A Prediction for the Future of Active Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat effect will the index fund revolution and the Department of Labor’s (DOL) fiduciary rule have on active managers? The data shows that active management is still a healthy business model. But industry consolidation is coming and advisors will need to change the way they construct portfolios.

Indexing is a very low-fee business, with the standard-setting fund Vanguard Index 500 Admiral Class (VFIAX) charging a tiny 0.05% of the investor’s asset balance per year. Active managers typically charge a fee some 20 times higher, around 1% per year, although fees for some popular actively managed funds have come down; the popular fund Fidelity Contrafund (FCNKX) has a net expense ratio of 0.70%.[1]

And the two types of funds are in direct competition with one another.[2] A visitor from Mars would guess that, unless high-fee active funds can provide a consistent and predictable return that exceeds the comparable index-fund return by more than the fee difference, active managers will lose most of their market share. Indeed, that visitor would wonder how active managers were able to garner as large a proportion of assets as they currently have.

Yet active managers have thrived, despite not only failing, on average, to beat comparable index funds by at least the fee difference, but also underperforming the index in an absolute sense. (In every period there are, of course, some excellent active managers, but it’s incredibly hard for investors to distinguish the winners from the losers in advance.) And index funds have been available to institutions for 45 years and to individuals for 40 years; if index funds were the better investment after fees are considered, they have had plenty of time to displace active managers.

They have not done so.

Recent trends, however, show that – finally – indexing is taking a real bite out of active manager market shares and profits. Reinforcing this trend is the recent DOL “fiduciary rule,” which makes advisors into fiduciaries who have to act in the sole interest of the client.[3] Most experts interpret the rule as saying that, if an advisor recommends an active manager, she must perform due diligence to conclude that the manager’s expected extra return, beyond that of the benchmark or index-fund alternative, is at least equal to the extra fee. This is a very difficult standard that could inhibit clients’ hiring of active managers.

So, should we expect the movement of assets from active to passive management to continue? How far will it go? How much will it affect the profits of the active management industry? Finally, will a shortage of active managers cause markets to become more inefficient, creating problems for indexers and opportunity for active managers, so that the trend will someday reverse?[4]

Recent trends in active versus passive management

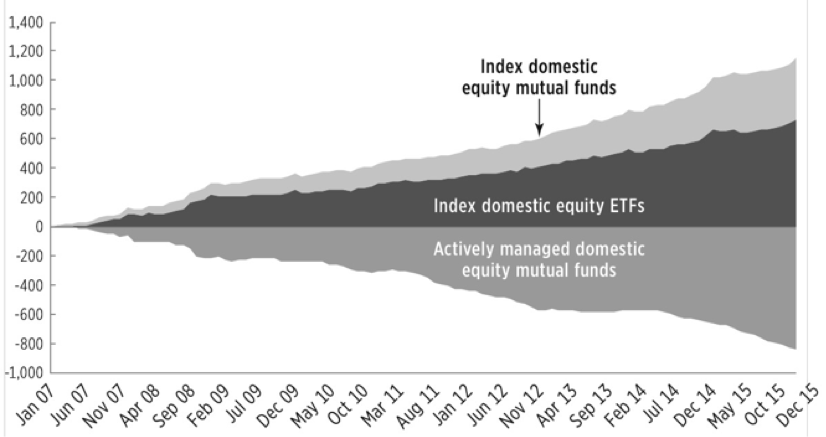

Exhibit 1 shows net fund flows into or out of each major type of pooled equity investment: index mutual funds, index ETFs, and active managers. Both types of index funds – conventional index mutual funds and ETFs, which are also a type of mutual fund – have gained tremendously at the expense of active managers. To provide a sense of scale, note that the mutual funds with a U.S. equity-only investment objective have assets of about $6 trillion.[5] The exhibit shows that index funds and index ETFs received about $1.2 trillion in new money over the nine-year period.

Exhibit 1

U.S. equity mutual fund flows, by fund type, 2007-2015

![]()

Source: Investment Company Institute, ICI 2016 Factbook, figure 2.14.

