An often-touted advantage of annuities is that they offer mortality credits due to the pooling of mortality risk – survivors receive a return boost from those who die. Although the general concept of mortality credits is widely understood, the underlying math is not. Understanding the math can help with decisions such as the best age to purchase an annuity and which type of annuity to purchase. Such an understanding can also be useful in debunking some popular beliefs about annuities.

For this article I’ll concentrate on “fixed” annuities that provide lifetime income. These include:

- Single-premium immediate annuities (SPIAs), which pay a lifetime income beginning at purchase;

- Deferred-income annuities (DIAs), which pay lifetime income after a delay period; and

- Qualified longevity annuity contracts (QLACs), a subset of DIAs that are funded through an IRA or other qualified retirement plan where the payments begin after age 70 ½.

I’ll base the examples on annuities that provide level nominal payments (rather than payments that increase to adjust for inflation), because they are the most popular and provide easy comparisons among SPIAs, DIAs and QLACs. This will be a pre-tax analysis, most applicable to funds held in qualified retirement plans. The analysis gets more complicated for taxable funds.

Mortality credit math

We’ll start with an example of a SPIA purchased by a 65-year-old female that will provide level annual lifetime payments, with the first payment one year after purchase. Based on rates provided by the annuity pricing service CANNEX as of late June 2017, the average of the best three prices from the 20 companies CANNEX monitors is an annual payment of $6,520.09 based on a $100,000 purchase. This can also be stated as a payout rate of approximately 6.52%.

Before calculating the value of mortality credits, we first need to estimate the internal rate of return that a purchaser of such an annuity could expect to earn, which is a function of expected longevity. I based my longevity estimates on the Society of Actuaries’ 2012 individual annuity mortality table and applied a projected mortality improvement scale. Using this approach, the average age at death for a 65-year-old female is 90. This may seem surprisingly old for those used to Social Security statistics and other published sources, but this table assumes that annuity purchasers will be a healthier-than-average. Also, there is evidence that socio-economic status affects longevity prospects and we would expect typical advisor clients to be somewhat upscale.

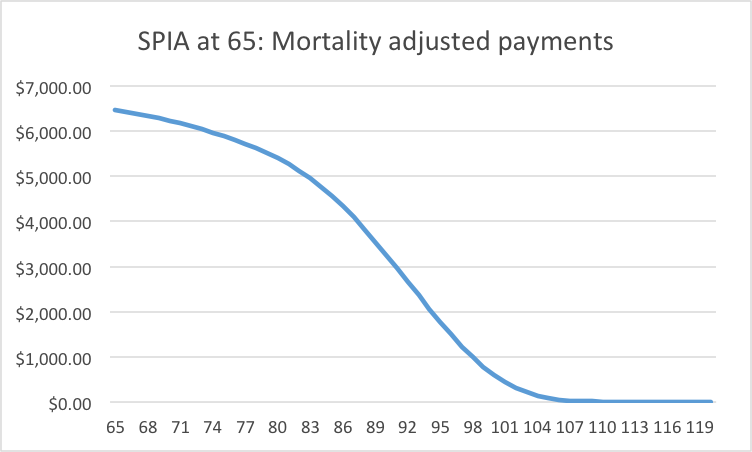

To calculate the IRR, we use the mortality table to estimate the percentage of survivors at each age and then multiply this percentage by the $6,520.09 payout. This produces declining expected payments by age as illustrated in the following graph.

We can then use the EXCEL IRR function with the initial $100,000 outflow to calculate the IRR for the expected annuity payments – 3.60% for this particular example – and this is analogous to the return calculation for a bond or a mortgage investment. Mortality credits reflect the fact that in any given year after purchase, annuitants who survive receive not only the 3.60% return, but also a return “bonus” from those who don’t survive and sacrifice their future payments. The leveraging factor is the one-year survival rate. Using age 80 for example, the survival rate from the mortality table from age 80 to 81 is 97.8771%. The mortality-adjusted return at age 80 can be calculated as (1.036)/.978771 – 1 = 5.85%. The mortality credit at age 80 is the difference between the mortality adjusted return of 5.85% and the IRR of 3.60%. So an 80-year old who survived to 81 gets a return bonus of 2.25% on top of the base 3.60%.

