My Proposed Bet with Buffett

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is not an official bet. I’m not interested in documenting all the potential details that would be involved, and I don’t have $1 million to wager. Moreover, licensed firms are not allowed to make public fund recommendations, so the details of an official bet would have to be private and that won’t work for my purposes. I’m interested in taking a stand on how investors should think about the investment problem based on core principles like risk parity and factors. This article details how I would think about the problem. While I don’t recommend any specific funds, I do recommend a basic strategy that I am confident will serve investors’ objectives much better than a concentrated investment in stocks over the next decade or so.

History of the Buffett bet

In 2008 Warren Buffett proposed a public bet to show that actively managed investment products, plagued by high fees, would not live up to the goal of beating a passive investment in the Vanguard S&P 500 ETF over the subsequent decade. Only one person had the intellectual conviction to represent the active management side of the bet. Ted Seides at Protégé Partners LLC, a fund-of-hedge-funds firm, placed a $1 million bet that a diversified basket of hedge funds (in fund-of-fund structures) would outperform U.S. stocks from January 1, 2008 through December 31, 2017.

In a letter posted to Bloomberg earlier this year, Seides acknowledged that, with just eight months to go in the bet, “for all intents and purposes, the game is over. I lost.”

But the outcome wasn’t always so certain. Over the first 14 months after Buffett and Seides sealed the wager the S&P 500 lost over half its value. In fact, U.S. stocks lagged Seides’ fund-of-funds portfolio for almost five years before finally pulling ahead in 2014.

Why would anyone bet against Warren Buffett? Seides cited some very good reasons for why he felt such a bet was skewed in his favor at the time. But his primary reasoning was based on market valuations. When Seides agreed to the bet, U.S. stocks were trading at high valuations that had only been observed about 10% of the time over the previous 140 years. That 10% included the months before the Great Depression, and a few years toward the end of the technology bubble in the late 1990s. Both periods subsequently saw stocks produce returns well below their long-term average. Seides felt the historical precedent stacked the odds in his favor.

Of course, Seides’ forecast turned out to be wrong over the bet’s ten-year horizon. U.S. stocks have produced 8% compound returns per year from January 1st, 2008 through September 30, 2017. At last check (May 2017) Seides’ fund-of-funds portfolio had generated less than 3% per year net of fees.

Seides’ rationale for taking the bet was reasonably sound at the time. Markets were very expensive, and history would have guided toward lower future returns. In fact, after enduring one of the worst bear markets in history soon after the bet was struck, it took a run back up to nosebleed levels of valuation at the end of the period to pull Buffett’s side of the bet so far ahead. According to some of the more useful valuation metrics, such as the Shiller CAPE, markets are currently 50%-75% overvalued relative to long-term trend valuations. Moreover, while U.S. markets fully recovered from the epic collapse in 2008 (and more), other major markets were not nearly so fortunate. For example, the Vanguard FTSE All-World ex-US Index fund generated just 1.2% per year over the same horizon.

Figure 1. Vanguard S&P 500 Index fund vs. Vanguard FTSE All-World Index fund total returns, January 1, 2008 – September 30, 2017

Source: ReSolve Asset Management. Data from CSI.

Seides faced one other major headwind with his bet. While we don’t have access to the specific constitution of his portfolio, we can be confident that his diversified portfolio of hedge-funds had a volatility well below that of the S&P 500. In fact, the volatility of the fund-of-funds portfolio was probably about 5% annualized, about one-fifth of the volatility observed in the S&P 500 over the same period. Had Seides scaled exposure to his portfolio so that it approximated the same risk as U.S. stocks, it’s likely that the competition would have been much closer. In fact, there’s a good chance Seides might have won his bet after all.

A new wager

Earlier this year I raised the prospect with my partners of issuing a new bet with Buffett based on a portfolio oriented around risk parity and factors. As mentioned above, U.S. stocks have pushed well into the same nosebleed valuation territory as Seides identified in 2007. For investors to achieve the same results as they achieved over the past 10 years in the next decade, we will have to experience a third major bubble in a row. As a result, investors with material allocations to U.S. equity-linked strategies are going to be disappointed with their returns over the next decade or so.

There is a broad consensus across many credible sources, including AQR, Research Affiliates, and even Jack Bogle at Vanguard, that traditional U.S.-oriented portfolios will have low returns over the next decade or more. I expect U.S. bonds to produce about 2% nominal returns over the next 10 years, while stocks are likely to generate between 2% and 5% nominal through 2030. Meanwhile, the duration of U.S. bonds, a common measure of bond risk, is near the top of its historical range, while stocks are more susceptible to the type of crashes we saw in 2000 and 2008 when they are trading at such expensive valuations.

