“…. valuing the market has nothing to do with where it’s going to go next week or next month or next year, a line of thought we never get into. The fact is that markets behave in ways, sometimes for a very long stretch, that are not linked to value. Sooner or later, though, value counts.” - Warren Buffett

As the equity bull market has entered its ninth year, market participants have voiced concerns over elevated valuation levels. John Hussman has been one of the more prominent who have sounded the warning bells about low expected returns and elevated risks embedded in equity valuations. In his recent note, Hussman stated that few investors recognize that one of the reasons why valuation multiples were so rich in 2000 is that profit margins were actually below historical norms at the time. The benefit of normalizing the embedded profit margin comes not just from muting margins that are above historical norms, but also from normalizing margins in periods where they are below historical norms.

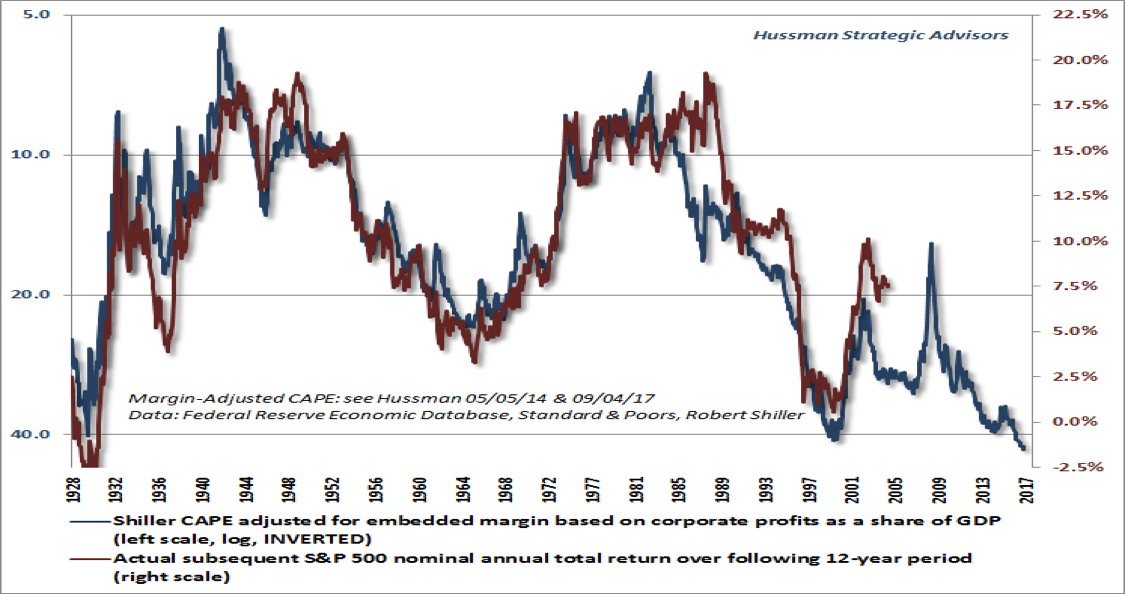

In the chart below, Hussman plotted the margin-adjusted cyclically adjusted price to earnings ratio (CAPE) on an inverted log scale along with actual subsequent S&P 500 nominal average total returns over the subsequent 12-year period. There are two points that are worth noting about this chart. Firstly, the fit between observed valuation levels and subsequent long-term returns is tight, suggesting that the valuation model employed is robust. Secondly, valuations based on this metric are in the same territory as the 1929 high and the tech bubble, zones that resulted in poor subsequent investment returns.

Source: Weekly Market Comment, John P. Hussman, Hussman Funds, October 2, 2017

At our firm, we are focused on a much smaller sub-set of businesses; that of high-quality businesses with durable competitive advantages. Accordingly, our concerns around market valuations are largely related to the valuation of this sub-set of businesses. Our target sub-set performed well over the last few years with a significant portion of that performance driven by the broader equity bull market. The important question that we face at this juncture is whether the sub-set of high-quality businesses is as overvalued as the broader markets and whether that is likely to bode ill for our future investment returns.