There’s another way of doing this calculation that provides an additional insight. This simple SPIA does not have a refund provision, so those who die in any given year will experience a negative 100% return since payments for the SPIA in this example are not made until the end of each year and their expected present value of remaining annuity payments goes to zero. We know that the combination of those who die and those who survive will earn the overall IRR of 3.60%. The 3.60% works out to be the weighted average of the -100% and the mortality adjusted return, with the weights being the 1-year death rate and its complement, the survival probability. For this age-80 example, we solve for X in the equation: 3.60% = 2.21229% * (-100%) + 97.8771% * X; X again equals 5.85%.

This latter version of the equation raises the question of whether this mortality credit is worth anything special. At the start of any given year an annuity owner has some probability of dying that year and suffering a 100% loss versus a probability of surviving and earning a mortality-adjusted return. But the expected return based on the probabilities is simply the IRR. So how can we say that the annuity is offering a mortality credit or premium over the IRR?

The answer depends on how we think about the benefits provided by the annuity. Let’s say the annuity was purchased to provide lifetime income to pay for basic living expenses – a typical use. When an individual dies, their annuity income stops but so do their basic living expenses. So the annuity purchase provides a hedge for expenses; there is no financial loss at death that adversely affects heirs. The mortality-adjusted returns provide an extra boost to generate retirement income beyond what the IRR provides.

SPIA analysis using mortality credits

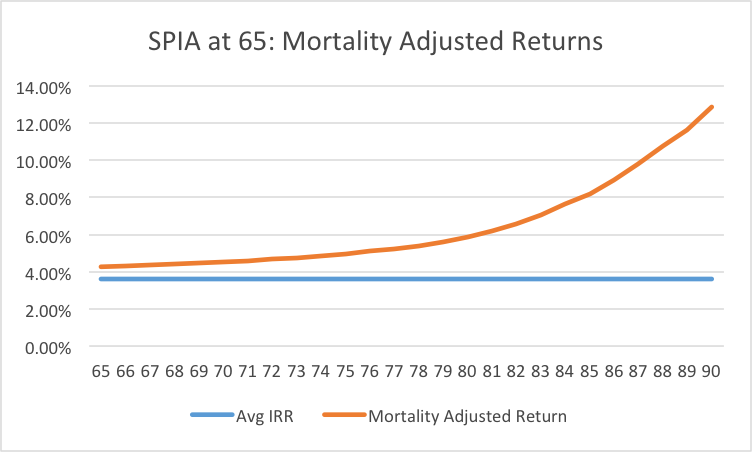

The following chart plots mortality adjusted returns and shows how they increase with age.

When considering purchasing a SPIA, it’s worth comparing the initial year mortality adjusted return to market bond returns for a duration and credit risk profile similar to a SPIA, perhaps an average credit investment-grade bond. If the bond returns are higher, it would be smart to wait and do the SPIA purchase some years hence. Purchasing a SPIA involves a loss of liquidity and flexibility, so one needs to be able to earn a premium over bonds on a mortality-adjusted basis for the purchase to make sense. There’s no easy way to measure the amount of premium needed, but zero or a negative premium is a “no-go.”

The mortality-adjusted returns for this product start at 4.27% at age 65. As of late June 2017 when this SPIA pricing was obtained, the yield for similar duration Treasury bond (about 12 years) was 2.35%. If we add 100 basis points for credit spread, that would be 3.35%, and even if we stretched to 4.00%, the initial mortality-adjusted SPIA rate would still be higher. So we don’t have a “no-go” signal for this case.

