Richard Bookstaber has authored two superbly written and thoughtfully argued books on the flaws of the financial system. His first, A Demon of Our Own Design (2007), was focused on the system’s complexity and foresaw the global financial crisis of 2007-2009. His latest book, The End of Theory, argues that economics as currently understood is poorly designed to understand the financial system and its potential for crises, and calls for agent-based modeling (ABM) as an alternative to the techniques used by most economists.

We spoke on July 20, 2017.

Bookstaber is chief risk officer of the University of California’s pension and endowment fund, one of the world’s largest. Previously, he was at Moore Capital, Bridgewater, and several other institutions, as well as the U.S. government’s Office of Financial Research. His Ph.D. in economics is from MIT.

What’s the matter with economics?

Siegel: You say that “economics works, until it doesn’t… Economics…not only leaves the cascades and propagation over the course of a crisis unexplained but also asserts that they are unexplainable.” In this context, what do you mean by economics? Microeconomic price theory? Macro? Financial economics? Are all of them flawed?

Bookstaber: Mostly I am talking about macroeconomics as it is currently taught in graduate schools, so that is what the economists at the Fed and at large financial institutions know best.

Siegel: What are the essentials of this macro theory?

Bookstaber: This theory or approach to the world is applied in central banks through what are called, in the trade, dynamic stochastic general equilibrium (DSGE) models. At least that is how it is applied by central bank economists. How much it is used by the policy makers is another question. I hope the answer is, “not much.”

The theory asserts that everyone in the economy is proxied by a single representative agent, a hypothetical individual who lives in a stable, equilibrium world, and makes fully informed, rational decisions.

Siegel: Why, in your view, is this theory, or set of theories, inadequate for understanding the economy, with its periodic disruptions, financial crises, and so forth?

Bookstaber: First, I’m not saying economics fails broadly. I’m focusing specifically on financial crises, and on the financial part of financial crises – what happens in financial institutions, not what happens when the crisis breaks through to affect the real economy.

What happens is that some shock spreads to affect critical components of the system, including those that had no apparent connection to the initial shock. Think, for example, of the propagation that started with the subprime mortgage market, really a backwater market, in 2008. This is analogous to minor traffic incident causing a huge traffic jam that affects people who are far from the incident, or, tragically, to the 2,400 Hajj pilgrims in Saudi Arabia who died a few years back in a stampede that occurred seemingly out of nowhere. Such stampedes have occurred in many times and places.

These are called emergent phenomena. From a distance, it looks like the cars on the highway, or the crowds in the street, have begun to behave like a single organism. This occurs because each agent’s behavior affects the environment in which every other agent operates. In neoclassical economics with a single representative agent, such behavioral contagion can’t occur, but in real life it does. If a model is going to be useful for understanding financial crises, it needs to take into account emergent phenomena.

Fire in a nightclub

Siegel: You have compared a financial panic to a fire in a nightclub. What are the parallels?

Bookstaber: In The End of Theory, I say that a financial risk manager is like a fire marshal. The problem, in a nightclub fire, is that people can’t get out fast enough because the exits aren’t big enough; they don’t have the time to get out because the fire is spreading too quickly; and there are too many of them.

So the relevant variables if you want to deal with the risk of fire are: how fast people can get out given the size of the exits, how many people have to get out, and how much time do they have to get out given the flammability of the building.

That’s what goes on in a financial crisis, too. Those who are really leveraged have to get out. How fast they can get out depends on the size of the exits, which is the amount of liquidity in the system. How many have to get out also depends on the concentration in that market, the crowding. The problem is, you can’t just calculate that as you would in a simple physics problem, because the very fact that people are trying to get out to the exits effectively changes the size of those exits. That is where emergence comes in.

Siegel: That’s a good way to think about it. As you’ve written, we don’t just react to our environment – our behavior changes the environment.

Bookstaber: That’s right. And a “fire” in the financial system is worse than in the nightclub. The effort of people to get out of the nightclub doesn’t actually increase the flammability of the building. But, in a financial crisis, the greater the number of people who are trying to get out of a financial market, the greater the “flammability” of the “building,” because leverage causes other people to become embroiled who would not otherwise have been involved. So the emergent phenomenon ends up proceeding in two directions, and you can’t model it well without something like an agent-based model.

Siegel: What is an agent-based model?