As a result, I favor a portfolio framework based on global risk parity and academic factor strategies, which offers a greater likelihood of producing the returns investors need, with less risk than they would be taking with a concentrated investment in the S&P 500 index. Remember, I define risk as the probability of not achieving financial objectives. My proposed portfolio, described below, does a pretty good job of minimizing this risk over the next ten or fifteen years, given the tools at our disposal in the current environment.

Risk parity and factors

My approach starts with a comprehensive focus on diversification. Remember, diversification requires a thoughtful combination of both diversity and balance. A diverse universe of investments will have assets that are designed to thrive in all of the major economic environments, not just environments that are favorable to stocks. That means we need to complement the investments that are typically found in portfolios with assets like commodities and gold, global government bonds, inflation-protected securities like TIPS, and emerging-market securities.

Fortunately, while developed-market stocks and bonds are expensive, emerging-market stocks, bonds, and currencies are priced for significantly better returns. It is not my intention to make a formal call on the relative merits of some assets over others, but to ensure all major asset classes are represented, including those that are often ignored. We aren’t in the business of forecasting, we are in the business of being prepared.

Of course, some of these diverse asset classes are much more volatile than others, so we need to be thoughtful about how we bring them together in a portfolio. Our objective will be to ensure each major asset class has an equal ability to express its unique character, so that the portfolio is designed to be resilient to any economic future. The portfolio strategy that optimizes the benefits of diversification by maximizing both diversity and balance is called risk parity. Thus risk parity funds will form a large part of our fund-of-funds portfolio.

The concept of diversification can extend to other sources of return that behave differently than the major asset classes themselves. It is well documented that investors in most countries around the world have a strong preference to own the stock and debt of their own domestic companies. This home bias is one of the strongest and most pervasive effects in markets. Many investors also express a preference for “lottery ticket”-type investments, and investments that are popular or appear to have a good “story.” Investors also take comfort in holding portfolios that are consistent with their peer group because the pain of underperforming their friends is much more intense than the joy of outperforming them. Investors are often slow to adapt to new information, and are prone to extrapolate intermediate-term trends, while underestimating the tendency of corporate or economic prospects to revert to the mean. Most investors are also averse to the use of leverage; avoid taking short positions; and chase performance at precisely the wrong horizon. They also overpay for insurance against large short-term losses.

These behaviors are universal, and are observed at the highest ranks of the most sophisticated organizations. Most investment capital is still guided by humans, and humans can be counted on to consistently behave in certain ways.