Note the upward curve of the mortality adjusted returns. In the early years after purchase, these returns are attractive relative to bond returns, and when we get older ages (early to mid-80s) these returns become attractive relative to what we might expect from stocks. For an individual whose primary focus is generating secure lifetime income, it could be argued that at higher ages SPIA ownership make a lot more sense than stocks – similar expected returns and a lot less risk. However, this requires that the individual has other savings for unexpected expenses (and for potential LTC needs), so the SPIA ownership can be dedicated to income generation.

This mortality credit math is not new; it was illustrated by Professor Moshe Milevsky in this 1996 paper with much more elegant mathematics than I have presented here. His focus was on when to purchase a SPIA and, unlike me, he concluded that it made sense to wait until some years after retirement. However, since that time, there have been declines in interest rates, annuity pricing margins and stock market return expectations, and these changes now favor an earlier SPIA purchase. In the past few years thought leaders Wade Pfau, Michael Kitces, Michael Finke, and David Blanchett have all written articles and done presentations on mortality credits and the paired concept of mortality pooling. They have used a variety of approaches to illustrate the benefits of annuitization.

A QLAC example

A typical QLAC would be an annuity purchased at age 65 with qualified funds providing lifetime payments that begin at age 85 after a 20-year deferral. This product would deliver tail-risk (late-in-life) longevity protection, rather than providing income for all of retirement. Because of the long deferral, payout rates are much higher than for SPIAs. Using our example of a 65-year-old female and CANNEX rates, a $100,000 purchase at 65 would pay annual $38,332.16 starting at 85 – a payout rate of 38.33%. This pricing is for a no-refund version that makes no payments for deaths prior to 85.

I’ve seen the following written about QLACs:

- An advantage over SPIAs is that QLACs minimize the impact of insurance company charges by making it possible to fund the bulk of retirement with regular investments.

- By concentrating payments late in life, QLACs make more effective use of mortality credits than SPIAs do.

It’s worth examining these claims. Regarding the first one, it’s necessary to estimate the returns that could be earned from regular bonds, or bond funds, during the deferral period until the QLAC kicks in at year 20. The duration for such payments is close to that of a 10-year Treasury bond that was yielding 2.22% in late June 2017 when this analysis was done. If we add roughly 80 basis points for corporate bond credit spread, we’d have a yield of 3.00%. As mentioned earlier, the IRR for a SPIA starting at 65 was 3.60%, which calls into question the claim that regular bond investments can beat insurance company products. If we design a level payment product that uses 3% bonds to generate income for the deferral period and then transition to a QLAC producing the same payments, a $100,000 investment in the QLAC plus the bonds will generate $5,903.26 of annual income. This would be about a 10% reduction from the $6,520.09 produced by a SPIA purchased at 65. So, for this example, heavier reliance on regular investments fails to produce the claimed effect.

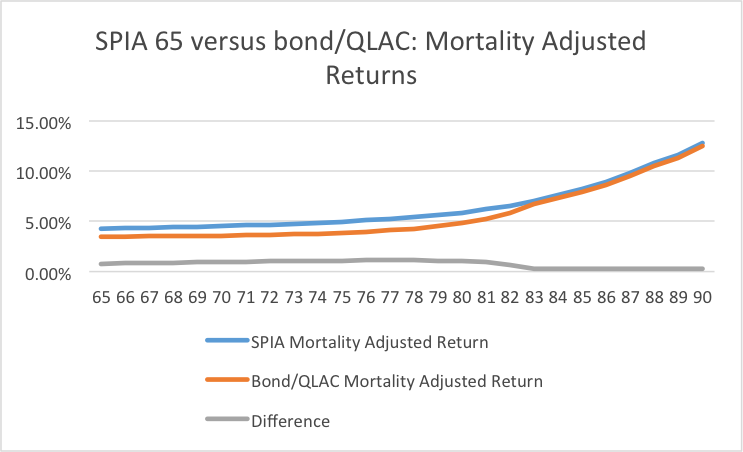

The second claim can also be challenged because it reflects a fundamental misunderstanding of how mortality credits work. The following chart compares year-by-year mortality-adjusted returns for our SPIA example to those for a bond/QLAC combo.

