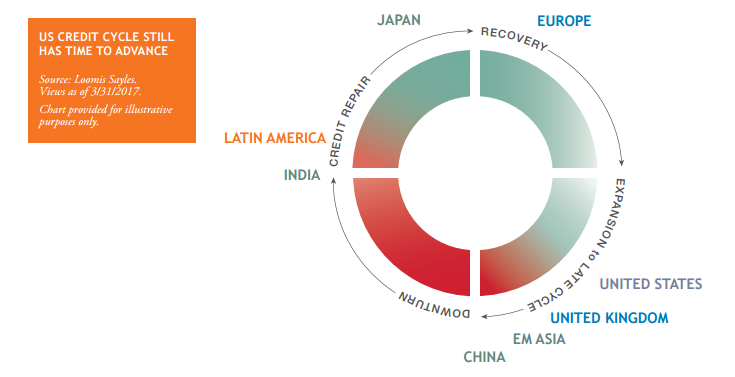

A synchronized pickup in global economic activity has lifted the spirits of businesses, consumers and investors worldwide. Though many equity markets are near 52-week highs and credit spreads are near multi-year lows, we still believe the US credit cycle has time to advance in its later stage.

Less Accommodative Monetary Policy is Slowly Emerging

After years of monetary stimulus, the world’s major economies are starting to see firmer growth and inflation, and policymakers are slowly shifting gears. The Federal Reserve (Fed) has ratcheted up rates three times since the economic recovery began, and the central bank looks positioned for two more hikes this year and three next year. In Europe, the European Central Bank (ECB) is trimming monthly asset purchases and inching away from ultra-accommodative policy, but the process of interest rate normalization is expected to be slow and take several years. Improving global growth and gradual steps toward less accommodative policy have limited US-dollar strength so far this year.

Though growth and inflation are headed in a positive direction, the long-term trajectory looks moderate, with no sign of an impending economic boom. US consumer confidence has reached pre-recession highs, and small business optimism has skyrocketed to levels not seen since 2004, but exceptionally high policy uncertainty could be limiting the passthrough to actual economic indicators like private non-residential fixed investment. Consensus expectations suggest US real GDP will grow at an annual rate of around 2.0% through 2019 and core personal consumption expenditures (PCE) will hover around 2.0%. The goldilocks economic backdrop means the Fed can tighten, but should do so cautiously.

As the credit cycle progresses, we expect only modest upward pressure on long-term US yields. A flatter US Treasury curve is expected as yields at the front end of the curve rise faster and by more than those at the long end. In this environment, we believe return prospects for risk assets will continue to look favorable relative to developed market (DM) government bonds.

Economic Backdrop Still Credit Positive

Global growth is expected to pick up modestly over the next two years and corporate profits are now growing again in most countries, two factors that could help higher-yielding credit products generate excess returns over government bonds. Though the US and UK are in later stages of expansion than Europe, corporates in each region can perform well if growth and business conditions continue to improve.

In aggregate, US investment grade corporate leverage has reached new highs, but when commodity-related sectors and financials are excluded, gross leverage has recently trended lower. Investment grade option-adjusted spreads are near their lowest levels since the global financial crisis, but modest excess returns could be achieved from here as corporate earnings recover. US high yield bond spreads have risen around 50 basis points from recent lows made in early March but remain tight relative to history. A reacceleration of corporate profit growth and the expected advance in US GDP, albeit slight, should help slow the credit rating downgrades seen recently.

Corporate health should continue to strengthen in Europe, where profits have been mixed at the sector level and slower to advance relative to other countries. Within the investment grade space, UK corporates have led performance globally over the past 12 months, and downside risks—like messy Brexit negotiations and the end of Bank of England (BOE) buying—look manageable at present.

Emerging Markets in Position to Benefit

With US corporate yields near the low end of their historical ranges, and the UK and European corporate markets yielding even less, those looking for more yield can currently find it in emerging market (EM) sovereign and local currency bond markets. Within EM, individual country performance will likely be driven by political and economic idiosyncratic developments, but broadly speaking, EM assets can benefit from the fundamental improvement we see globally.