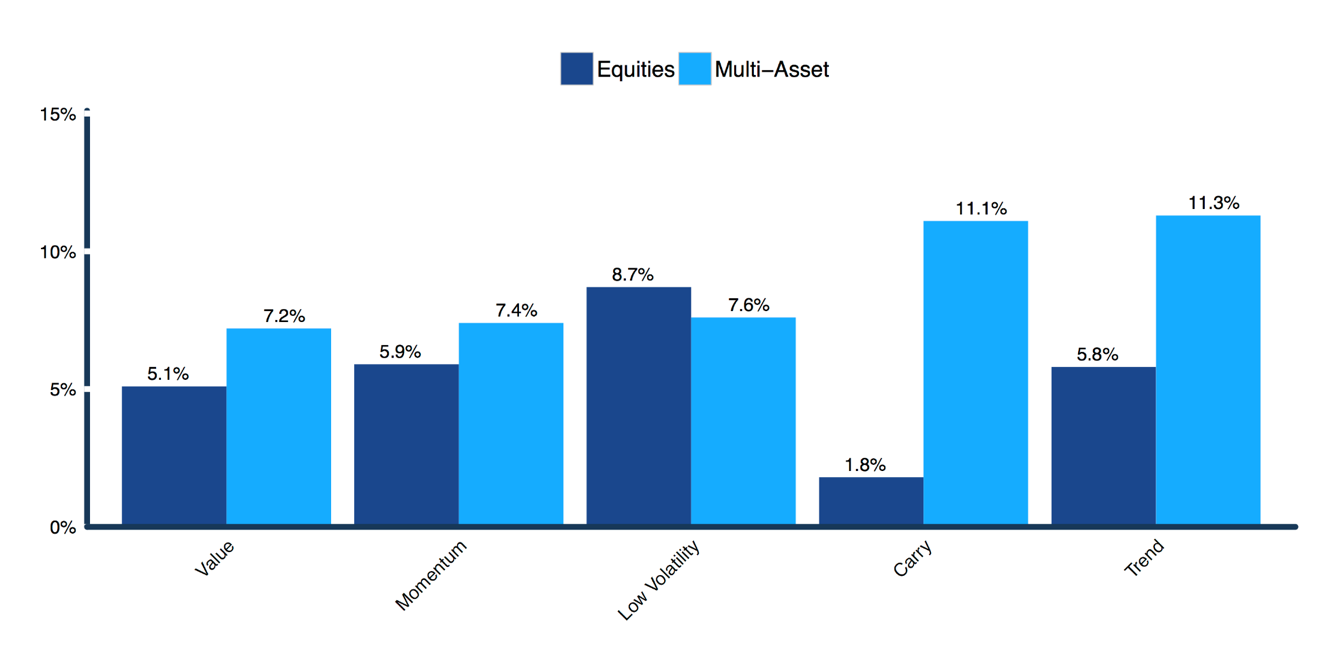

It turns out that the systematic errors above manifest in economically large effects across global markets. These effects, which academics call “factors” and many practitioners call “style premia” explain a very large portion of the differences in returns across groups of securities. If a large portion of investors can be counted on to behave in ways that leave profits on the table, then there is an opportunity for other investors – factor investors – to earn excess profits by taking the other side of those trades. And these excess profits can be very attractive. Figure 2 describes the long-term gross excess returns to these factors based on the literature.

Figure 2. Excess annualized historical returns to long-short factor portfolios formed from individual securities (Equities) and asset classes (Multi-Asset) scaled to 10% ex post volatility.

Source: Value and Momentum data from Asness, Moskowitz & Pedersen “Value and Momentum Everywhere” (2013). Carry (dividend) equity factor is for U.S. only from Ken French database (long top decile value-weighted, short bottom decile value-weighted for stocks in top 30% by market capitalization). Carry factor is from Koijen et al., “Carry” (2013). Defensive factor data from Frazzini & Pedersen, “Betting Against Beta” (2014). Equity trend data from “The Enduring Effect of Time-Series Momentum on Stock Returns over nearly 100-Years” by D’Souza et al. (2015). Multi-asset trend data from Hurst, Ooi, and Pedersen, “A Century of Evidence on Trend-Following Investing” (2017).

Source: Value and Momentum data from Asness, Moskowitz & Pedersen “Value and Momentum Everywhere” (2013). Carry (dividend) equity factor is for U.S. only from Ken French database (long top decile value-weighted, short bottom decile value-weighted for stocks in top 30% by market capitalization). Carry factor is from Koijen et al., “Carry” (2013). Defensive factor data from Frazzini & Pedersen, “Betting Against Beta” (2014). Equity trend data from “The Enduring Effect of Time-Series Momentum on Stock Returns over nearly 100-Years” by D’Souza et al. (2015). Multi-asset trend data from Hurst, Ooi, and Pedersen, “A Century of Evidence on Trend-Following Investing” (2017).

Many investors will be familiar with some of these investment factors or “styles”. The value investing style is especially popular, made famous by such lionized investors as Benjamin Graham and his protégé, Warren Buffett (though neither Graham nor Buffett invested according to contemporary, quantitative systematic-value methods). Other styles are more obscure, but no less powerful in terms of their historical results. Momentum, also known as “relative strength”, is the tendency for assets with high returns over the past few months to outperform assets with low returns. Several behavioral phenomena contribute to this effect, including the tendency for investors to herd; the fact that it takes investors some time to adjust prices to account for new information; and behavioral biases that compel investors to dispose of assets with gains too soon, while failing to dispose of assets with losses. The momentum strategy takes a long position in assets with the strongest returns, and shorts assets with the worst returns over the past 12 months (with a skip month).

The low-beta or low-volatility premium arises from the tendency for investors to avoid leverage, and overprice lottery type investments. As a result, lower volatility assets tend to outperform higher volatility assets on a risk-adjusted basis. “Carry” is the return that an investor would earn on an asset if the price didn’t change. For example, an equity investor might receive dividends, and a bond investor would receive a coupon. Commodities and currencies also offer carry, in the form of futures “roll yield” and interest rate differentials. Finally, the trend factor capitalizes on the tendency for assets with rising (falling) prices over the past few months to continue moving higher (lower) over the subsequent few weeks. This strategy goes long assets with positive excess returns over the past few months, and short assets with negative excess returns.

Unfortunately, most investors attempt to harvest exposure to these factors using severely diluted “smart beta” products, like the iShares Russell 1000 Value ETF (IWD), or the Vanguard Value Index fund (VIVAX). The returns to these funds are over 90% explained by simple exposure to the S&P 500, which means their “value” exposure is almost meaningless to long-term returns. Even the popular DFA Small-Cap Value fund is over 70% explained by the returns to broad U.S. stocks (source). Investors need access to new products that isolate the true uncorrelated opportunities afforded by these powerful premia.

While certain hedge funds have been profiting from long-short exposure to these alternative premia for decades, it has been challenging for most investors to take advantage. Fortunately, flattering returns from passive indexing strategies have compelled the traditional active management industry to innovate and focus on strategies with the most differentiated value. As a result, investors now have at their disposal a rich array of reasonably priced, accessible strategies that offer pure exposure to the most persistent, pervasive, and significant alternative return premia.

