In part I of this two-part report on tools that help you meet the requirements of the DOL fiduciary rule, I acknowledged that there is a high likelihood that the rule will eventually be diminished or repealed by the incoming Republican leadership in the White House, House and Senate.

But I also wondered whether this can be accomplished in less than two months, given that the rule may not be at the top of the legislative priority list. It’s probable that advisory firms will need to acknowledge their fiduciary status, justify that their rollover recommendations from 401(k) plans to IRAs were made with the client’s best interests in mind and otherwise meet the standards of the full rule for part of the year. After that, the best practice may be to continue complying – or, at least, have a way to show clients that your rollover recommendation really is superior to where they are now.

The first part of the report looked at the new cottage industry of DOL fiduciary compliance tools, which variously proscribed your business process for getting into compliance, comparing fees in the 401(k) portfolio with your fees and the industry standard, comparing the quality of the investments in the current and proposed portfolio, demonstrating that you’re monitoring the quality of those investments, assessing the riskiness of one portfolio versus the other and determining what trades need to be made when dialing down the riskiness to the client’s risk tolerance.

Here in part II, let’s look at a couple of new tools that give you an integrated solution to DOL fiduciary compliance. Are you recommending a superior asset allocation? Are you recommending better investments in the IRA than the client previously owned? Is the IRA’s all-in cost lower than the plan sponsor’s offering, and if not, are you offering more services than the plan sponsor was offering?

