|

| Jack Bogle and Ted Aronson |

Speaking two weeks after his 88th birthday, Jack Bogle called the fiduciary rule “silly” and said that financial advisors’ fees are heading lower. Indeed, he said, advisors are destined to charge hourly or retainer fees, like lawyers and accountants.

Bogle is the founder and retired chairman of Vanguard Investments. He spoke at the CFA Institute’s Annual Conference, held in Philadelphia. He spoke for about 20 minutes and was then interviewed on stage by Ted Aronson, the founder and managing principal of AJO Partners, a Philadelphia-based active manager of equities.

“The fiduciary rule is silly because it applies only to retirement plans,” Bogle said. He said that brokers will be in a compromised and uncomfortable position when they work with a client who has retirement and non-retirement portfolios, under the fiduciary and suitability standards, respectively. The SEC will need to step in and make the fiduciary rule apply universally, according to Bogle.

Despite his prediction of fee compression, Bogle was upbeat about the future of the advisory business.

He said that he has “a lot of respect for RIAs,” but cautioned them to avoid individual stock trading, and instead to rely on asset allocation, which he said is “not as complex as it used to be.”

“Concentrate on what can really help the client,” he said, “like explaining the implications of market timing and the complexities of retirement and tax planning.”

He was far less sanguine about the future for active managers.

Reflections on a revolution

“The realm of investing has been no exception to the rise of innovation,” Bogle said.

Just as innovation has upended the media, music, retailing and transportation industries, it is slowly transforming the investment management business, according to Bogle.

He was not referring to so-called robo advisors, which he said are unlikely to have a significant impact. The transformative innovation is the availability of information that has exposed the high fees charged by some active managers and the overwhelming advantage of traditional index funds (TIFs).

“So far,” he said, “the index revolution has claimed no victims.”

But, he said, “Everything happens at the margins.” He noted that over the last decade, TIFs have had $1.3 trillion of inflow and active funds have suffered $1.1 trillion of outflows.

“That trend seems to be accelerating,” Bogle warned. “We are on pace for the biggest year for index flows and the second worst year for active funds.”

“Indexing is not a fad or fashion, but a fact of life,” Bogle said.

The failure of active management has gone unnoticed by consumers because the absolute returns were very good, according to Bogle. Since 1900, he explained, U.S. stocks have had a nominal return of 9.5%, consisting of 4.4% from dividends and 4.6% from earnings growth, which Bogle collectively termed the “investment return,” plus another 0.5% in P/E expansion, which he called the “speculative return.”

Since 1982, the results were even better: 3.3% from dividends, 5.4% from earnings growth and 3.4% from P/E expansion, for a nominal return of 12.1%. Active managers who charged high fees were still able to produce decent absolute returns, and their underperformance relative to TIFs was largely unnoticed by investors.

Looking forward, Bogle said, in the next 10 years investors should expect only 2.0% from dividends and 4.0% from earnings growth. With P/E ratios at 26.3, Bogle said investors could expect to lose 2% from P/E contraction, for a total return of 4.0%.

“Future returns will suffer as well,” he added, “as fund expenses will take a larger chunk of returns.”

Pension funds, smart beta, survivorship and other thoughts

Pension funds are courting disaster, Bogle said. Those who manage the $1.5 trillion in pension assets are assuming 7.5% future returns, which Bogle said was entirely unrealistic. For those portfolios, he said, “5% looks like a stretch. The word ‘crisis’ is appropriate.”

He was similarly critical of smart-beta funds, which he loosely defined to include strategies such as value, growth and fundamental indexing.

“Smart beta is not a terrible idea, but it’s not a world changing idea,” Bogle said.

Those strategies rely on heavily mined data and ignore the principle of return to the mean, which Bogle said is a “huge mistake.” He likened smart beta to the “go-go” strategy of growth investing that was popular in the 1950s – both were popular fads that drove fund creation.