To effectively answer that question, we built a bottom-up model of the companies in our investment universe; the Global Moats Index. Our analysis covers 120 unique companies over the last 16 years with 110 of these companies being a part of our investment universe currently. In the discussion below, we take a deep dive into the profitability of these businesses as a group, levels of leverage employed, business reinvestments and share buybacks, and business valuations.

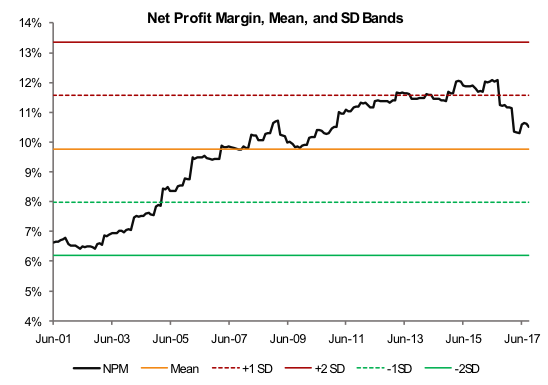

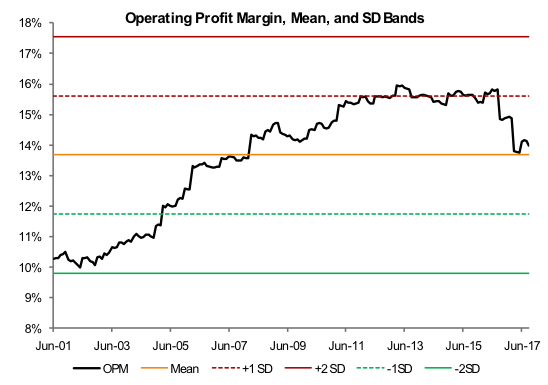

Profitability – troughs and peaks

As is seen in the charts below, profit margins, net profit margin as well as operating profit margin, started from a low level in 2001 and peaked in the 2013 to 2016 period. Since then, profit margins for the Global Moats Index have pulled back towards the mean of the past 16 years.

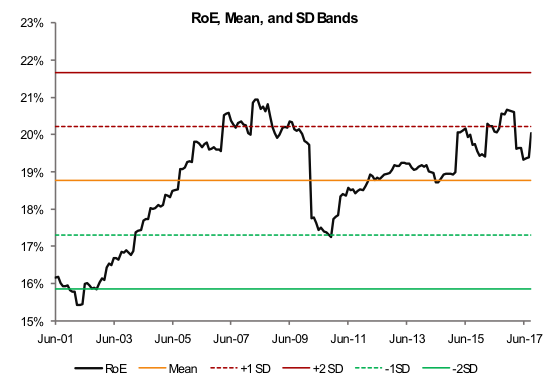

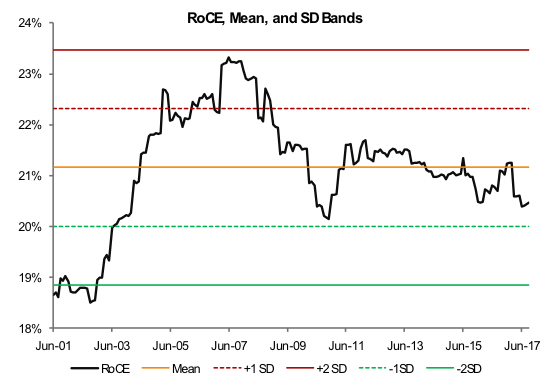

When we measure profitability in terms of returns on capital, a somewhat different picture emerges. For one, the range of returns on capital has been fairly tight when measured in terms of return on equity1 as well as return on capital employed2. Additionally, while returns on capital persistently increased between 2001 and 2007, since then we have had much more of an oscillating behavior.