Bookstaber: It is one that models the behavior of each agent in the economy separately instead of mushing them all together into a representative agent. Before I get into explaining agent-based models, let me get into why we need a new model in the first place. There are four conditions that distinguish the real-world financial system from the economic models that most analysts use to try to understand it. And those conditions leave standard economics wanting. The existence of emergent phenomena is one of those four conditions. The other three are non-ergodicity, computational irreducibility, and radical uncertainty. I call these, along with emergent phenomena, the Four Horsemen of the Econocalypse.

Non-ergodicity: Things change over time

Siegel: These sound quite formidable. Let’s go into these one at a time. What is non-ergodicity?

Bookstaber: Economics assumes we are in an ergodic world, one in which the probability distribution of outcomes is the same at all times and places.

In an ergodic world, if you move through it for a long enough time, just about everything that could be experienced would be experienced. If I moved forward 10,000 years, the world would not look very different. But we are human, we change with experience, we invent, we interact, we alter what we do based on what’s happened in the past; all these things create a world that is not ergodic.

Siegel: How does this observation help us understand the financial system?

Bookstaber: If you want to use history as a guide for what’s going to happen in the future, you are going to have a problem. If you have a model that doesn’t lead to surprising changes in the characteristics of the world, it’s not reflecting how the world really works.

This is more than saying the world is random. You can have a random component and still have the world be ergodic because the random events are drawn from the same distribution every time.

Siegel: And why do you think the financial system is not ergodic?

One of the reasons the financial world isn’t ergodic is that we develop new strategies, new instruments, new financial entities. We react differently based on our past experience. The next crisis we have is not going to look like 2008 because we will have adjusted our behavior based on 2008.

Computational irreducibility

Siegel: So let’s get to the next of the four horsemen. What is computational irreducibility?

Bookstaber: Computational irreducibility means that you have a process or a dynamic that you can’t pin down to a set of equations, and that you can’t solve analytically. If you want to know where things are going to be, you have to march down the path as it moves along, either in reality or through simulation.

A good example of that, from physics, is the three-body problem. The three-body problem is computationally irreducible. If there are three planets in a gravitational system and I want to know where the three of them are going to be located five years from now, I can’t find out by solving an equation {except in a few special cases). In general, there is no equation that I can plug numbers into and figure out where the planets will be. I have to actually follow the path, minute by minute, of each of those planets to see where they’ll end up.

Siegel: Why is the financial system computationally irreducible?

Bookstaber: Well, if we find computational irreducibility for a problem as simple as this – it is deterministic, and involves only three “agents” all interacting based on simple rules of physics – what are the odds something so complex and interacting as the financial system is not going to have the same characteristic? The point is that you find computational irreducibility just about everywhere.

Radical uncertainty

Siegel: Finally, you’ve written that the financial system is characterized by radical uncertainty. We all know what uncertainty is, but what is radical about the uncertainty facing financial agents?

Bookstaber: You’ve heard the comment by Donald Rumsfeld about known unknowns and unknown unknowns, which refers back to work by the economist Frank H. Knight.

When you face known unknowns, you know what phenomenon you are trying to measure or forecast, but you don’t know the value of the variable, the measurement itself. With unknown unknowns, you don’t even know what phenomenon you’re trying to measure. You don’t know what it is that you don’t know. That is radical uncertainty.

Siegel: What do you mean by radical uncertainty?

Bookstaber: To answer your question – and actually shed some more light on my comments about computational irreducibility – I’m going to talk about agent-based models, in particular Conway’s Game of Life [called “Life” for short], a computer simulation that shows how agents behave in an interactive system.

Agent-based models and the “Game of Life”

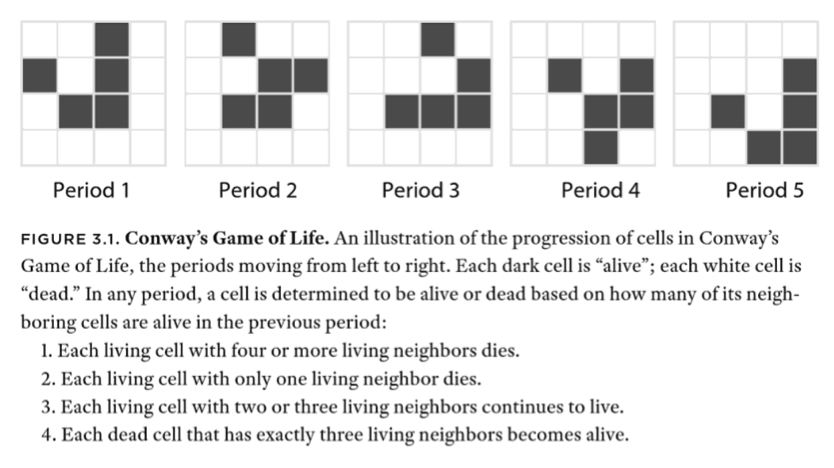

Siegel: Can you describe Conway’s Game of Life?