RiXtrema: Costs, performance and risk comparisons

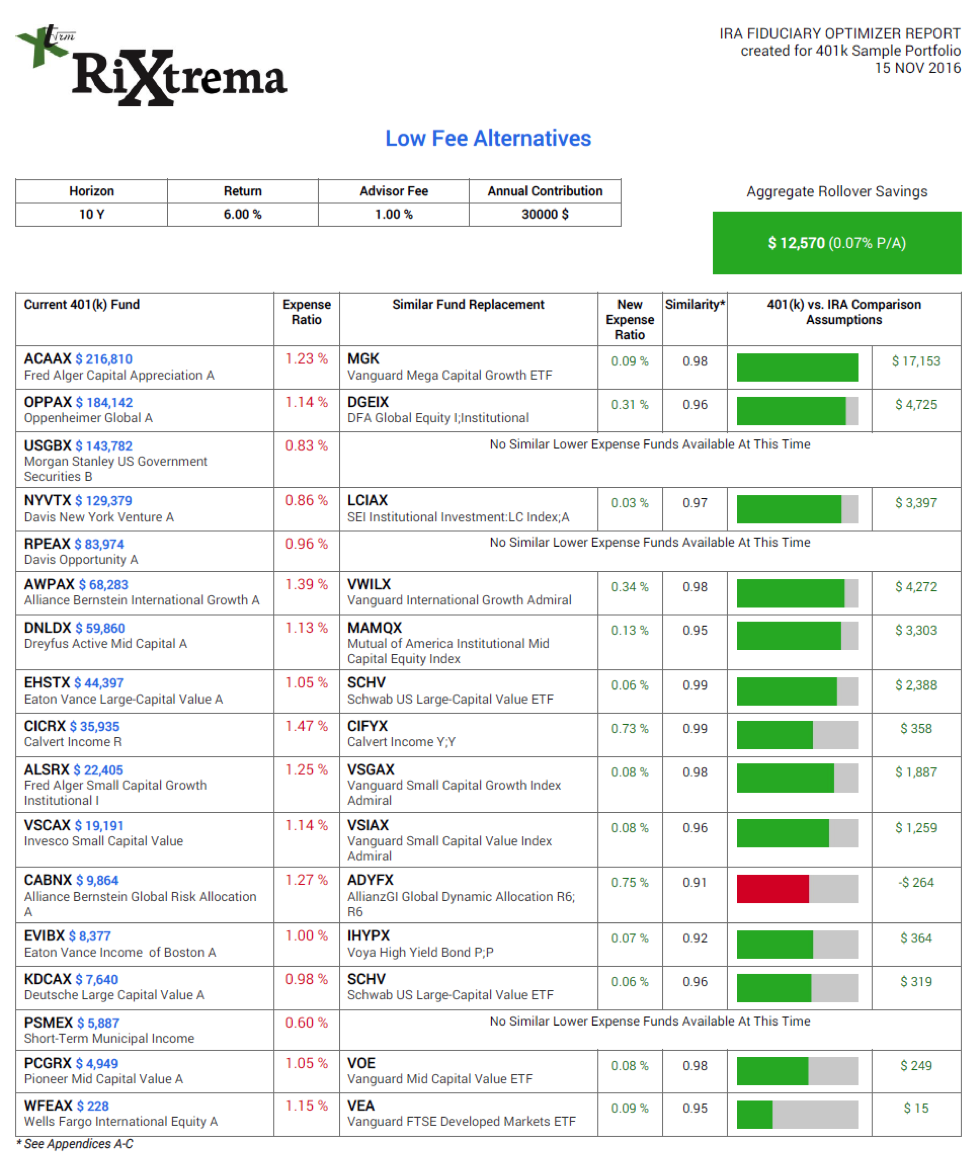

Arguably the most comprehensive DOL rule solution available to advisors is the IRA Fiduciary Optimizer, offered by RiXtrema. Company president Daniel Satchkov thinks that there is a lot of ways for planners and advisors to add value by replacing the plans their clients are currently invested in. “According to our estimates,” he says, “401(k) plans, in aggregate, probably waste over $12 billion a year of retirees’ money.” You can find the numbers in a white paper on the RiXtrema website.

The IRA Fiduciary Optimizer is an extension of one of RiXtrema’s legacy programs, called the 401(k) Fiduciary Optimizer, used by advisors who are managing qualified assets. Among other things, the tool pulls data from the 5500 forms that qualified plans file with the Department of Labor, and looks at the underlying funds.

“You would be surprised at the data we’ve been collecting,” Satchkov says. “It’s not unusual to find plans that gouge people. I was looking at a $21 million plan this morning that didn’t bother to negotiate institutional share classes.” Pulling a plan up at random from the RiXtrema database, Satchkov finds that one of its investment options is an “A” share class from a large fund company, with an annual expense ratio of 128 basis points. “This is broad daylight robbery going on,” he mutters, considering that a lower cost, institutional share class is available for the same fund.

What to do? Pulling this and other data from the tool’s database, an advisor using the IRA Fiduciary Optimizer can assess the expense ratio of the funds the client is invested in currently within the 401(k) plan. Then it will search for superior funds – either from the advisory firm’s buy list or the entire universe of open-end mutual funds and ETFs – that have a high correlation to those existing funds.

Running the system produces several possible alternatives to the aforementioned A share fund, each with a correlation of .97 or better – a number that is not only based on the monthly behavior of the funds that are being compared, but also on the similarity of their underlying holdings, pulled from the SEC’s Edgar database using another data-collecting algorithm.

“Basically, this tells you that these funds are behaving very much like the fund they would be replacing,” says Satchkov. “In this case, I would propose to replace the position with a similar Vanguard fund, which would get almost exactly the same exposure – except that at 8 basis points a year, it is 15 times less expensive.”

After going through the process of replacing each of the fund positions the client is holding in the 401(k) plan, you can do a comparison of the costs in the 401(k) plan vs. the IRA portfolio that you’re recommending as a replacement. Most advisors will obtain the summary plan costs from statements the client provides, but if that isn’t forthcoming, RiXtrema provides access to the Larkspur Data database of 401(k) plan expenses. “Their database has 1.3 million plans in it, so the client’s plan may be included,” says Satchkov.

The system adds in the plan expenses and accounts for the fees that the advisor proposes to charge for managing the IRA. Once all the costs are on the table, the Fiduciary Optimizer tool automatically calculates – and shows in a report – that the client would reduce total all-in investment expenses from $187,000 to $60,000 a year.

The report also tracks the historical performance of each fund that has been replaced against that of the fund that the advisor is proposing, and in this particular demonstration, the difference between the lines on the graph is striking. “The lineup I am offering is not only less expensive,” says Satchkov; “it is much better performing in any type of environment that we look back at.”

But is it the best policy to replace every fund, dollar for dollar, without getting a better idea of whether the 401(k) portfolio is appropriate for the client’s risk tolerance?

RiXtrema’s IRA Fiduciary Optimizer lets you input the client’s FinaMetrica risk-tolerance score, and then it compares that score with the riskiness of the client’s 401(k) allocation. “In this case, the 401(k) portfolio had a risk score of 70,” says Satchkov. “But the FinaMetrica questionnaire says that this person has a risk-tolerance metric of 44. So we should probably replace the plan allocations with a less volatile portfolio.”

A separate working environment allows advisors to reallocate the fund weightings they propose to use in the rollover IRA, by trial and error, to quickly reach a risk score that matches the client’s risk tolerance number.

The Fiduciary Optimizer also invites you to input the services you plan to provide to the rollover client, side-by-side with the services the client is receiving currently from the plan sponsor.

At the end of the process, RiXtrema’s platform will produce a report that summarizes all the different ways to compare the 401(k) plan to the proposed IRA rollover: the differences in costs, expected performance, allocation and services that the advisor will provide. It also notes whether the 401(k) plan and the advisor are using institutional share classes. (A sample cost page is included here for reference purposes.)

All of this lets you make the case that the client would be better off rolling money into the IRA that you’re managing. But you still have to act as a fiduciary, which means, among other things, charging reasonable fees.