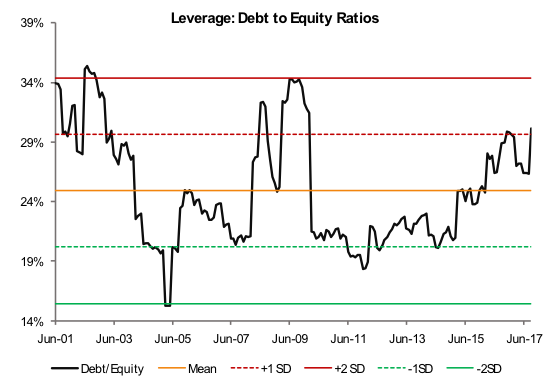

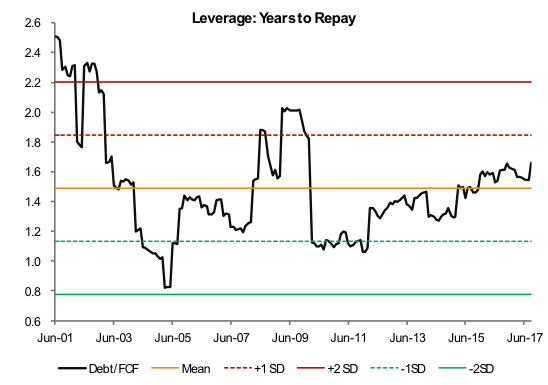

Leverage – capital structure and years to repay

The last few years have seen a significant increase in employment of leverage at corporate levels driven by low borrowing costs and lax lending standards, factors that have created an environment ripe for levered speculation. We have no affinity to levered engagements and accordingly we avoid leverage. As the charts below show, leverage embedded in our businesses remains well controlled. Years to repay debt as measured by total leverage divided by free cash flows has stayed below two years.

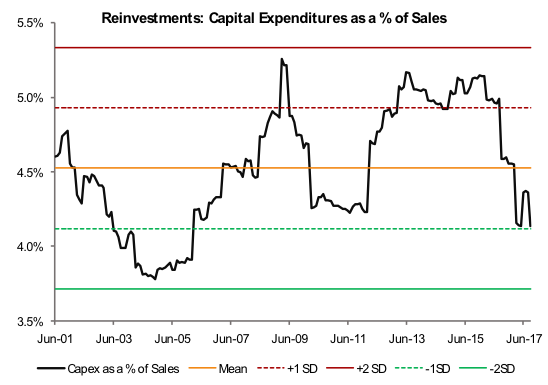

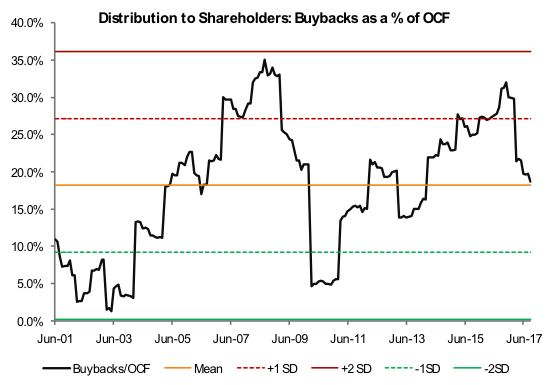

Usage of cash – reinvestments and distribution to shareholders

While the economic recovery since the global financial crisis has continued at a slow pace, reinvestments by companies have declined. Additionally, companies have increasingly engaged in buying back their own shares by borrowing at low interest rates. Interestingly, this behavior hasn’t been as pronounced among our high-quality businesses. Indeed, reinvestment rates as measured by capital expenditures as a percentage of sales has stayed around its mean. While buybacks did take up a larger share of the operating cash flows, they have since declined towards the mean.

