Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

When most investors think about “risk reduction” their minds immediately conjure volatility and losses. We cover strategies and products for downside protection at length in our discussion with clients. However, as advisors we should consider a broader definition of risk that connects more directly to how clients feel about their investments. Specifically, advisors should define risk as the probability that clients won’t meet their financial goals. Advisors should have the singular objective of minimizing this risk.

This new definition of risk profoundly shifts the conversation away from volatility and losses, and toward strategies that also achieve minimum required returns. From this new perspective, it is not sufficient to manage risk and provide downside protection; an investment strategy must also produce returns that fulfill long-term goals. Moreover, the strategy must account for the fact that investors are susceptible to shorter-term dynamics, such as tracking error relative to domestic benchmarks, which may run counter to the objective of long-term wealth maximization. In other words, advisors need to build portfolios that are financially optimal, but that investors can stick with over time.

This is not a trivial undertaking. The current environment presents unique challenges that make it extremely difficult to engineer a traditional portfolio with expected long-term returns that are consistent with client objectives. Advisors must look to alternative sources of return to fill the gap, but this presents a different complication. These alternative sources of return will behave very differently than what clients are used to. They also come with large tracking errors to typical benchmarks. As a result, clients run a high risk of abandoning these strategies before they have a chance to perform.

Realistic expectations

First, let’s examine why traditional portfolios are unlikely to produce sufficient returns. Expected bond returns are least controversial, so let’s start there. The weighted average yield-to-maturity for the widely held iShares U.S. Aggregate Bond Index ETF is 2.55% net of expenses, with a weighted average maturity of eight years. The Barclays Global Aggregate yields just 1.66%. This is a good proxy for the actual return that investors in this fund might expect over the next decade or so.

What about stocks? Let’s start with an unbiased assumption that the equity sleeve of a typical investment portfolio will earn the historical long-term excess return of a globally diversified equity portfolio. Global equities have produced compound returns about 4.2% above T-bills over the long-term, and 3.2% above 10-year Treasury bonds[1]. T-Bills currently yield about 0.5% and benchmark Treasury bonds yield 2.35%, suggesting that a diversified stock portfolio should earn nominal returns between 4.7% - 5.5% over the next decade or so. Let’s assume 5.5% to err on the side of optimism.

This means that the most an investor can likely expect from any unlevered traditional portfolio is 5.5% per year over the next 10 years or more. To achieve 5.5%, you need to own a pure equity portfolio, with all of its accompanying risks. A traditional 60/40 portfolio will produce about 60% * 5.5% return + 40% * 2% return = 3.3% + 0.8% = 4.1% nominal. And that’s if we are being optimistic.

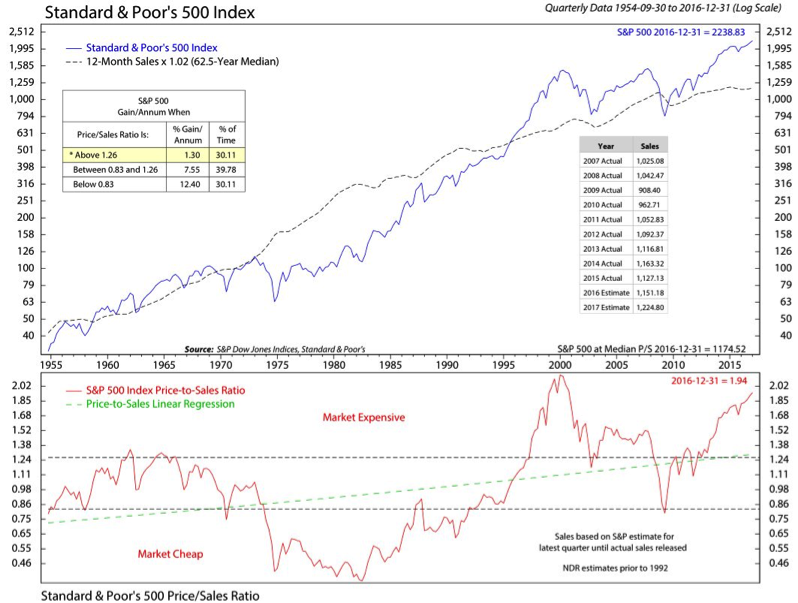

Unfortunately, there is not much reason for optimism. Stocks are expected to produce an average excess return only when they are priced near average valuations. But many stock markets are currently quite expensive. U.S. stocks, which represent over half of total global stock market capitalization, are trading near record valuations according to some measures. For example, U.S. stocks are trading near their 2000 bubble peak as a multiple of total revenues (Figure 1). Should stocks retrace to average valuations by this measure in an acute correction, investors would endure a 48% decline. If they were to mean-revert over a longer horizon, they would face a material headwind on long-term returns.