A handful of other firms (including ReSolve) run strategies that allocate to diversified sleeves of the most persistent, pervasive and economically significant long-short style premia. One such strategy run by AQR allocates to value, momentum, low beta, and carry. The strategy achieves this exposure by forming market-neutral long and short portfolios on both individual securities and global stock, bond, commodity and currency indexes consistent with the underlying factor definitions. Since the strategy exclusively uses long-short portfolios in global assets classes, it is completely uncorrelated with traditional asset class premia, like stocks, bonds and commodities.

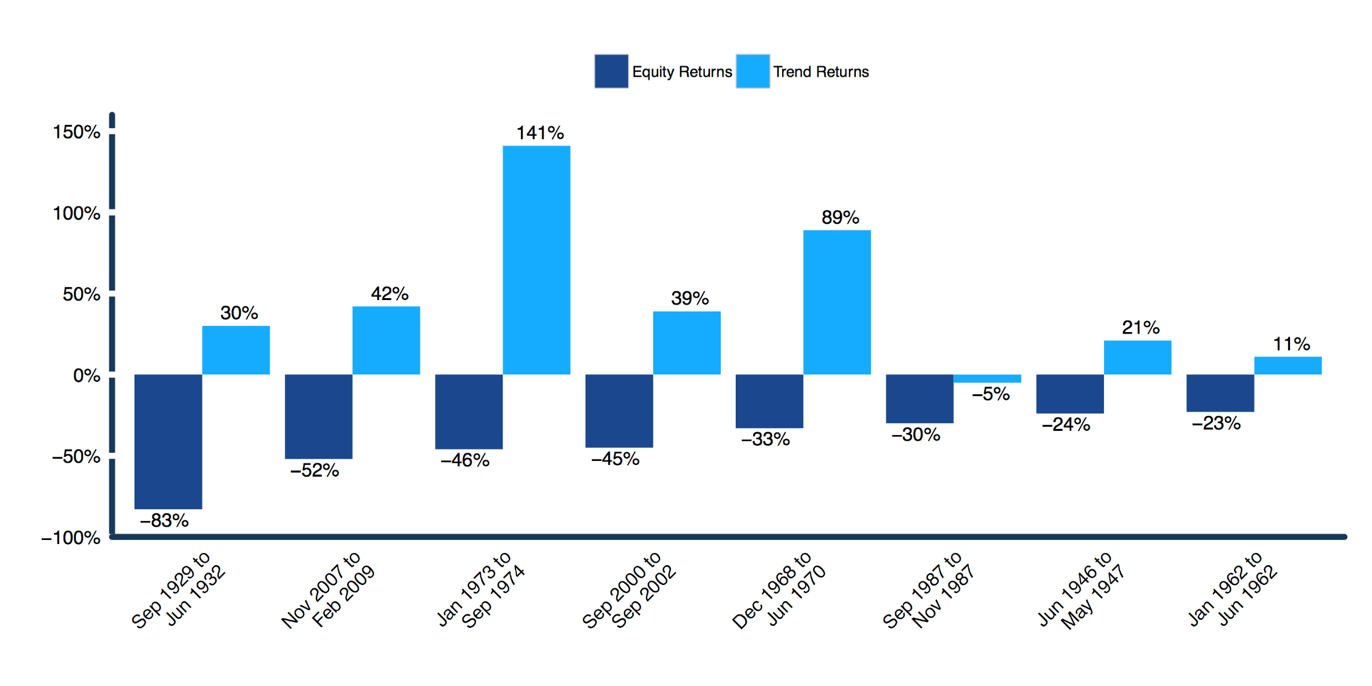

Many diversified style premia strategies separate out exposure to trend, because investors typically like to customize their exposure to this factor. Trend is particularly attractive as a diversifier for other sources of return, because it has a history of producing some of its best days, months and years when other strategies are struggling. Figure 3 shows the cumulative returns to the global trend factor during the eight worst equity market declines since 1926. The mean return to equities during the eight worst periods is negative 46%, while the mean return to the trend factor is +42%. While there is no guarantee the trend factor will serve the same hedge function in the future, history strongly suggests that trend is an attractive exposure to have in your portfolio during crisis periods.

Figure 3. Trend factor returns during the eight worst U.S. equity market declines, Monthly 1926 – 2017

Source: U.S. equity returns sourced from Ken French data library (Mkt + Rf). Multi-asset trend data from Hurst, Ooi, and Pedersen, “A Century of Evidence on Trend-Following Investing” (2017)

Source: U.S. equity returns sourced from Ken French data library (Mkt + Rf). Multi-asset trend data from Hurst, Ooi, and Pedersen, “A Century of Evidence on Trend-Following Investing” (2017)

Buffett bet portfolio

To reiterate, my overarching objective is to maximize diversification across as many independent, persistent, pervasive, economically significant sources of return as we can access in public markets. In short, I am advocating a portfolio based on risk parity and factors. Specifically, I want exposure to diversified funds of global asset classes, as well as style premia and trend. I want to hold these sources of return so that they all contribute approximately the same total risk to the portfolio. If I hold assets with similar expected Sharpe ratios in equal risk, this portfolio will have the highest ex-ante Sharpe ratio; in other words, it is the most mean-variance efficient portfolio that we can construct.