US-dollar-denominated EM sovereigns offer US investors the potential to earn carry over US Treasurys without taking currency risk. If US Treasury yields rise slowly as expected, it should limit upward pressure on dollar-denominated sovereign yields. After lagging for five years, EM corporate earnings are finally growing faster than DM earnings, a factor contributing to EM equity outperformance year to date. Additionally, the emerging to developed real growth differential is expected to improve in favor of EM, which could provide an additional tailwind to the asset class.

Equity Valuations Supported by Low Yields and Profits Recovery

The US has been largely alone in generating healthy stock market returns in recent years, but performance appears to be in the early stages of broadening. Global economic data like Purchasing Managers’ Index (PMI) readings and surprise indices are supporting equity sentiment. Developed market equities are posting respectable gains so far this year, led by technology and healthcare. Emerging markets have also gotten off to a strong start.

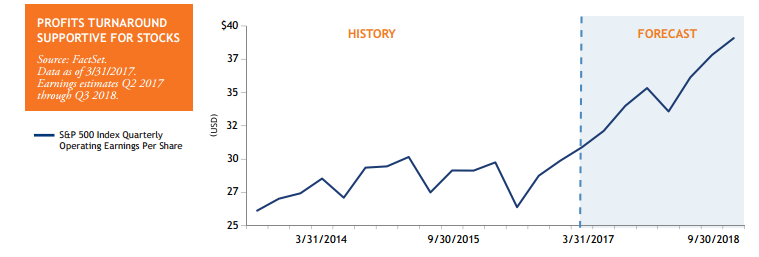

Ultimately, stock market prices will reflect macroeconomic conditions and earnings coupled with dividend payout growth and other shareholder-friendly activity, like buybacks. We don’t think higher interest rates will hamper support for equity market valuations in the medium term. If yields rise gradually as we expect, the 10-year Treasury may not reach and sustain 3.0% until the middle of 2019. A 3.0% yield on the 10-year Treasury would still imply valuation support for stocks, which are trading at about 17.5X operating earnings estimates for 2018. Equities continue to have a strong cash return story, even with interest rates having moved higher since bottoming last year. The S&P 500® Index sports a current yield of about 2.0%, a level that has been fairly consistent in recent years.

Dividend increases have been running strong since 2011, and we expect mid- to high-singledigit cash dividend growth this year and next as modest economic growth continues. Share repurchases remain an ongoing benefit to valuations as well. When combining net share repurchases with dividend yield, we currently find the effective yield of the S&P 500 to be above 4.0%, significantly higher than the current 2.35% yield on the 10-year Treasury. While some may forecast a further pickup in share repurchases, we think a balanced approach to corporate spending, including share repurchases, cash dividends, mergers and acquisitions and capital expenditure, implemented over time is the most likely scenario.

Developments in Washington Could Bring Positive Catalysts

The 2017 policy agenda in Washington, D.C., will take time to play out, with considerable uncertainty over the extent and timing of change. Corporate tax reform, incremental infrastructure spending and potential regulatory reforms are all on the table and could be positive catalysts. The US has one of the highest statutory corporate tax rates in the world, and if tax rates could be brought down to the global average of 23.6%, many companies would benefit. Additionally, US companies would face less pressure to engage in aggressive global tax structures if tax rates were reduced. Of course, many companies do not pay taxes at the statutory rate, so not all will benefit—especially if certain tax preferences are reduced or eliminated. The details will make the difference, and we believe it is too soon to have a strong view on the outcome. Corporate earnings may rise a bit with tax reform, but a continuation of the current economic expansion is far more important than a modest earnings-per-share boost.

Disclosure

This commentary is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product.

Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice.

Past performance is no guarantee of future results.

Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index.

This document may contain references to third-party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Loomis Sayles & Co.,

L.P. and does not sponsor, endorse or participate in the provision of any Loomis Sayles services, funds or other financial products.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR016950