Figure 1. S&P 500 Index and Price-to-Sales ratio, 1955-2016

Source: Ned Davis Research

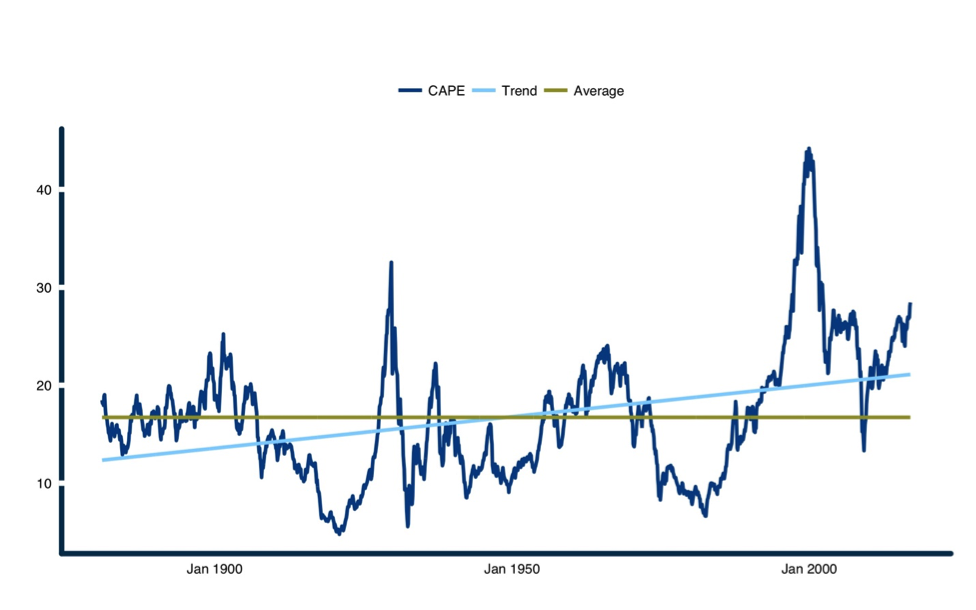

Another popular measure of stock market valuations is the cyclically adjusted price-to-earnings (CAPE) ratio, proposed by Dr. Robert Shiller. This measure accounts for the volatility of earnings through a full business cycle by taking the average of aggregate earnings over the past decade, adjusted for inflation.

By this metric, U.S. stocks are also expensive relative to history, sitting at a ratio of 28.5, about 70% above their long-term average value of 16.7.Some argue that the equilibrium CAPE should rise through time for structural reasons such as declining economic volatility, and improved stock market transparency and liquidity. This would make the long-term average less relevant. To account for this, we found the line of best fit describing the steady growth in CAPE over time. Even accounting for trend growth in multiples, stocks are still 35% overvalued (Figure 2).

Figure 2. S&P 500 Cyclically Adjusted Earnings Ratio, 1881 - 2016

Source: ReSolve Asset Management. Data from Robert Shiller

While it has paid to be optimistic about stocks over the past century, it is also prudent to be realistic about the probabilities. It is highly likely that investors will earn about 2% on high-grade fixed income, and probably much less than 6% per year on stocks over the next decade or more. After adjusting for inflation and fees, investors will be hard pressed to earn more than 2% per year on traditional portfolios.

Getting comfortable with feeling uncomfortable

It is unrealistic to expect the portfolios that investors have grown comfortable with over the past few decades to produce the returns investors need to achieve financial independence. Investors who are entrenched in the current investment model face the uncomfortable choice of working longer, saving more, or lowering expectations about their retirement lifestyle.

But investors have other choices if they are willing to think more broadly about their investment options. These choices are no panacea. While they may substantially reduce investors’ savings burden, and provide long-term returns that will support a more substantial retirement lifestyle, they inflict a different type of discomfort.

