Those looking for an optimistic forecast for U.S. equities can turn to Northern Trust. Bob Browne, its chief investment officer, identified six themes that will drive the capital markets over the next five years. Taken together, they translate to 5.9% annual returns for U.S. stocks over that period, which includes 2017.

Those looking for an optimistic forecast for U.S. equities can turn to Northern Trust. Bob Browne, its chief investment officer, identified six themes that will drive the capital markets over the next five years. Taken together, they translate to 5.9% annual returns for U.S. stocks over that period, which includes 2017.

Browne spoke at the Schwab IMPACT conference in Chicago on November 15. He oversees much of the $1.1 trillion under management at Northern Trust.

Browne predicted that developed markets, exclusive of the U.S., will earn 6.8% and emerging markets will return 8.4%. Because U.S. markets have returned so well this year, with equities returning approximately 17% year-to-date, he said we are “stealing future returns” in 2017.

How does he get 5.9% returns with PE ratios starting at approximately 20?

Browne said that revenue growth would contribute 4.3% annually (consisting of 2% from inflation and 2.3% from nominal GDP growth), 1.9% from dividends and 0.9% from enhanced margins and stock buybacks. Those numbers add up to 7.1%, but he applied a 1.2% “haircut” to account for valuations (PE ratios) “normalizing” to get to 5.9%.

Browne is not predicting a recession in the U.S. over the next five years.

He said the emerging market returns will be higher mostly because of stronger revenue growth at 6.7%.

Here are the six themes that Browne said should matter to investors:

-

Entrenched growth – Economic expansion will continue globally, but at a modest rate by historical standards. Browne said that U.S. and other developed economies are in a growth “channel” and that means that there will be “fewer reasons to tighten monetary policy.” High debt levels will prevent a breakout to the upside, he said, and will keep monetary policy relatively easy.

-

Waiting for monetary Godot – Browne said Beckett’s Waiting for Godot is a metaphor for the fact that those waiting for a return to the pre-crisis era of monetary policy will be disappointed. Instead, he said, the watchwords of monetary policy will be patience, gradualism and communication.

-

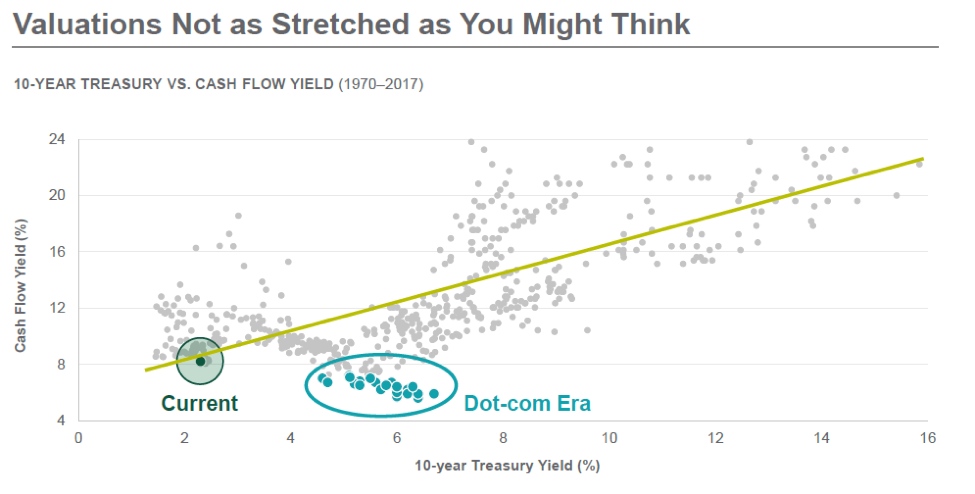

Valuation superstructure – Browne said there is a structural reason why PE ratios should be higher, but not extremely higher, than historical averages. Industries such as information technology, consumer discretionary, healthcare and consumer staples should drive higher margins across the economy. Those industries went from 37% to 50% of the market in the last 10 years, he said, which explains 1.5% of the increase in PE ratios.

Browne showed a graph of 10-year Treasury yield versus the cash-flow yield for stocks (which he said is the best proxy for the value of equities):

There is a strong linear relationship, Browne said. “Both are low by historical standards, as opposed to dot-com era, when cash-flow yields were lower than now despite higher Treasury yields.”

Browne said that rates are not going higher due to slow growth and “stuckflation” (see below). The macro theme of the past eight years was quantitative easing (QE) – zero-rates and clear communication of policies, according to Browne. “This has driven our risk-on view for years,” he said.

Browne expressed concern that the Fed would make a mistake, such as seeing that inflation is different from what he believes it is. “People keep missing this key point,” he said.

Browne is not worried about a 5% correction in the market, which he said happens about every 10 weeks – “it really is noise.” “The bigger risk is overreacting, thinking it is the start of a 20% correction,” he said.

-

Stuckflation – “There is a risk of cyclical upticks in inflation,” Browne said. However, he does not believe long term inflation will exceed 2%. The primary forces driving this “stuckflation” are an aging workforce and automation, which he said are not short-term phenomena; they are structurally deflationary forces, according to Browne.

-

Populist catharsis – This goes beyond Trump’s election, Browne said, in that Japanese Prime Minister Abe is following a populist theme. “Politics will have a bigger role in the markets,” he said, which affects whether or how investors will get paid. Volatility in the ballot box will lead to volatility in policies, according to Browne.

-

Regulation in the limelight – Investors should expect “smarter” regulation over the next five years, Browne said, which would also be more business-friendly. Expect the Senate to review Dodd Frank, according to Browne, who added that Emanuel Macron has taken similar steps in France. “It is more important to understand what is pro-growth versus cabinet appointments,” Browne said.

Browne stressed that markets are “very much in a risk-on” mode, but that investors should position themselves in a diversified, global manner. He noted that U.S. equities had outperformed other developed and emerging markets over the last seven years, but that streak is likely to end in 2017.

He disclosed that his firm is overweight U.S. high-yield bonds and developed markets ex-U.S. by 5% each, and is overweight U.S. equities by 3% and emerging markets by 2%. He is underweight U.S. investment-grade bonds by 13% and emerging-market debt by 2%

More Schwab IMPACT Conference Topics >

Those looking for an optimistic forecast for U.S. equities can turn to Northern Trust. Bob Browne, its chief investment officer, identified six themes that will drive the capital markets over the next five years. Taken together, they translate to 5.9% annual returns for U.S. stocks over that period, which includes 2017.

Those looking for an optimistic forecast for U.S. equities can turn to Northern Trust. Bob Browne, its chief investment officer, identified six themes that will drive the capital markets over the next five years. Taken together, they translate to 5.9% annual returns for U.S. stocks over that period, which includes 2017.