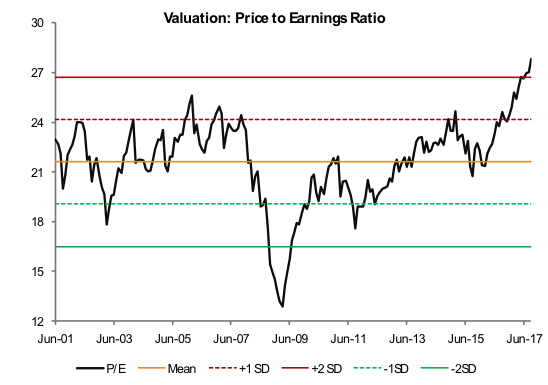

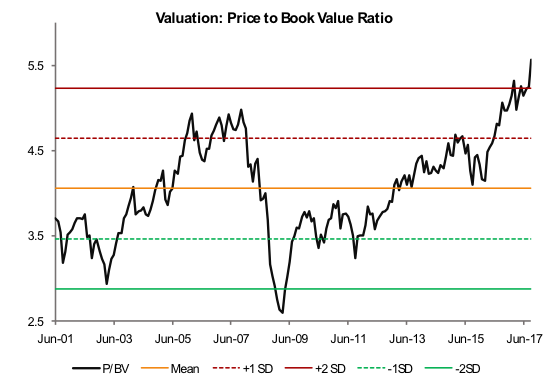

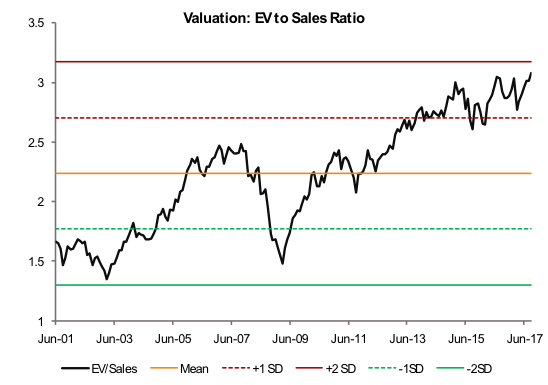

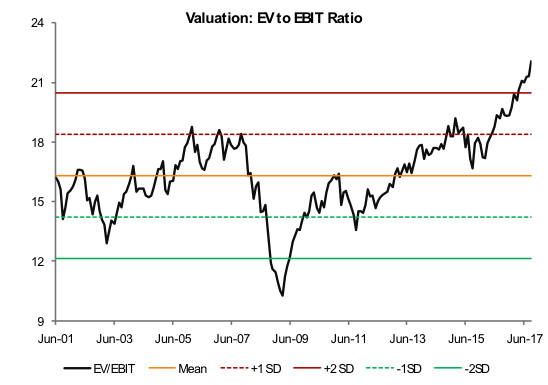

Valuation – uncharted territory as measured by conventional valuation tools

Much as the work of Hussman suggests for the broader equity markets, a similar picture emerges regarding valuations for the Global Moats Index. Valuations are in a zone where we haven’t been before.

Below, we show valuations for the Global Moats Index based on four conventional valuation tools, namely the price to earnings ratio, the price to book ratio, the enterprise value to sales ratio, and the enterprise value to earnings before interest and taxes (EBIT) ratio. In each one of the cases, valuations are the highest they have been over the last sixteen years.

Valuation – absolute valuations are suggesting overvaluation too

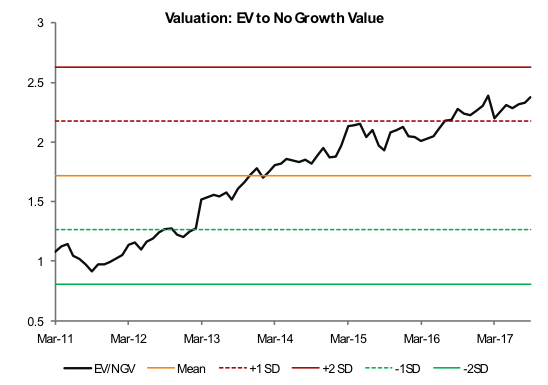

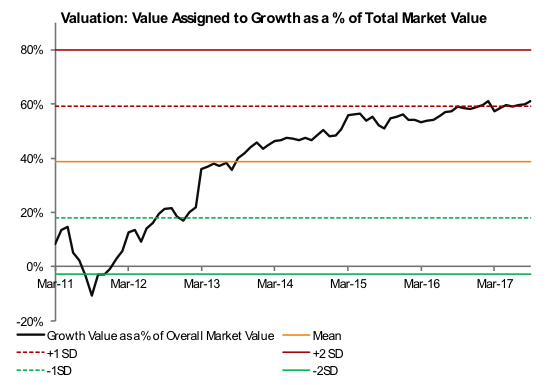

As Benjamin Graham posited, shares are not mere pieces of papers. Instead, they should be thought of as part ownerships in a business. As part owners of businesses that we invest in, we look to understand the value of what we own. One of the valuation metrics that we find quite useful is the value of the current business franchise of the business, i.e., the current earnings power value of the business’s moat. This is the value of a moat business if it were to have zero growth. Assessing the value of current earnings power of the business allows us to segregate the overall market value between the current earning power’s value and the percentage of market value that is ascribable to future growth of the business.