Extreme diversification

One way investors can make their portfolio more resilient to an uncertain future is to consider more comprehensive diversification strategies. Many investors would be surprised to learn that typical “balanced” portfolios composed of 60% stocks and 40% bonds actually derive over 90% of their risk from equities. This is because equities are so much more volatile than stocks. Even worse, equities only produce positive returns during periods of persistent positive growth shocks, benign inflation and abundant liquidity. While these conditions have prevailed in most years over the past few decades, there have been notable exceptions. In addition to the acute crisis periods like 2000-2002 and 2008, which many investors lived through personally, both equity and bond markets suffered through a 16-year period of low growth and high inflation from 1966 through 1982.

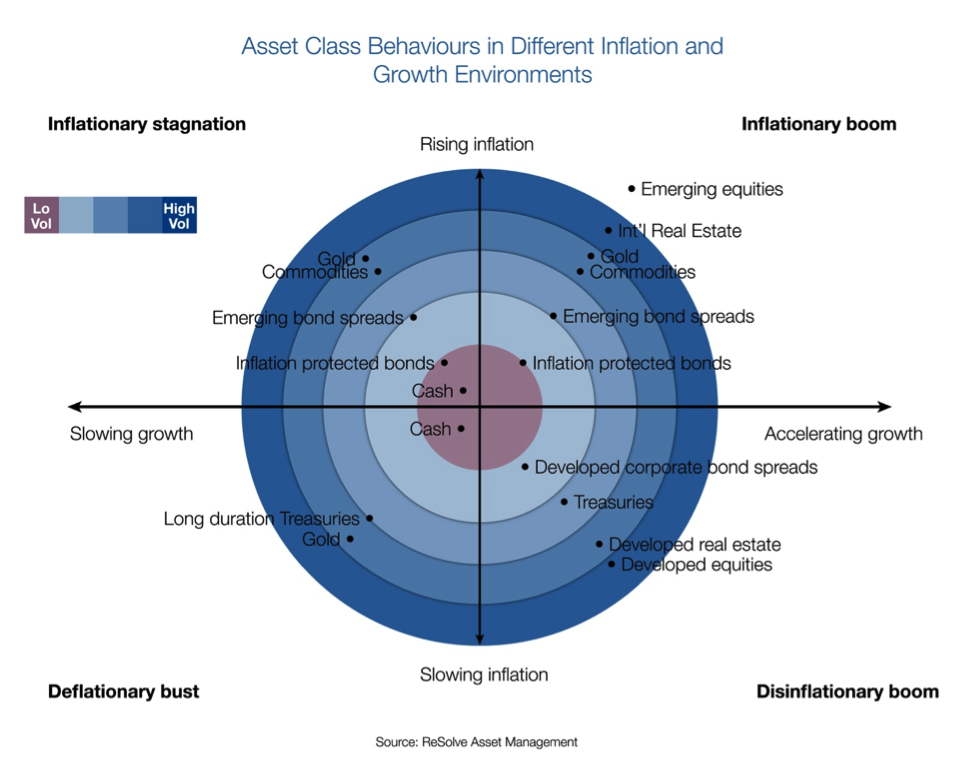

Figure 3 puts the idea of extreme diversification in context, by illustrating how various global asset classes would be expected to react to the economic effects of growth and inflation. Investors who do not feel qualified to forecast future economic environments might be well served by allocating to all of these asset classes so that they have the opportunity to profit however the future evolves. Of course, the asset classes in Figure 3 have very different risks, and complex relationships with one another. The portfolio that maximizes the opportunity for diversification across these diverse assets is called the Global Risk Parity portfolio. Learn more about the risk parity concept here.

Figure 3. Asset class responses to the four major economic environments.

Source: ReSolve Asset Management

One way to introduce the prospect of higher future returns is to introduce frontier asset classes, such as emerging-market stocks and bonds. By many measures, emerging-market stocks, currencies and bond markets represent substantially better value – and commensurately higher prospective returns – than the developed markets with which investors are typically comfortable. Consider that the Vanguard FTSE Emerging Markets ETF has a price-to-earnings ratio of 18.5, while the Vanguard US Total Market ETF trades at a multiple of 24.4. By construction, maximally diversified strategies often allocate a significantly larger portion of capital away from U.S. equities, and provide greater allocation markets that may represent better value.