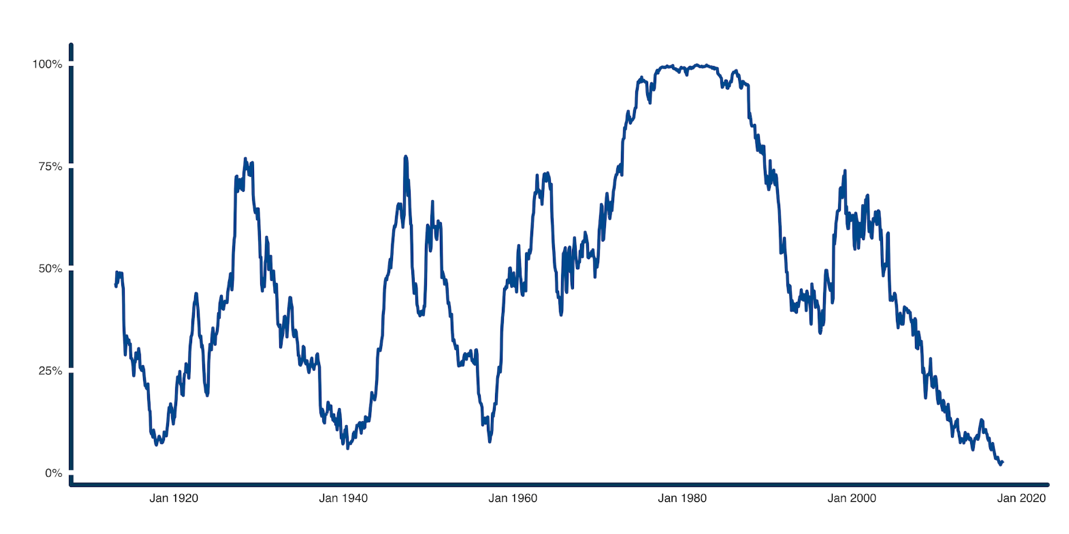

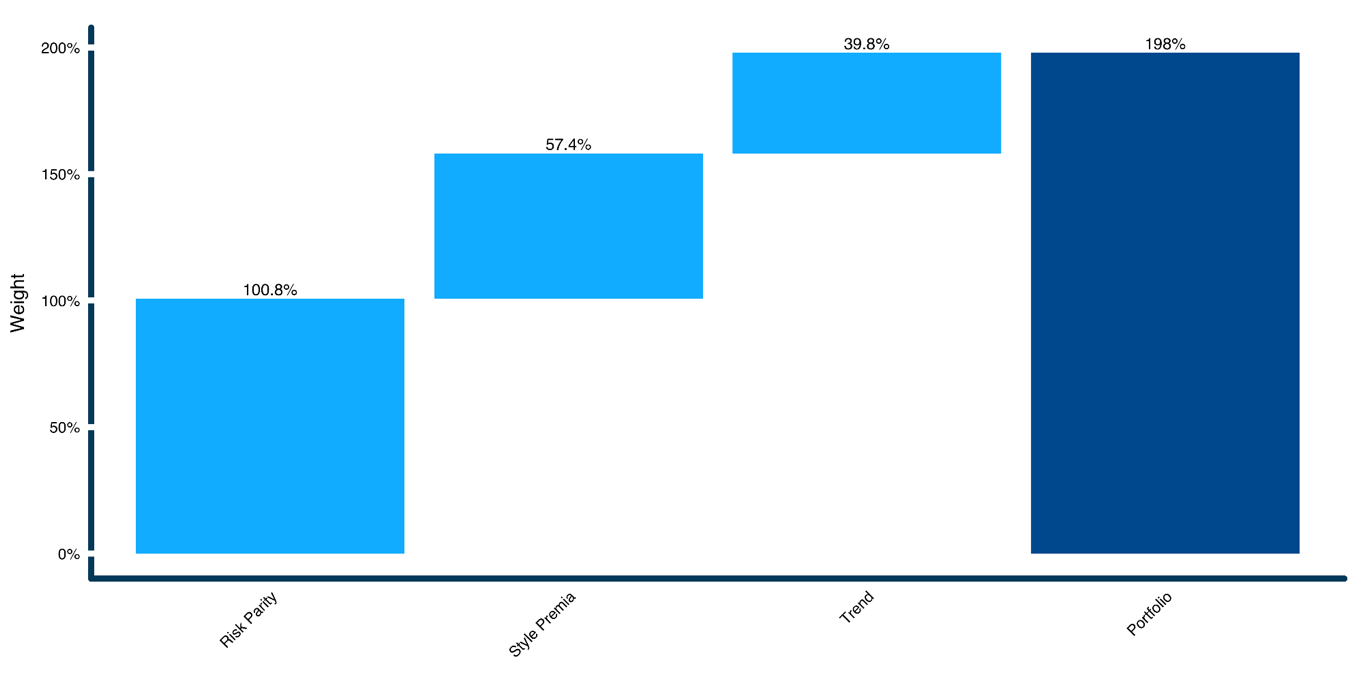

Our portfolio will combine exposure to traditional asset classes in a global risk parity framework, and diversified factor premia. Specifically, I will allocate 40% to global risk parity, 40% to a combination of market-neutral style premia including value, momentum, low-volatility and carry factors; and 20% to the global trend factor. I am choosing to emphasize the trend factor for two reasons. First, as mentioned above, trend is particularly attractive due to its history of delivering its best returns when other markets are in crisis. Second, because the trend factor is currently as “cheap” as it’s ever been in terms of its rolling 10-year annualized Sharpe ratio. Per Figure 4, the Sharpe ratio for the trend factor over the current decade ending September 2017 is lower than what has been observed over 98% of periods since 1903. I like to allocate to proven strategies that have fallen out of favor, and trend is a perfect example at the moment.

Figure 4. Percentile of diversified trend factor rolling 10-year Sharpe, 1900 – 2017

Source: Calculations by ReSolve Asset Management. Data from Hurst, Ooi, and Pedersen, “A Century of Evidence on Trend-Following Investing” (2017) for period 1903 – 2012, and Moskowitz, Ooi and Pedersen, “Time-Series Momentum” (2012) for period 2013 – 2017.

One challenge to my approach, which seeks to maximize diversification across many uncorrelated sources of return, is that the final portfolio will have very low volatility. Despite this low volatility, the expected returns from un-levered exposure to the diversified portfolio are considerably