As is seen in the charts above, the Global Moats Index went from selling at just about the franchise value in 2011 to selling at more than 2x the franchise value currently. The result of this valuation rerating is that market participants went from assigning almost no value to the growth of our businesses in 2011 to assigning nearly 60% of the current market value to future growth.

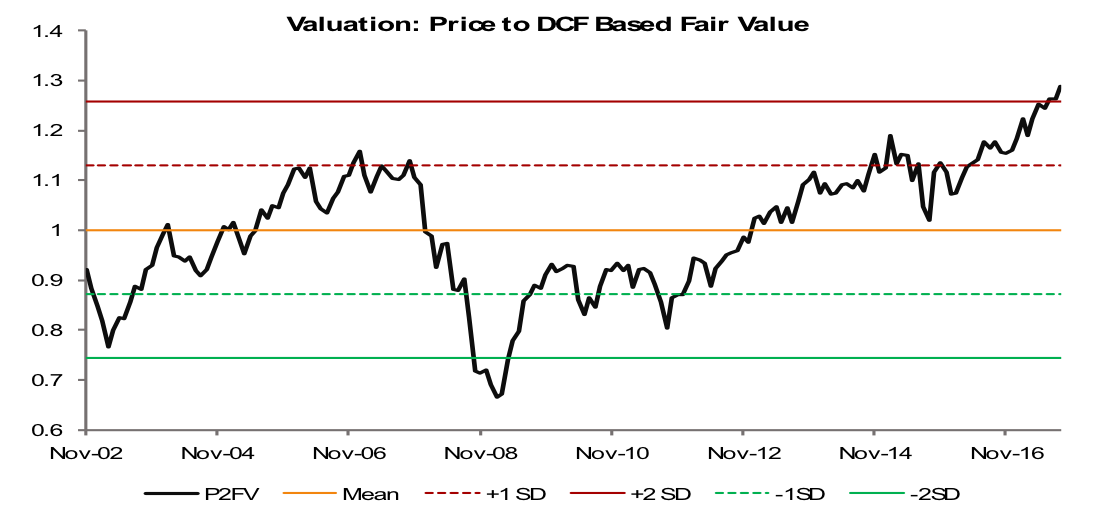

A similar picture emerges when one looks at the pricing of the index in relation to appropriately calculated discounted cash flow based business value. As is seen, we are indeed in uncharted territory.

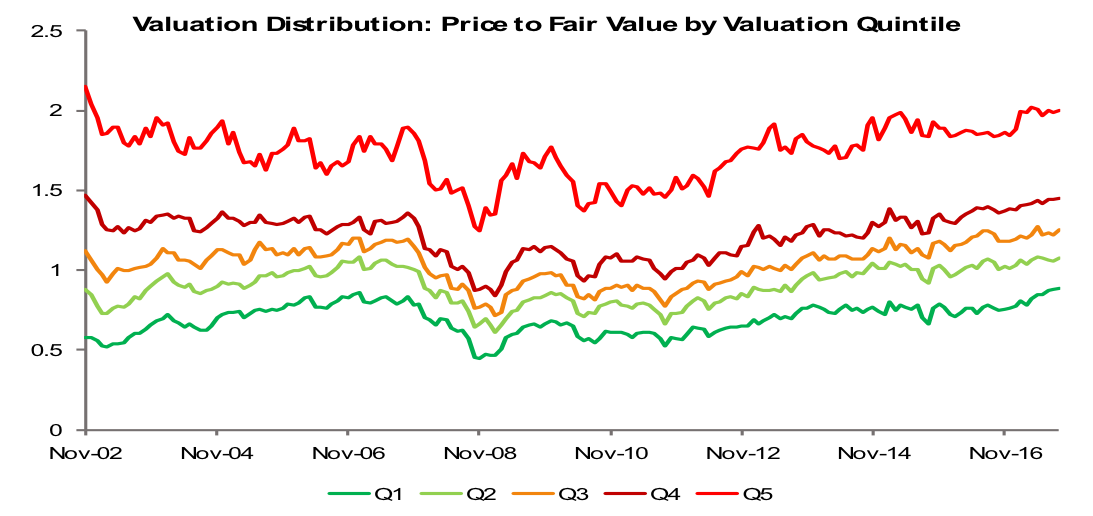

Valuation distribution – ability to buy businesses at meaningful discounts to fair value

