column. For this particular example, the lowest risk is at a 45% stock allocation. But what is perhaps surprising is that the risk measure does not worsen much when we go to higher stock allocations, at least up to 75%. Given this risk/reward tradeoff, the preliminary conclusion is that a “least-bad” solution is to invest heavily in stocks.

The chart also shows that a heavier stock allocation also reduces the chance of failure and that the average failure does not worsen much at higher stock allocations. It is worth noting that, although all failure percentages are above 50%, average ending balances are positive with 75% and 100% stock allocations. The distribution of outcomes is skewed positively.

Lower stock returns

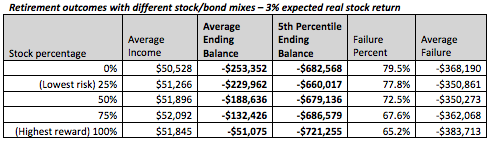

Some may be concerned that a projection of a 5% real return for stocks is too optimistic – considering that the cyclically-adjusted PE, or CAPE, stands at about double the long-term average of 17. The chart below is based on the same analysis as the previous chart, except the average real stock return is reduced from 5% to 3%, with the average real bond return still zero.

We see lower average income than before with less improvement from raising the stock allocation. The average ending balances are now all negative regardless of stock allocation and the spread in the balances from zero percent stocks to 100% is reduced. The lowest-risk 5th percentile balance is at 25% stocks and the additional risk from increasing the stock allocation is somewhat more severe. However, the risk at 75% stocks is not dramatically greater than at 25%, so a heavy stock allocation still makes sense, although going all the way to 100% may be too chancy.

Purchasing a SPIA

If the 5th percentile numbers based on stock/bond mixes cause too much concern, a possible strategy is to accept defeat and purchase an inflation-adjusted SPIA. In this case the relatives would pay a monthly or annual allowance to make up the shortfall. Based on rates from the pricing service CANNEX, a $500,000 inflation-adjusted SPIA would generate annual real income of $20,407, a payout rate of 4.08%. With $30,000 of Social Security income and the SPIA, the retiree comes up short by a real $9,593 each year. The result would be a sure loss for the relatives, but more predictable than using stock/bond mixes.

The above chart compares results for this SPIA strategy with a 100% stock allocation based on 5% average stock returns. Note that the 5th percentile ending balance for the SPIA is lower than the average balance, so there is some unpredictability with this strategy. This is because longevity is variable, so retirees who live longer than average will require larger total payments from relatives even though the periodic payments are fixed. Although this strategy is a certain loser for relatives with no possibility of a bequest, the 5th percentile risk measures are considerably reduced from those based on stock/bond mixes.

The 5th percentile result from this SPIA strategy is considerably better than from an all-bond strategy (compare to the top line of the first chart). The SPIA and all-bond strategies are fixed-income approaches that produce similar average ending balances, but the SPIA strategy provides the additional risk reduction benefit of longevity pooling.

The SPIA strategy clearly wins out over a conservative strategy with a heavy bond allocation, but compared to utilizing a heavy stock allocation, there is more of a risk/reward tradeoff. For those interested in a more in-depth discussion of this tradeoff, I recommend this article by Wade Pfau on risk pooling versus risk premium.

Another type of annuity

Rather than use a SPIA and lock in a sure loss, another possibility is to use a deferred-income annuity (DIA, also known as a “longevity annuity”) that provides delayed payments beginning late in life, and to take withdrawals from investments in the interim. The QLAC (qualified longevity annuity contract) is a government-sanctioned form of such a product, held inside a tax-sheltered account, such as an IRA.

Unfortunately there are no QLACs offered that provide inflation-adjustments from time of purchase. For this analysis, I assumed 3% inflation and used CANNEX to obtain the price for a QLAC that would pay $54,183 ($30,000 compounded at 3% for 20 years) beginning at age 85 with 3% annual increases thereafter. This particular QLAC would cost $158,433 for purchase at age 65, leaving $341,567 of the original $500,000 available to remain invested and (hopefully) provide for 20 years of $30,000 inflation-adjusted payments until the QLAC payments begin.

The chart below compares this QLAC strategy with the SPIA strategy and the 100% stocks base case. I assume that the funds not used for the QLAC would be 100% invested in stocks. It turns out that this QLAC strategy beats the SPIA both in terms of the average ending balance and the 5th percentile risk measure. In a previous article, I argued for a SPIA over a QLAC strategy for an adequately funded case, but, in this case when savings are inadequate, the best strategy is different.

Final word

I’ve provided a framework for evaluating how to deal with underfunded retirement plans and compared a few alternatives. There are many more strategies that could be studied, including: employing different withdrawal strategies, utilizing higher yielding fixed-income investments, purchasing options to set a floor on stock returns, utilizing more complex annuity products with lifetime withdrawal benefits, and various combinations of strategies. The key point is that the best strategies for these underfunded cases may differ from when there are adequate retirement savings.

Joe Tomlinson, an actuary and financial planner, is managing director of Tomlinson Financial Planning, LLC in Greenville, Maine. Most of his current work involves research and writing on financial planning and investment topics.

Read more articles by Joe Tomlinson