higher than what I expect from traditional stocks and bonds over the next decade or two. However, since my strategy is explicitly competing with an all-stock benchmark (the S&P 500), I will use leverage to target a volatility that is more consistent with the long-term volatility of stocks. This will help avoid one of the challenges that Seides faced with his portfolio. Specifically, I will borrow the same value as the portfolio to achieve a total of 200% exposure, and 12% volatility. To finance the leverage, I will assume borrowing costs at T-bills + 1%.

For illustrative purposes, Figure 5 through 9 describe the hypothetical constitution, historical risk contributions, and performance character of our proposed strategy. The global “risk parity” strategy is based on a diversified basket of global asset classes reconstituted monthly to achieve “equal risk contribution” assuming a 1% fee. Volatilities and correlations are calculated using the RiskMetrics (2006) methodology described here. The market-neutral “style premia” portfolio is proxied by a heavily discounted version of the strategy described in the paper “Investing with Style” (2012) by Ilmanen, Israel and Moskowitz, with data provided by the authors. The returns data also include a 1.5% fee. The diversified “Trend” strategy is proxied by the strategy in “A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen (data provided by the authors) and supplemented by data from “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen (data here), less a 1.5% annualized fee. We use data from 1990 through September 2017, with a one-year data-priming period, which gives us monthly data from 1991 – August 2017.