“Successful short-term marketing strategies are rarely, if ever, successful long-term investment strategies,” Bogle said.

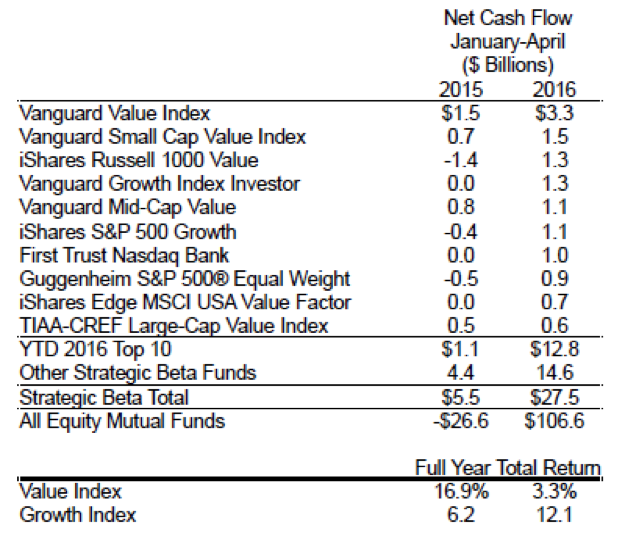

He provided the following table to illustrate the recent growth of smart-beta funds, as well as the inconsistent performance of value and growth over the last two years:

Bogle was particularly critical of the Research Affiliates fundamental indexing (RAFI) funds, which he called “closet indexers,” claiming that they have a 97% r-squared to the broader market with lagging risk-adjusted returns and Sharpe ratios.

Investors overlook the long-term impact of fund survivorship, according to Bogle. He said that only 57% of active mutual funds from 10 years ago are alive today. A 30-year-old investor with a four-fund portfolio will experience 37 fund failures, Bogle said.

“What are the chances that investor will match the returns of the index?” he asked, rhetorically.

The future of active management

As I have written, Bogle predicts that actively managed mutual funds are an obsolete business model – especially publicly owned fund companies.

S&P index funds are a commodity, he said, where competition is based purely on price. Bogle said that he “fired a shot across the bow” many years ago, when he created Vanguard’s Admiral Shares and cut fees in half based on a $25,000 minimum. He said that some TIFs have managed to reduce their expense ratios to zero and make money through securities lending, a strategy that he does not like.

“The index fund is abhorrent to a profit-making business,” he said, since it is motivated by lower costs.

By contrast, he said the mutual structure of Vanguard’s business give it a client orientation that is “priceless.”

ETFs face a significant risk due to lack of liquidity, according to Bogle. That applies to sector funds like high-yield bonds and gold, but not to broader market ETFs. “At the margins I can see real problems,” he said, “even beyond those specialized ETFs.”

He called leveraged funds and ETFs that bet on down markets “asinine.”

Indexing represents 36% of equity funds and 22% of the total U.S. market, according to Bogle. It will get to 50%, he said, but that will take 10 to 15 years; it will never get to 75%. Indexing is a way to neutralize a certain portion of the stock market, he said, shrinking the universe in which active managers can compete. “As this happens,” he said, “it will be easier for some managers to win, but also for others to lose. Markets are highly efficient but could get a little less efficient.”

Index funds need to take a more active role in management, Bogle said, and give more careful consideration to proxy voting. He said that Vanguard has 30 analysts working on corporate proxies to ensure that each company is run in the interest of its shareholders. He said that index investors have a duty to society, the community and investors to be good fiduciaries.

One issue facing index funds is industry concentration. Bogle said that the three biggest index fund companies – BlackRock, State Street and Vanguard – collectively own 22% to 23% of all stocks. This could create anti-trust issues, he said. “I was too stupid to realize that by giving investors the best possible deal, I would build a colossus,” Bogle said, sarcastically.

“At some point, we will need to worry about government intervention,” Bogle said.

Read more articles by Robert Huebscher