When investors become acquainted with the arguments in favour of extreme diversification, they are often convinced that global risk-parity should form a meaningful portion of their portfolio. While I wouldn’t argue with this sentiment, diversification is not always an easy path to follow. Concentrated equity portfolios often deliver very exciting returns during periods of strong growth and low inflation. Diversified investors will experience this excitement, but to a lesser extent. This breeds feelings of regret, especially when investors’ domestic equity market is leading the charge. In practice, I advise clients to hold a portion of portfolios in their home equity market, and in other markets that they watch. This will attenuate feelings of regret, which often cause investors to make unwise choices under extreme emotion.

Alternative sources of return

While a certain core of financial academics continues to cling to an outdated model of efficient markets, open-minded academics, and most experienced market practitioners, now acknowledge that investors make errors. Some of these errors are truly random and are offset by equally random errors in the opposite direction. But there are some types of errors that investors make over and over again in the same way. Some of these errors are actually not errors at all. Rather, they reflect the fact that investors have a variety of preferences in markets other than a pure focus on wealth maximization. I call these investors “willing losers” because they have decided to forego wealth maximization to pursue alternative objectives.

For example, it is well known that investors in every country around the world have a strong preference to own the stock and debt of their own domestic companies. This home bias is one of the strongest and most pervasive effects in markets. Many investors also express a preference for “lottery ticket”-type investments, and investments that are popular or appear to have a good “story.” Investors also take comfort in holding portfolios that are consistent with their peer group because the pain of underperforming their friends is much more intense than the joy of outperforming them. Investors are often slow to adapt to new information, and are prone to extrapolate near-term trends while underestimating the tendency of corporate prospects to revert to the mean. These behaviours are almost universal and are observed at the highest ranks of the most sophisticated organizations. Most investment capital is still guided by humans, and humans can be counted on to behave in certain ways.

It turns out that the systematic errors above manifest in economically large effects across global markets. These effects, which are called “factors,” explain a very large portion of the differences in returns across groups of securities. If a large portion of investors can be counted on to behave in ways that leave profits on the table, then there is an opportunity for other investors – factor investors – to earn excess profits by taking the other side of those trades. And these excess profits can be very attractive for several reasons.

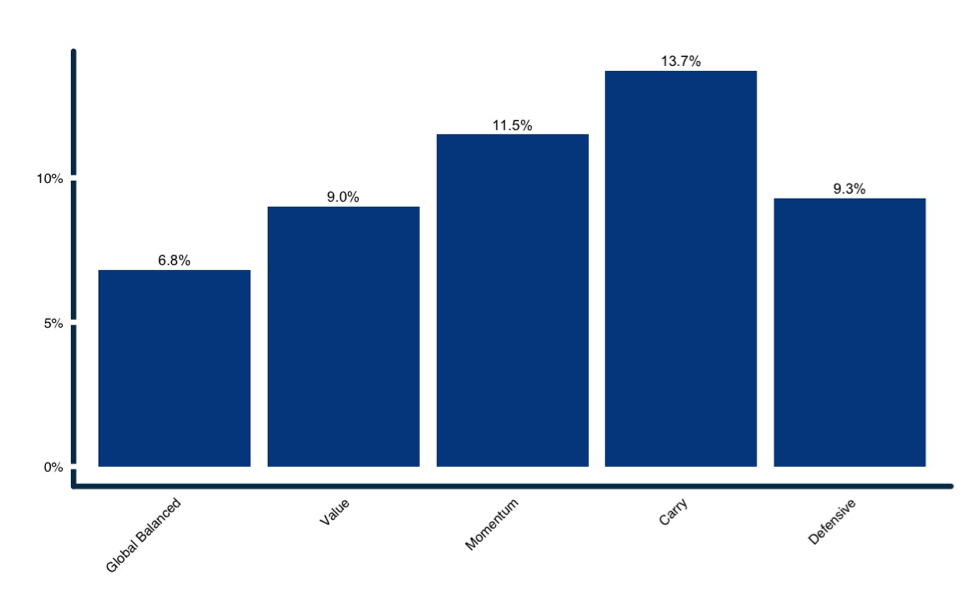

First of all, these profits can be quite large. When harvested in their purest sense across a diverse basket of global markets and securities, they have produced returns of between 9% and 13.7% per year, when scaled to about the same risk as a global balanced portfolio (Figure 4).