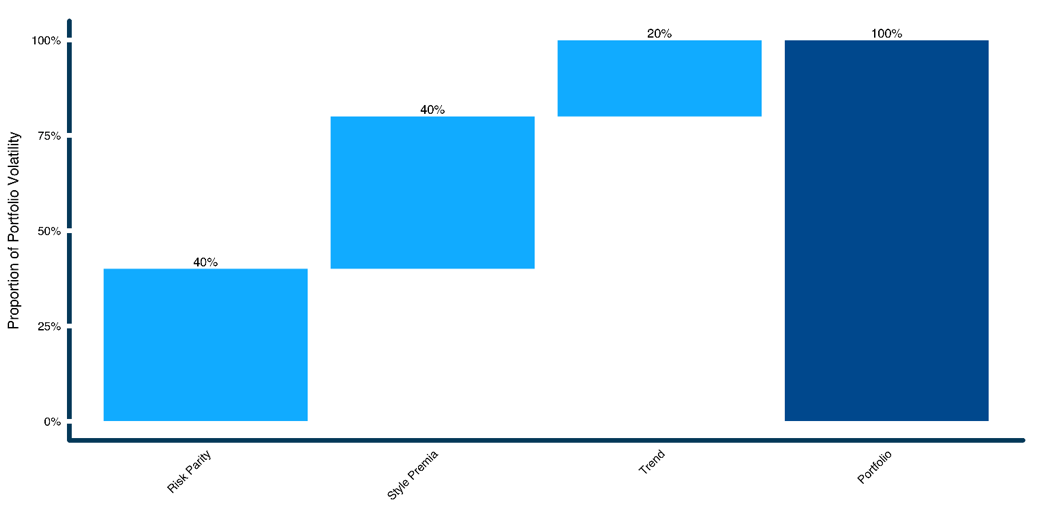

Figure 5. Proposed portfolio weights

Source: Calculations by ReSolve Asset Management. Data for Risk Parity from CSI and S&P Down Jones Indices. Data for Style Premia furnished by the authors, and based on the strategy described in ”Investing with Style” (2012) by Ilmanen, Israel and Moskowitz. Data for Trend furnished by the authors, and based on the strategy described in”A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen from 1990 – 2012, and “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen from 2013 – 2017. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal, investment or tax advice.

Source: Calculations by ReSolve Asset Management. Data for Risk Parity from CSI and S&P Down Jones Indices. Data for Style Premia furnished by the authors, and based on the strategy described in ”Investing with Style” (2012) by Ilmanen, Israel and Moskowitz. Data for Trend furnished by the authors, and based on the strategy described in”A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen from 1990 – 2012, and “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen from 2013 – 2017. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal, investment or tax advice.

Figure 6. Proposed proportional risk contributions

Source: Calculations by ReSolve Asset Management. Data for Risk Parity from CSI and S&P Down Jones Indices. Data for Style Premia furnished by the authors, and based on the strategy described in ”Investing with Style” (2012) by Ilmanen, Israel and Moskowitz. Data for Trend furnished by the authors, and based on the strategy described in”A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen from 1990 – 2012, and “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen from 2013 – 2017. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal, investment or tax advice.

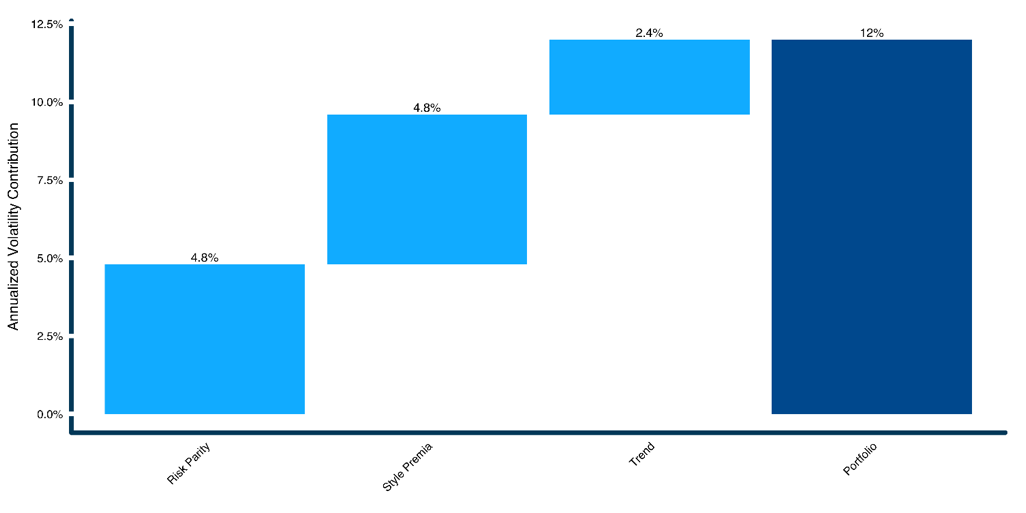

Figure 7. Proposed portfolio volatility contributions

Source: Calculations by ReSolve Asset Management. Data for Risk Parity from CSI and S&P Down Jones Indices. Data for Style Premia furnished by the authors, and based on the strategy described in ”Investing with Style” (2012) by Ilmanen, Israel and Moskowitz. Data for Trend furnished by the authors, and based on the strategy described in”A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen from 1990 – 2012, and “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen from 2013 – 2017. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal, investment or tax advice.

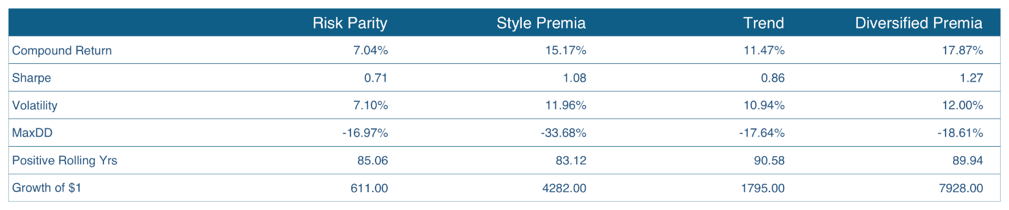

Figure 8. Constituent strategies and Diversified Premia performance 1991 – Aug 2017. SIMULATED PERFORMANCE

Source: Calculations by ReSolve Asset Management. SIMULATED PERFORMANCE. Global Diversified Premia is 40% Risk Parity, 40% Style Premia, 20% Trend. Data for Risk Parity from CSI and S&P Down Jones Indices. Data for Style Premia furnished by the authors, and based on the strategy described in ”Investing with Style” (2012) by Ilmanen, Israel and Moskowitz. Data for Trend furnished by the authors, and based on the strategy described in”A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen from 1990 – 2012, and “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen from 2013 – 2017. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal, investment or tax advice.