As active investors, our ability to add value depends not only on the level of valuation across the target investment universe, but also on width of the valuation distribution. As is seen in the chart below, the valuation distribution continues to be wide affording us an opportunity to selectively build portfolios that have superior expected prospective returns. However, it is important to note that even the cheapest quintile is close to valuation levels that were observed in 2007.

Expected returns

Over extended periods, we expect our investment experience to be largely driven by the change in underlying per-share business values of the businesses in our portfolio. Accordingly, the key factor in our assessment of expected returns is the expected business value growth.

Over the past 16 years, businesses within the Global Moats Index observed a growth of about 13% in their intrinsic value with about 2% of the business value growth driven by margin expansion, i.e., core business value grew at about 11%. The Index’s results were further aided by valuation multiple expansion which added another 2.5% to the index’s returns.

Both these factors, margins and valuation multiples, are likely to be sources of negative returns over the next seven years. Assuming that profit margins and valuation multiples normalize over a course of seven years, they will contribute -1% and -4% respectively to the index’s returns. Further assuming that core business growth rate stays at similar levels as observed over the past 16 years and a contribution of 1.5% from dividends, we will expect our high-quality business universe to generate annualized investment returns of about 7.5% over the next seven years (11% -1% -4% +1.5%).

Clearly, our expected investment returns from hereon are well below the returns that we expect to generate over full business cycles. However, when looked at in relation to other investment avenues, our sub-set of businesses will likely serve as one of the best potential investment avenues over what promises to be a low-return period for equities.

There are two factors that support our opinion. Firstly, as we have shown above, we estimate prospective returns for the Global Moats Index to be 7.5% nominal. This estimated return is significantly better than the negative nominal return expectation for the broader equity markets as estimated by Hussman. Secondly, as the valuation distribution chart above shows, the valuation distribution within our investment universe continues to be wide. This affords us an opportunity to selectively build a portfolio of businesses that will likely generate investment returns that are superior to that of the Global Moats Index.

Summary

The Global Moats Index is depicting similar overvalued conditions as observed around the broader equity markets. Such elevated valuation levels have historically resulted in poor long-term investment returns. This time is not likely to be any different and prospective returns will be significantly lower than the returns over the last few years.

However, the superior quality of businesses in our investment universe results in business value growth that is significantly greater than publicly traded benchmarks. While valuation factor will likely affect our investment returns negatively, higher business value growth generated by our businesses means that our forecast of expected investment returns is significantly higher than that of the broader markets. Additionally, the width of valuation distribution within our investment universe affords us the opportunity to selectively build a portfolio of businesses that will generate excess investment returns over and above that of the Global Moats Index.

Baijnath Ramraika, CFA, is a cofounder and the CEO & CIO of Multi-Act Equiglobe (MAEG) Limited and is Executive Director at Sapphire Capital. As a portfolio manager, he manages the Global Moats Fund and the India Moats Fund. Contact him at [email protected]. Baijnath’s thoughts and ideas can be read at his blog at www.symantaka.com

Prashant K. Trivedi, CFA, is a cofounder of MAEG and the founding chairman of Multi-Act Trade and Investments Pvt. Ltd.

MAEG is an investment manager and manages the Global Moats Fund, an investment fund that invests in a global portfolio of high quality businesses with sustainable competitive advantages. Multi-Act is a financial services provider operating an investment advisory business and an independent equity research services business based in Mumbai, India.

1 Return on equity is calculated as net income divided by common shareholder’s equity.

2 Return on capital employed is calculated as operating profits divided by shareholder’s equity plus debt.

Read more articles by Baijnath Ramraika, CFA and Prashant K. Trivedi, CFA