Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Investment opportunities are quite limited, in part due to the legacy of quantitative easing (QE) engineered by central banks in response to the 2008 crisis. Those actions lowered costs of borrowing and boosted asset prices, especially for U.S. equities. The Fed will enter uncharted waters as it begins to reduce its balance sheet, in addition to raising short-term interest rates.

How should investors respond?

Investors should look at reducing risk in their portfolios. They can sell assets that have rallied and retain a portion of the proceeds in cash to protect capital, in case market prices deteriorate sharply, as occurred in 2000-2002 and again in 2008-2009. U.S. stock valuations are an excellent candidate. Based on a number of metrics, including the cyclically-adjusted price/earnings (CAPE or P/E10) ratio, U.S. stocks are at stratospheric levels that have only occurred twice since 1881. Non-U.S. stock markets look more attractive.

Investing in overvalued asset classes eventually impairs capital. Twice since 2000, U.S. equities have fallen by 40%, generating significant losses for investors. Seth Klarman at Baupost Group recently stated: “When securities prices are high, as they are today, the perception of risk is muted, but the risks to investors are quite elevated.” That sentence is well worth reading at least twice, if not three times! Similar to a house of mirrors, the optics often are at odds with the underlying reality, making investment choices even more elusive and challenging.

A decision to hold cash and forego potential returns is sensible when assets are overpriced, as they are today. In the words of Warren Buffett, we do not need to swing at every pitch. In 2005, in an annual letter to shareholders, Seth Klarman noted: “we prefer the risk of lost opportunity to lost capital.” We agree that the current focus should be on preserving capital. The generalized belief that there is no alternative to U.S. equities is at odds with this approach. If we face poor investment choices, given valuations, macro risks, etc. opportunities may well improve over time. Markets are cyclical, even those momentarily distorted by central bank policies.

U.S. equity valuations

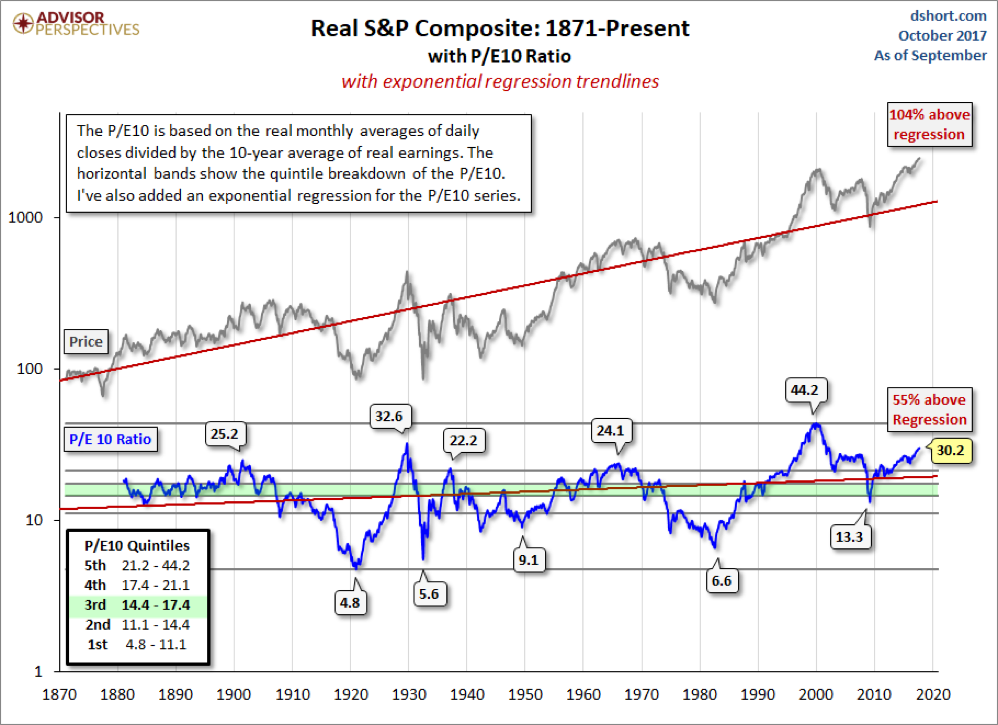

Using any number of metrics (including CAPE, market cap/GDP, Tobin’s Q, etc.), U.S. equities are expensive. Doug Short and Jill Mislinski have generated the chart below, which illustrates the history for U.S. equities going back to 1871.