After borrowing costs and assumed fees, the simulated Diversified Premia portfolio produced almost 18% annualized returns since 1991, with a Sharpe ratio of 1.27. We are targeting a long-term Sharpe ratio of about 1.0, so we expect the portfolio to produce 12% excess returns at our target 12% volatility, which is about twice the long-term U.S. equity risk premium of about 6%. Of course, we could have levered the portfolio to a volatility target of 16%, consistent with the long-term volatility of global equities, but we don’t think we’ll need anywhere close to that amount of risk to dominate U.S. stock returns over the next decade or so.

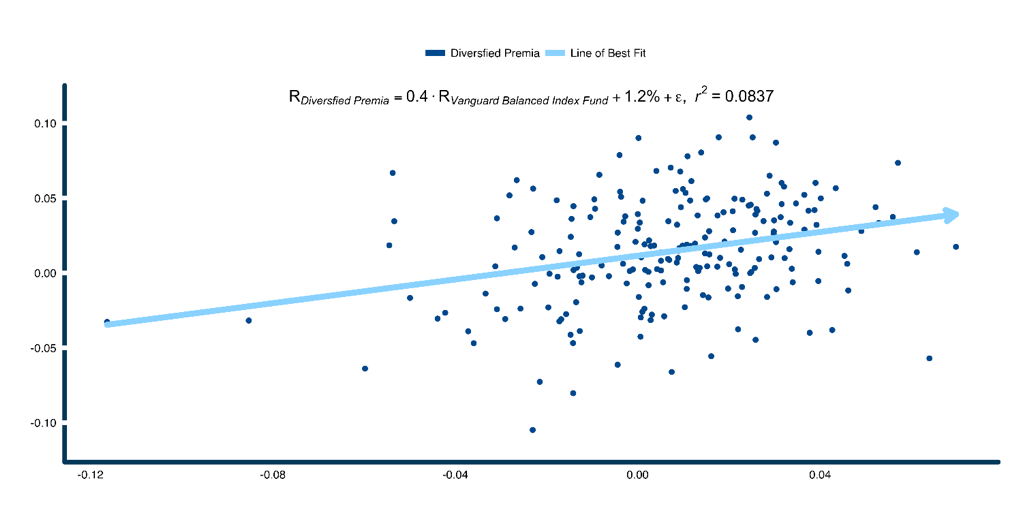

Importantly, we expect our Diversified Premia portfolio to produce returns with very little help from U.S. equities or bonds. A regression of the historical simulated Diversified Premia returns on the Vanguard Balanced Index fund (VBINX) yields an r-squared value of 0.084, suggesting that traditional U.S. stock and bond exposure explains just 8.4% of the returns to our Diversified Premia portfolio. In addition, over 25 years in simulation, and after discounting and fees, the strategy produced 1.2% per month in pure alpha, or about 14% per year. This alpha is a function of exposure to a wider variety of traditional and alternative risk premia.

Figure 9. Regression of proposed Diversified Premia returns on Vanguard Balanced Index Fund (VBINX), 1992 – Aug 2017

Source: Calculations by ReSolve Asset Management. VBINX data from CSI. Data for Risk Parity from CSI and S&P Down Jones Indices. Data for Style Premia furnished by the authors, and based on the strategy described in”Investing with Style” (2012) by Ilmanen, Israel and Moskowitz. Data for Trend furnished by the authors, and based on the strategy described in”A Century of Evidence on Trend-Following Investing” (2017) by Hurst, Ooi and Pedersen from 1990 – 2012, and “Time-Series Momentum” (2012) by Moskowitz, Ooi and Pedersen from 2013 – 2017. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, accounting, legal, tax, investment or tax advice.

Epilogue

At ReSolve, we believe risk is the probability that an investor will not meet his financial objectives. In the context of this definition of “risk,” and given current historically rich developed-market stock and bond valuations, we think traditional portfolios are extremely risky. Our objective is to propose a publicly available, alternative portfolio filled with a much wider variety of return sources, that we believe will help close the gap. In particular, we believe our proposed Diversified Premia strategies based on risk parity and factors is well positioned to deliver considerably higher returns than traditional portfolios over the next 10-20 years, with less risk.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All