Figure 4. Annual excess returns to factor portfolios vs. global balanced, scaled to 10% annualized volatility, 1990 – 2012

Source: Ilmamen A.,Israel R., Moskowitz T., “Investing With Style: The Case for Style Investing” (2012)

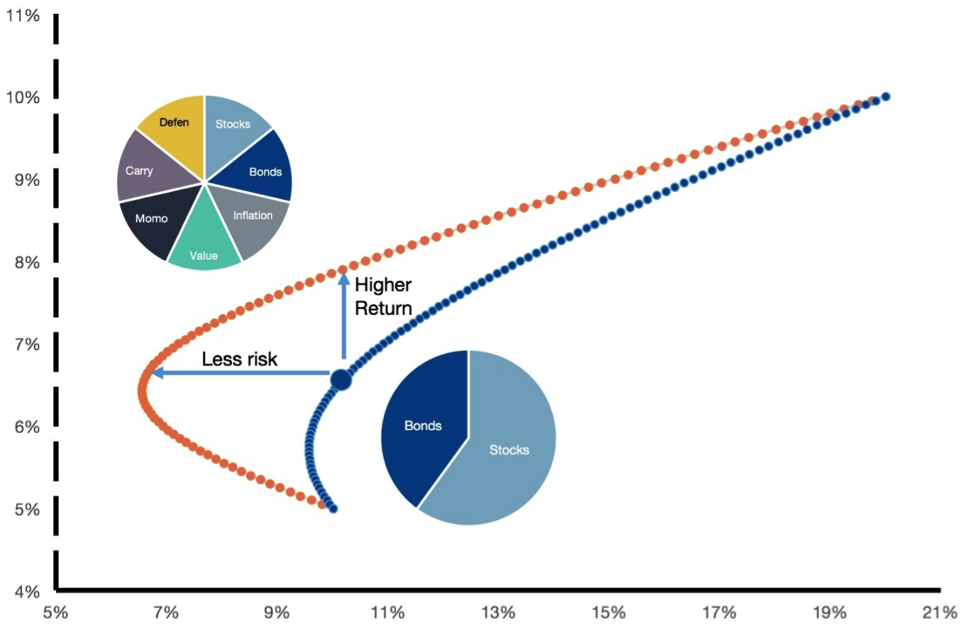

Second, their returns are unrelated to the returns of traditional assets like stocks and bonds. In fact, on average they have near-zero correlation to both equities and bonds. This means that, when they are added to a traditional portfolio, they are likely to produce substantially higher returns per unit of risk. This concept is illustrated in Figure 5, which is a stylized efficient frontier. It describes the return of the most efficient portfolio at each level of risk. The inclusion of factors moves the traditional frontier substantially up and to the left, implying both higher returns and less risk.

Figure 5. The “New Frontier” including factors. For illustrative purposes only.

Source: ReSolve Asset Management

So far I have focused on the benefits of adding factor strategies to traditional portfolios. But, as I mentioned above, factor strategies have their own set of discomforts. Remember that factor strategies work because they require investors to act against human nature. In other words, they are often counterintuitive.

Consider a global value strategy that systematically sells stocks in countries with high valuations to purchase stocks in countries with extremely depressed valuations. At the end of 2016, this strategy would have mandated selling out of U.S. stocks to purchase stocks in countries like Russia, Turkey, and the Czech Republic. Many investors would find it difficult to divest of shares that have treated them so well for the past 10 years, to purchase stocks in countries that are embroiled in war or economic turmoil. Other factor strategies are often equally difficult to execute, on an emotional level.

Another reason why investors should tread lightly into factor strategies is that they behave very differently than what we expect from traditional portfolios. For example, some strategies deliver very steady and strong returns for years at a time and then give back a large portion of returns in an acute and unexpected crisis. Some factor strategies have a history of performing at their absolute worst in periods when traditional portfolios are experiencing their best gains. These character quirks make it challenging for many investors to stick with these approaches in concentrated positions.

In addition to issues of comfort, many investors have investment constraints that make it difficult to invest in pure factor strategies. For example, many factor strategies require leverage and shorting to produce returns that are competitive with equities. For this reason, it often makes more sense to layer a factor strategy directly on top of a long-only asset allocation. That way, investors can benefit from long-only exposure to traditional sources of returns, like global stocks and bonds, while using factor strategies to enhance returns and manage downside risk.