According to Robert Shiller, at the end of September, P/E10 ratio for US equities was slightly above 31, a level seen only two times since 1881, first, just prior to the Great Depression in 1929 and then again before the tech bubble burst in December 1999. The P/E10 is not a particularly useful trading tool, with one very important exception. Namely, when it reaches extreme levels, either high or low, it provides very useful information to mitigate risk.

For example, in August 1982, the P/E10 declined to 6.6, suggesting that stocks had become cheap. And conversely, when the P/E10 approaches extreme highs, as in September 1929 (33), in December 1999 (42), and once again today (31), a decision to reduce exposure makes sense. Needless to say, we cannot predict whether the P/E10 will continue its surge in the short-term, perhaps hitting 35 or even 40. However, given current levels, U.S. stocks are vulnerable.

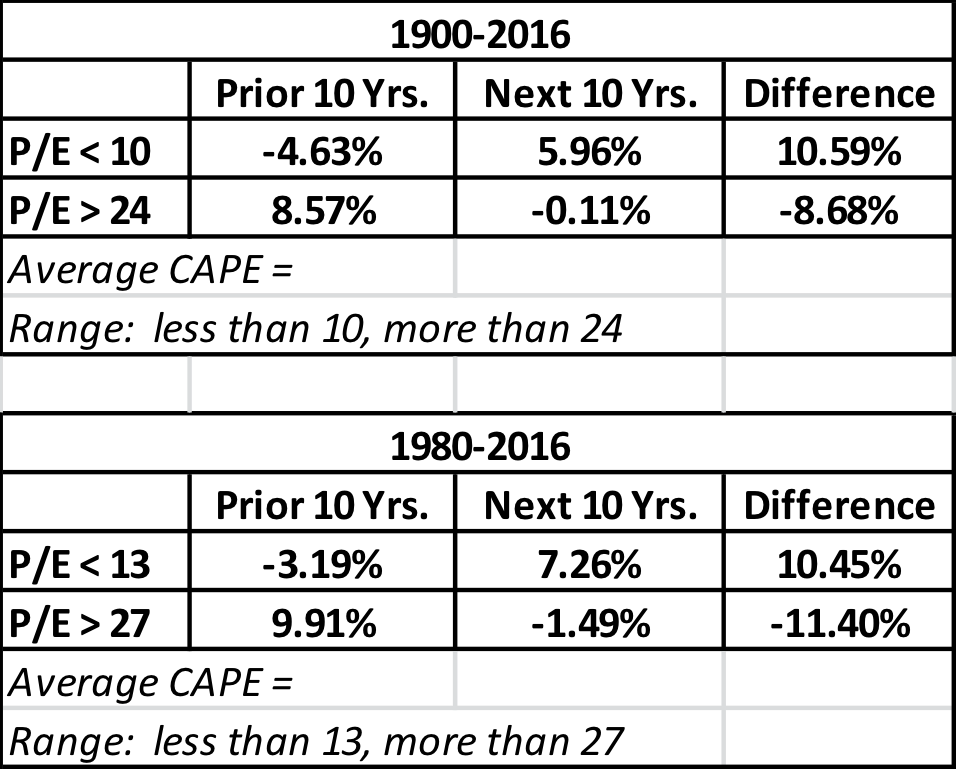

In the analysis that follows, returns refer to real returns (net of inflation). I conduct a very simple analysis in the table below. It illustrates average annualized returns for 10-year periods for those months when the P/E10 is at an extreme level. I define extreme levels relative to the averages in the 1900 to 2017 and the 1980 to 2017 periods. As a sports announcer in Washington DC used to say, “Let’s go to the videotape.”