For individual advisory practices, this isn’t a huge issue. But when a broker-dealer has hundreds or thousands of reps using its investment platform, the compliance staff will find it helpful to compare what the reps are charging to manage IRA portfolios against a national best-practice fee structure.

To make this possible, RiXtrema has created an algorithm that compares the AUM fees charged to fees charged by the 17,500 independent RIA firms who provide fee disclosures on the SEC’s ADV Part II. “We built code that will look at the fees and compensation section, and using some pretty sophisticated technology, we are extracting the fee schedules,” says Satchkov. “They all look different, have different wording and a different structure,” he admits. “But we can weed out the mutual funds by looking at the responses in various check-boxes, and then we can parse the data so that we can calculate the average [retail advisory] fees for a portfolio of $0 to $500,000, or $1 million to $1.5 million and so forth.”

So, for example, a compliance officer can look through the RiXtrema platform and sort the various fees that different reps are charging. At the top, he notices that one advisory team is charging 1.26% for a $1 million portfolio, when the industry average is 1.02%. “Is that a red flag?” Satchkov asks. “If I saw that, I would want to know what additional services that office was providing to its clients.”

Cost? For one advisor, the IRA Fiduciary Optimizer costs $300 a month, with the per-user costs scaled down for larger firms with multiple planning practitioners.

PCS: A recordkeeper’s alternative

The other comprehensive tool addressing the DOL fiduciary rule comes straight from the ERISA space itself. Professional Capital Services (PCS) is a record-keeper in the 401(k) marketplace, currently serving advisors with an aggregate $4.5 billion in qualified plan assets across 150,000 participants. The firm also trains independent fiduciary financial planners to manage company 401(k) plans through its Advisor Lab subsidiary, and since so many of those advisors were handling IRA rollovers, the company started Advisor Trust in 2008 – a trust company that serves as a low-cost IRA record-keeper.

“We act as an administrative fiduciary and offer consolidated reporting,” explains company founder Mark Klein, who describes himself as “a recovering ERISA attorney.” On the 401(k) side, the firm offers administrative services and either serves as a record-keeper or works alongside a third-party administrator (TPA) that the advisor selects.

Last year, as the DOL rule was finalized, Klein began fielding requests for a tool that would help advisors benchmark their fees for managing an IRA to the fees that clients were paying in company 401(k) plans. They also wanted a software solution that would make it easy to compare the transfer of another advisor’s commission-based IRA to their own fee-compensated fiduciary IRA management.

PCS was already taking a feed from the Department of Labor with the data from annual 5500 filings from qualified plans, and had developed algorithms to extract cost and other information. So, to meet the DOL demand, it added several new features to its AdvisorPlan software, the advisor-facing tool that accesses PCS’ databases.

Such as? The comparison starts with the fees the client is currently paying, either in the 401(k) portfolio or a commission-based investment in an IRA. This information might come from the data feed or an account aggregation system that would pull in recent transaction data from the client’s online account. “We support a lot of turnkey asset managers, so we’re familiar with how to evaluate these models through our platform,” says Klein. The client’s plan document also lists the services that the client is currently receiving from a 401(k) provider.

The system integrates with Morningstar’s database, which provides the yearly expense ratio for the client’s holdings (including variable annuities) and, for comparison purposes, it generates the expense ratios for the funds in your proposed IRA portfolio. You input your advisory fees and the services you plan to provide to the client.

AdvisorPlan generates a document which includes the DOL-required legal language that commits you to act as a fiduciary, and offers a side-by-side comparison of the various annual fees the client is currently paying in the 401(k) portfolio or commission-based IRA versus the proposed IRA. There’s a side-by-side comparison of the services and portfolio performance. The document is client-facing, and often the client will sign it. But the system also automatically saves the documents in a master compliance file.

Cost? The AdvisorPlan software, including the DOL fiduciary compliance add-on, is free for advisors who use Advisor Trust as the trust company for the rollover IRAs. The company is currently deciding whether to offer it as a standalone product for advisors who custody elsewhere.

Gaining a competitive edge through technology

When you look at the new software capabilities that are coming online, driven by the DOL rule, it’s easy to see a rapid professional evolution toward a more fiduciary mindset. Commission-compensated RIAs have new tools that automate the conversion of annuities or commission-implemented IRAs to an AUM-based revenue model. Fiduciary advisors have better ways to document their decision processes, and the benefits of moving client assets under their management.

As the tools take hold, more clients will be exposed to compliance with the fiduciary rule, and become accustomed to having their entire financial situation treated as if it was qualified money. Whether or not the DOL rule survives in its present form, the standards it has set appear to be here to stay. And, thanks to the cottage industry of new compliance tools, it is also easier to comply with than people might have believed last April, when the rule was finalized and announced.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com. Or check out his Insider's Forum Conference (for 2016 in San Diego) at www.insidersforum.com.

Read more articles by Bob Veres