Focusing on the right side of the chart (after the QLAC payments begin), we see that the mortality-adjusted returns are a close match for the SPIA and QLAC. If we recall the formulas for calculating a mortality adjusted return at a given age, we see that the primary determinant is the survival rate, which is a function of age. It doesn’t matter when the product was purchased or when the payments begin. So the QLAC structure does not offer an advantage of higher mortality credits.

Moving to the left side of the chart, we see that during the deferral years when income is provided by bonds, the mortality-adjusted returns are lower for the bond/QLAC than for the SPIA. If we recall the weighted average formula for mortality adjusted returns for the no-refund SPIA, deaths during any year produced a -100% return. With the bond/QLAC combo, deaths during the first 20 years provide remaining bond funds to heirs, so the returns are still negative, but not -100%. A less negative return on death results is a less positive mortality-adjusted return since the combination equals the IRR.

Pre-retirement DIAs

In two prior article (here and here), I challenged claims about the benefits of purchasing DIAs prior to retirement. A typical structure might involve purchasing a DIA at age 55 that begins payments at 65. Again using CANNEX data, a DIA based on this 55/65 structure would generate $8,532.26 annually beginning at 65 based on a $100,000 purchase. This particular structure I chose involves a cash refund of any of the $100,000 premium not recovered from annuity payments, so there would be a $100,000 refund during the 10-year deferral period and a declining refund for 18 years after that. The reason I favored this structure was that I was particularly concerned about financial exposure during the working years when death at a relatively early age would likely cause financial hardship. It turned out that this refund provision only reduced payments by about 4% compared to risking a no-refund approach.

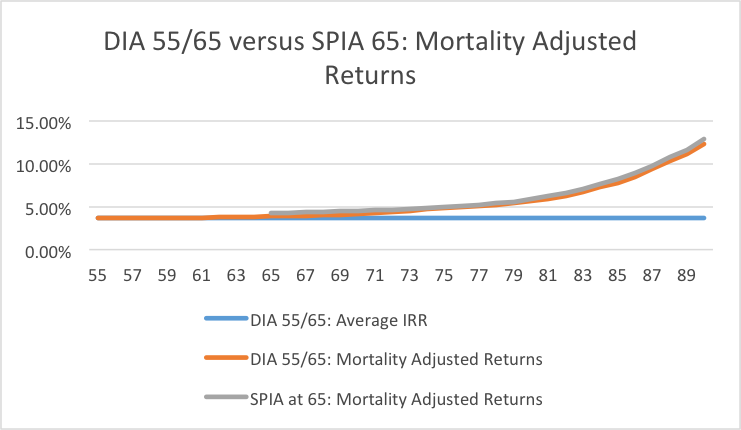

The following chart compares results for the DIA 55/65 structure versus a SPIA at 65.

On the left side of the chart we see minimal mortality credits because, during the 10-year deferral period, mortality-adjusted returns barely rise above the average IRR, which is 3.65%. The actual mortality-adjusted returns are 3.66% for age 55 and only rise to 3.83% by age 64 at the end of the deferral period. So there is minimal advantage from buying a DIA at 55 versus waiting to buy a SPIA at 65. These meager mortality credits reflect low mortality rates at younger ages and the refund structure for the DIA product. After age 65, the DIA and SPIA mortality credits are similar, again demonstrating that mortality credits are mainly a function of mortality rates which are a function of age.

Final word

Although a general grasp of the concept of mortality credits is useful in understanding the value that annuities provide, it’s worth having more in-depth knowledge of how mortality credits are calculated. Such an understanding can be useful in decisions such as when to annuitize and the choice of particular annuity products or product structures.

Joe Tomlinson, an actuary and financial planner, is managing director of Tomlinson Financial Planning, LLC in Greenville, Maine. Most of his current work involves research and writing on financial planning and investment topics.

Read more articles by Joe Tomlinson