Bookstaber: Life is a computer game that uses cellular automata – essentially a set of agents with prescribed behavior – to simulate the behavior of extremely simple living organisms.[1]

Exhibit 1, from my book, summarizes the rules and gives some intuition of how a cellular automaton can be programmed to behave and how the game proceeds.

Exhibit 1

Conway’s Game of Life

Source: Bookstaber [2017], page 31.[2]

The little group of five black cells that behaves like a very primitive organism is a single cellular automaton. Life is a “zero-player game” in that all outcomes at every stage are determined by the initial settings. You “play” the game by manipulating the initial settings to try to get the result you want.

Siegel: What light does the Game of Life shed on agent-based models and financial markets?

Bookstaber: Well, first of all, note that it is an agent-based model. Each black square is an agent, the four rules define its heuristic, and the cells surrounding it define its environment.

It is pretty much as simple an agent-based model as you can get. But although it is simple, it turns out that the game is incredibly rich, and it has the characteristics that I talked about earlier.

It is computationally irreducible. So if you start a grid like the one in Exhibit 1, and you make a bunch of cells come alive, and you ask me what cells will be alive if I let the game run for, say, 1,000 periods, there is no equation I can use to tell you. I have to run it through those 1,000 periods.

Also, it has emergent phenomena. All these lives are moving along, and suddenly they might just go splat all over the place, half of them coalesce, and so on.

Finally, it is non-ergodic and it embodies radical uncertainty. These are the Four Horsemen of the Econocalypse that I referred to earlier, the four characteristics that define financial markets in the real world where agents are real people.

Siegel: In what sense does Life involve radical uncertainty? The game sounds like it is deterministic. And it can only take on so many states. And those states are well defined.

Bookstaber: That’s true. But here’s the thing. If you run the game on, say, a million by a million grid – and you can do that on a computer – the number of possible outcomes, or states of nature as they are called in decision theory, is greater than the number of atoms in the universe by many orders of magnitude. So, in what sense do you understand all the states of nature, all the possible outcomes of the game? Well, you don’t. You have radical uncertainty, because you can’t comprehend everything that’s possible.

Siegel: And this ties into the celebrated Argentine writer Jorge Luis Borges’ “Library of Babel,” which, as you wrote, uses essentially the same mechanism.

Bookstaber: Right. Borges imagines a library consisting of all possible 410-page books, created by combining the letters of the alphabet, punctuation, and spaces in all possible ways. Most of the books are gibberish, but the library will also contain every coherent book ever written as well as every book not yet written.[3] Every possible state of nature that can possibly occur is described in one of the books, but there are more books than you could ever access.

So Borges, like the Game of Life, described a world that, at one level, is completely deterministic and that also spans all possible occurrences or state of nature, but in reality is one of radical uncertainty.

Siegel: This is heavy stuff – and fun stuff. But let’s return to finance.

Is the financial system too complex? As we react to different events by adding new features to the financial system, the complexity of the system increases, with each new problem calling forth a solution that then creates a list of new problems. In the past, in A Demon of Our Own Design, you’ve emphasized this concern.

Recently, however, Tom Coleman, a University of Chicago professor who was, like you, a director of risk management at Moore Capital, discussed this issue with me. He expressed the following concern:

If you go back to the late 1700s and early 1800s, they had many more financial crises then than we do now. And the securities were not complex; they were basically Treasury bonds and a few equities.

You don’t need financial complexity, then, to get crises and crashes. Go back in history and read the contemporary accounts, or read Reinhart and Rogoff. None of these problems are new!

How do you respond?

Bookstaber: It depends what you mean by complexity. I don’t mean that financial contracts use a lot of difficult words, are non-linear, or require hard math to understand.

What I mean by complexity is that we interact. When we interact, those interactions change our environment, which in turn changes the way we interact. Through this process we end up in a world that has computational irreducibility, emergent phenomena, non-ergodic processes, and radical uncertainty. These are all things that just innately occur because we interact: when we interact, we change the environment, and the environment changes us.