The data above indicates that extreme P/E10 ratios provide useful information for both periods. From 1900 to 2017, when the P/E 10 ratio was extremely low, returns during the preceding ten years were negative (-4.6%) and returns for the following ten years are positive (+6.0%). These periods, when U.S. equities were cheap, represented very good times to invest.

Conversely, when the P/E10 ratio was extremely high (more than 24), then the returns for the preceding years were highly positive (9.9%) and returns for the following 10 years were modestly negative (-0.1%). Thus, when P/E10 ratios are at extremely high levels, we should consider reducing exposure to US equities.

Similar patterns occur during the shorter 1980 to 2017 period. When P/E10 ratios were below 13, the previous 10 year returns on average were negative (-3.2%) while those for the following 10 years were quite positive (+7.3%). And conversely, when P/E10 ratios were above 27, the previous 10-year returns on average were positive (9.9%) and the returns over the following 10 years were negative (-1.5%).

Let’s take a closer look at a couple of dates when this ratio was at extreme levels.

-

September 1929: The P/E10 ratio rose to 32.6. During the preceding 10 years (from October 1919 to September 1929), annualized returns were a whopping +13.6%, as the P/E10 ratio increased from 6.8 to 32.6. Needless to say, a decision to invest in September 1929, as Irving Fisher declared that a “permanent plateau” had been reached for equity prices, would have generated enormous losses. The annualized returns over the next ten years were -6.7%.

-

August 1982: The P/E10 ratio declined to 6.8. During the previous 10 years (from August 1972 to July 1982), annualized returns were -8.2%, as the ratio fell from 17.6 to 6.8. With the P/E10 ratio near record lows, investing generated annualized returns of +10.2% over the following decade.

-

December 1999: The P/E10 ratio rose to 44.2, the highest level on record since 1881. Annualized returns over the preceding decade (January 1990 to December 1999) were quite strong, at +11.9%, as the P/E10 ratio increased from 18.4 to 44.2. A decision to invest in December 1999 would have generated annualized returns of -4.9%.

-

September 2017: The P/E 10 ratio is now at 31.2, a level seen only twice since 1881. Real returns over the past decade have been relatively modest at 3.42%, given the fact that they include the crisis in 2008. Since March 2009, the S&P has generated annualized returns of about +12.0%.

The P/E10 ratio provides useful information when it is at extreme levels. When it is extremely high, as it is today, it provides useful early-warning information, and when it is at extremely low levels, it indicates a very good time to invest.