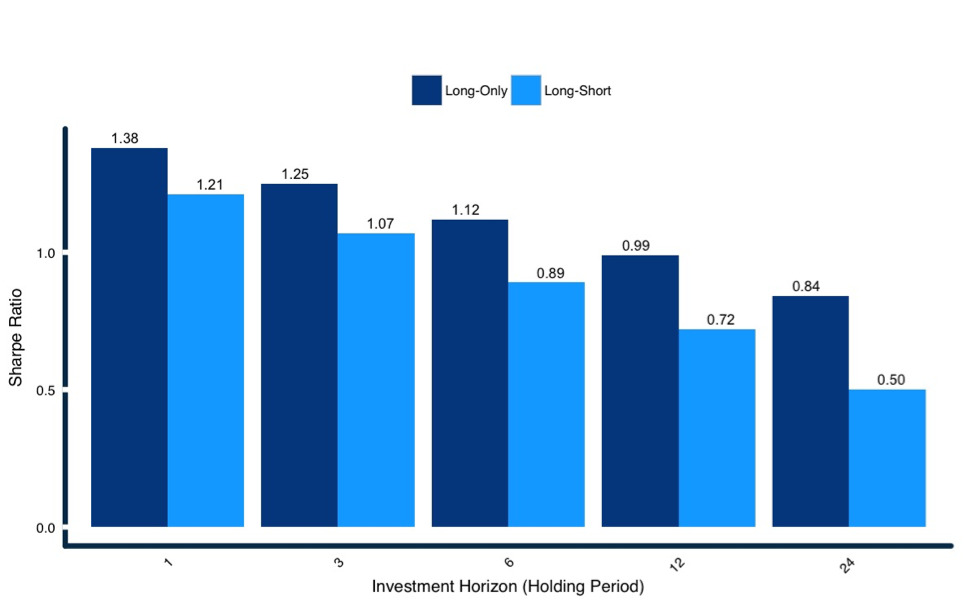

Perhaps unsurprisingly, since these strategies are allocating across assets with positive expected returns, the long-only versions of these factor strategies have historically produced stronger performance. Figure 6 illustrates the potential of a time-series momentum factor strategy applied in a long-only framework on a basket of global asset classes.

Figure 6. Sharpe ratios for long-only and long/short multi-asset Absolute Momentum factor strategies by investment horizon (in months).

Source: JP Morgan Asset Class Momentum Primer

Conclusion

Risk is the probability that clients won’t meet their financial goals. Advisors should have the singular objective of minimizing this risk. This definition of risk expands the concept to include not just the prospect of short-term losses or volatility, but also the need to generate sufficient returns in all market conditions.

Unfortunately, with low yields on fixed income and elevated valuations for North American equities, investors are unlikely to achieve their desired returns from investments in traditional portfolios. Investors face less comfortable choices now than in the past. Some investors may choose to stay the course with their investments while saving more, working longer and reducing expectations about their lifestyle in retirement.

Others may choose to explore alternative ways to construct portfolios. To protect against a highly uncertain future, investors might explore extreme diversification methods like global-risk parity. This strategy is designed for maximum resilience, but also includes frontier markets like emerging-market stocks and bonds to boost returns. Others may seek higher returns and the potential for lower risk by allocating to alternative return premia – factors – that arise from other investors’ mistakes. Long-only multi-asset strategies may offer the best of both worlds for many investors with typical constraints.

None of these choices is without risk or discomfort. It is uncomfortable to save more and retrench. Diversification is uncomfortable when an investor’s home equity market is on a hot streak. Many factor strategies produce returns in unconventional ways, which can catch inexperienced investors off guard.

If investors want successful financial outcomes in coming decades, they need to get comfortable with being uncomfortable.

Adam Butler is co-Founder and Chief Investment Officer at ReSolve Asset Management. ReSolve specializes in diversified ETF-based active asset allocation strategies, including Adaptive Asset Allocation, Risk Parity, and Tactical Equity. Learn more at investresolve.com.

[1] Elroy Dimson, Paul Marsh and Mike Staunton, Credit Suisse Global Investment Returns Sourcebook 2016

Read more articles by Adam Butler