If you follow that dynamic over time, it will look very complex because of all the feedback loops and other effects. So, as I said, you don’t need complex securities to get an incredibly complex system. It’s the dynamic, the fact of all these agents interacting that leads to a complex result.

This was true in 1800 and 1900 because we were the same human species back then, and explains why there were crises and crashes even though the actual securities being traded were simple.

Siegel: Should we have a financial system with no crises? Is there a benefit that we give up by always avoiding crises?

It occurs to me that crises and crashes have the positive effect of correcting overpricing, of making things more affordable. That certainly happened with housing after 2008. The period ended with the best housing affordability index ever recorded. It’s true that we went through the 2000-2002 bursting of the tech-stock bubble without a financial crisis, but that is very unusual. More typically you get some sort of crisis with a large price correction.

Bookstaber: I think you’re always going to have crises. People get over their skis some way or another. They try new things that look fine so they do more of it, and that still looks fine, so they do even more and eventually become over-leveraged, over-concentrated, or whatever. So, you can have mistakes and people can lose money because of them.

Let’s say that there are people who are overleveraged in a particular market and that suddenly prices dropped and now they are forced to liquidate. They are losing 10%, then 30%, then 50% on their money. That’s fine – you made a bad bet. Some people are going to be out of business, and that is the end of that.

I guess you could call that a crisis, but I would not. A crisis occurs when linkages that exist in the financial system cause collateral damage. Collateral damage occurs when financial institution A can’t pay its obligations to financial institution B and, all of a sudden, a single woman in Des Moines who has no dealings with either institution can’t support her kids.

Siegel: So how do you allow the price corrections within a market but not the overspill that causes collateral damage?

Bookstaber: You could do it by having an agent-based model where the regulators could say, “We see these guys are getting over their skis. And, if such-and-such occurs, we could see how this could cascade out and propagate to other areas.” The regulators could thus take action. At least in theory. But they are usually very slow on the draw, and go to great lengths to avoid creating moral hazards, so they underreact to these kinds of situations.

Siegel: What is the alternative to having regulators serve this function?

Bookstaber: The alternative is to have people who have a lot of capital on hand and who are not leveraged – people who have long time frames. They might say, “I see these guys are super leveraged. They are into a market that is becoming way too crowded. They are starting to have to sell. And they are going to have to sell other assets besides the ones that are under stress, because the markets for the thing that they really needed to sell are so weak. Prices are going down 10, 20, 40, 50 percent.”

“We understand what is going on,” they would say, “and we can go in and supply liquidity in that market. Prices are down 20% and we will buy. Because we have a lot of capital and we are willing to buy, prices don’t go down 40%. And because prices are not going down 40%, there is a whole other set of markets that doesn’t get enmeshed into the crisis.”

Siegel: Who would play this role?

Bookstaber: Primarily asset owners – pension funds, endowment funds, sovereign wealth funds. They have a very long time horizon, because the liabilities that they were organized to pay arrive very slowly, over years or decades.

Siegel: Why don’t asset owners play this role already?

Bookstaber: In a small way, they do, through various intermediaries such as investment management firms and hedge funds that they hire. However, the stabilizing function of asset owners could be much larger and more effective.

The asset owner could say, “I know what’s going on, because I have a model, an agent-based model, that helps me understand it. And, on that basis, I’m willing to come in and buy. I’ll make money in the process, but I will be providing a social benefit as well, by reducing propagation.”

Siegel: Thank you very much.

[1] The game of Life was invented in 1970 by the University of Cambridge mathematician John Horton Conway and was introduced in Gardner, Martin. 1970. “Mathematical Games – The fantastic combinations of John Conway's new solitaire game ‘life’,” Scientific American 223: 120-123. [October].

[2] Bookstaber, Richard. 2017. The End of Theory: Financial Crises, the Failure of Economics, and the Sweep of Human Interaction. Princeton, NJ: Princeton University Press.

[3] Borges, Jorge Luis. 1941. “The Library of Babel,” in The Garden of Forking Paths. Full text online (translation by Andrew Hurley) here. In an interesting aside, the philosopher and logician Willard Van Orman Quine noted that, if the library of all books can be created using combinations of the letters of the alphabet and other symbols, it can also be created using just combinations of the numerals 0 and 1 (or, in Quine’s rendering, dot and dash). Thus the Game of Life contains every good and bad book that can ever be written as well as the right and wrong answers to every possible question!

Jonathan Basile, an American graduate student, programmed the Library of Babel simulation. It is here. The results are discouraging.

Read more articles by Laurence B. Siegel