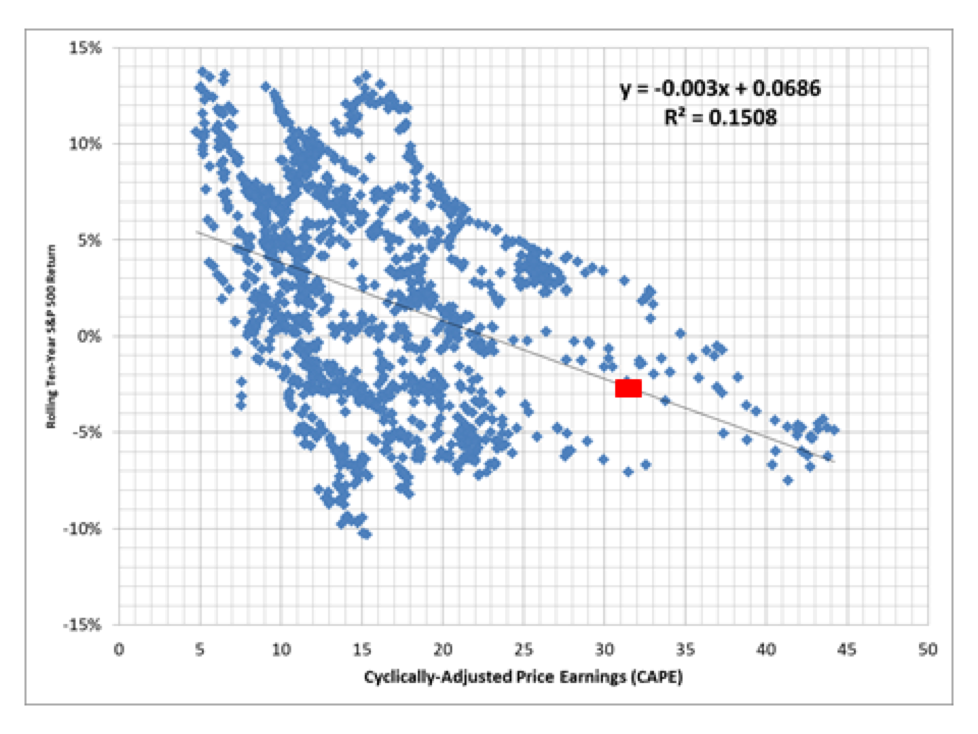

The P/E10 ratio is extremely high, relative to both periods, which suggests that the S&P 500 is likely to deliver very modest (potentially negative) returns over the next decade. Below, I regress 10-year returns on the P/E 10 ratio from 1980 to 2017. This forecasts a negative annualized return (-2.5%) over the next 10 years.

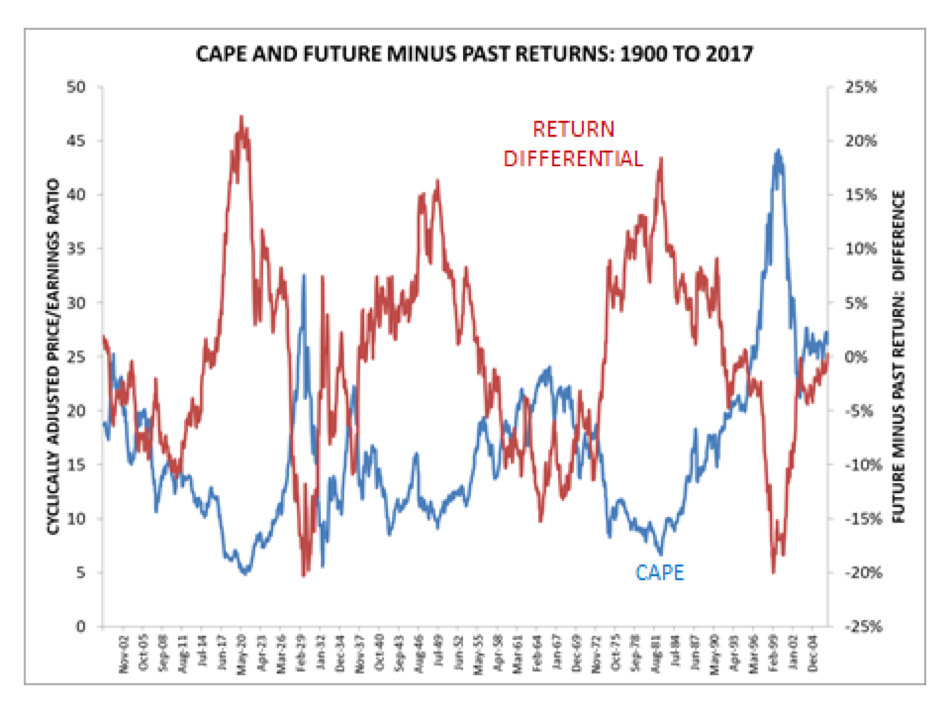

The chart below illustrates this from another perspective. I examined the P/E 10 ratio over time (blue line) and compared it with the difference in returns from the decade prior to the decade after each month. For example, in August 1982, the previous 10 years generated annualized returns of -8.2%. The next 10 years generated returns of +10.2%, so the difference for that month is a positive 18.4%. The correlation between these two data series (P/E10 ratio and return differentials) is 0.73 for the 1900 to 2017 period, and 0.96 for the 1980 to 2017 period.

This data confirms that the P/E10 ratio provides useful information when valuations are extremely high or low. Based on this analysis, given that the ratio is at extremely high levels, it makes sense to reduce exposure to U.S. equities. Others have reached similar conclusions, including John Hussman and James Montier at GMO. Some recognize that U.S. equities are expensive, but think they can exit the markets on a timely basis. Hussman believes that U.S. equities could lose as much as 60% of their value on an interim basis, while he believes they will generate a return of zero between now and 1929.

I am not arguing that a collapse in US equity prices is imminent – perhaps it is, perhaps it is not. The path is always uncertain. However, U.S. equities have declined by 40% twice since 2000. There are metrics that can provide advanced warning, though none of these are entirely foolproof. Even John Bogle, who believes in being “fully invested,” has stated that he thinks one or two declines of 50% are entirely possible over the next decade. The case for weak returns becomes even more robust once we examine the macroeconomic drivers of current valuations.

Other factors

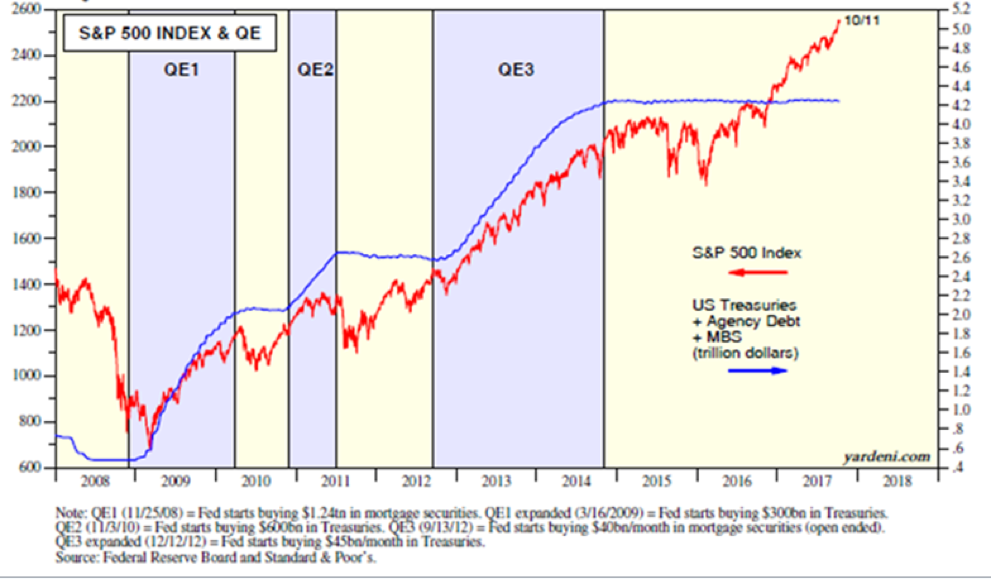

QE policies engineered by the Fed beginning in late 2008 (see chart from Ed Yardeni below) helped fuel the surge in U.S. equity prices, as the P/E 10 ratio rose from about 10 to 25 when the Fed ended these purchases in October 2014. By then, the Fed’s balance sheet stood at about $4.5 trillion, having increased from just over $700 billion at the beginning of this program.

These policies succeeded in boosting asset prices and effectively lowered the costs of borrowing. Unfortunately, they did not do much to stimulate real economic growth. In fact, these policies largely benefited those households that own financial assets, mostly the top 20% of the wealth distribution, which as of 1983 owned more than 80% of all wealth. By 2013, the top 20% owned nearly 90%. The additional “wealth” these policies generated did little to support aggregate demand, given that studies have proven that these households do not tend to shift consumption habits by much in response to increases or declines in wealth. However, these policies did nothing to mitigate the burgeoning debt stock in the bottom 80% of households, other than perhaps lowering the costs of servicing that debt. These households ability to consume has been negatively impacted. The net effect has been a weak economic recovery, given the inability of the bottom 80% to fulfill their historic role of consuming most of what they earn, given a continued need to service this debt (plus rising student loan debt, auto debt, etc.).

The rate of real economic growth will not suddenly accelerate until the excessive debt stock of the bottom 80% has been excised. And, as a consequence of QE, asset prices, primarily US equities, are overpriced, consistent with what we saw earlier with P/E10, driving the following concerns:

- Appreciation of U.S. equity prices have been driven by financialization, increased liquidity and QE, not by improvement in fundamentals or economic growth.

- Real economic growth remains weak, given the still significant debt stock held by the bottom 80% of households, who historically have fueled aggregate demand. They are incapacitated from doing so today, and given the expectation that interest rates may be more likely to rise than to fall, there is little reason to expect this to change.

- The “recovery” is increasingly prolonged – and a recession at some point will become inevitable. If the debt stock remains at that point in time, we will, no doubt see QE4.

For these reasons, I am exceedingly cautious about U.S. equity market exposure, and recently have begun reducing exposure, while taking profits. Risk is asymmetrically biased to the downside. Prices will decline; I do not know when. Does it make sense to risk a potential loss of 30% to generate an additional 10% in return? Are we really that good at playing “chicken” with the financial markets? Investing should not be treated as a game that can be won – we can only lose, in terms of failing to meet our long-term investment objectives.

Conclusion

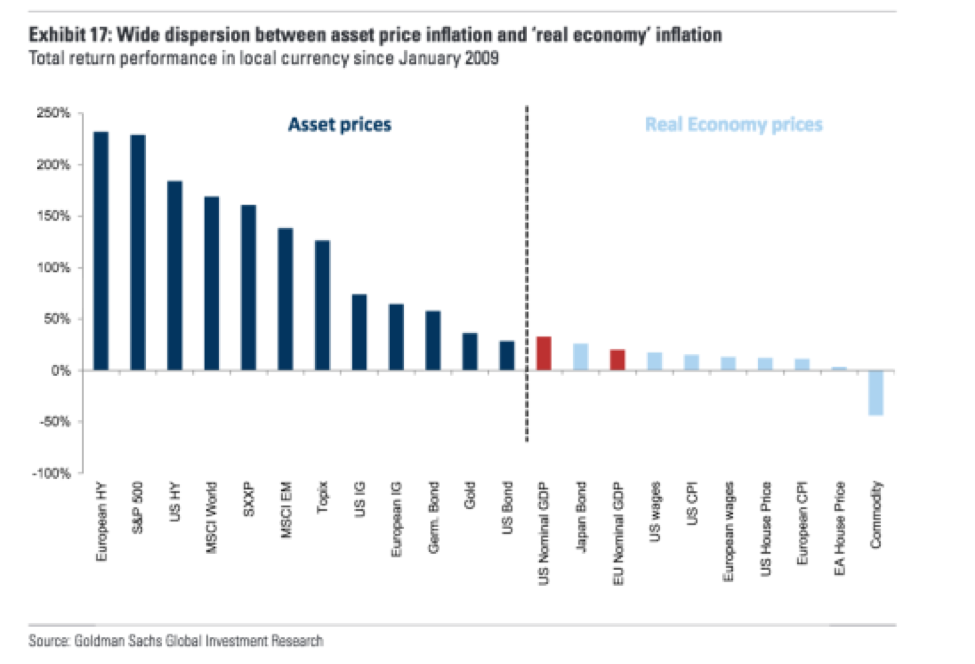

In addition to building a cash reserve, in light of valuations across asset classes (see chart from Goldman Sachs below, which compares asset prices with the real economy), my firm also is investing in non-U.S. equities for several reasons. First, the financial cycles in many of these economies have lagged that of the U.S. And second, QE policies have continued across these economies. The funds derived from our reduced allocation to U.S. equities has been divided equally between cash and non-U.S. stocks. Other asset classes, including high-yield bonds, emerging-market debt, corporate bonds and commodities do not appear attractively priced. Given current valuations across-the-board, we prefer to be patient and wait for a more attractive entry point.

John Balder is a co-founder and CIO at Investment Cycle Engine, Inc. His experience combines more than 25 years of work building innovative investment strategies at firms that included GMO and SSgA. He previously worked with the U.S. Treasury and Federal Reserve Bank of New York after beginning his career with the House Banking Committee on Capitol Hill. His research focuses on the financial stability and the real world relationship between macroeconomics and finance. More information is available at www.icycleengine.com.

Read more articles by John M. Balder