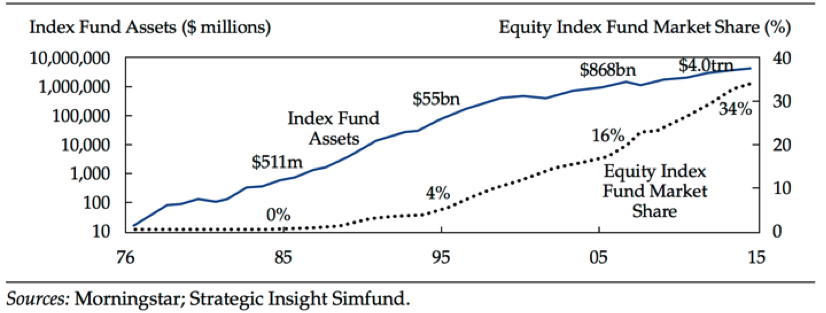

Before the most recent decade, index funds grew at a rate that was large relative to their own size, but represented only a trickle when compared to active managers. Only in the mid-1990s did the trickle become a flood. Exhibit 2 shows the growth of indexed assets, including institutional index funds (which are sometimes not reported as part of mutual fund totals), over the period since Jack Bogle launched the first retail index fund at Vanguard in 1976. Equity index fund assets are shown in log scale on the left axis, and equity index funds as a percentage of all equity funds are shown in arithmetic (conventional) scale on the right axis.

Exhibit 2

Growth of Index Fund AUM and Market Share, 1976-2015

Reproduced from Bogle, John C., “The Index Mutual Fund: 40 Years of Growth, Change, and Challenge,” Financial Analysts Journal, January/February 2016, p. 10.

How much indexing is too much?

As the move toward indexing accelerated, some commentators began to wonder whether there eventually would be a shortage of active managers. Finance theory says that while, by indexing, any given investor can piggyback on the price discovery provided by active managers, someone has to analyze and set the prices of securities or else markets will be wildly inefficient. In other words, there must be active managers in the system to support indexed investors.

If there is too much indexing, this argument goes, we’ll know it because active management will have become easy and lucrative. Large arbitrage profits will draw active managers and active management money out of the woodwork and the trend toward indexing will stop. That is, the index/active balance is self-correcting and finds an equilibrium with a large proportion, but not all, of equity assets indexed.

Yet we must remind ourselves of William Sharpe’s powerful observation that active management is, always and everywhere, a zero-sum game gross of fees (if the community of active managers is defined broadly to include all non-indexers, including, for example, individuals managing their own portfolios). Thus active management will never be easy in the sense of active managers outperforming as a group. An oversized commitment to indexing might cause it to become easier for some active managers to outperform, but they will still have to do so at the expense of other active managers – there being nobody else to trade with!

Revenues and profits of leading asset management firms over the last decade

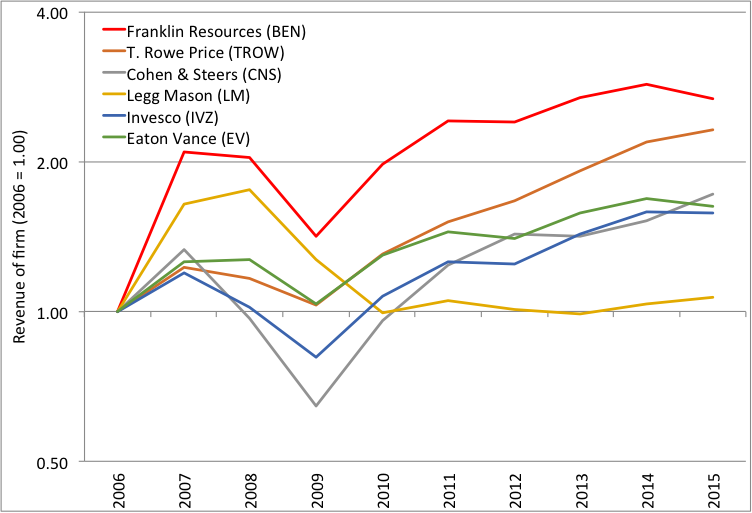

To get “under the hood” of the asset management industry, I looked at income statements of six publicly traded companies whose primary business is managing mutual funds. Exhibit 3 shows the growth or decline of revenues (top-line sales) for these companies, normalized to 2006 = $1.00.

Exhibit 3

Revenues of six publicly traded asset management firms, 2006-2015

Source: Constructed by the author using data from publicly available financial statements

This does not look like an industry in decline! The great crash of 2008 caused revenues of all the firms to decline sharply, but only Legg Mason failed to recover and move to new highs – even then, its 2015 revenue exceeded its 2006 revenue.[6] Franklin Resources (which owns Templeton) and T. Rowe Price more than doubled their revenues over the decade despite the crash. Note that the S&P 500 was up 59% over the period; so while market appreciation accounted for most of the middle three firms’ revenue growth, it did not account for the growth of the top two.

Profits are more important to investors than total revenue. Exhibit 4 shows profits (earnings) of the six firms, normalized to 2006 = 1.00 except for Cohen & Steers, which is normalized to 2007 = 1.00 because that company had essentially no profits in 2006. Negative numbers represent losses.

Exhibit 4

Profits of six publicly traded asset management firms, 2006-2015

Source: Constructed by the author using data from publicly available financial statements.

Again, is this an industry in decline? Profit growth at the top two firms (which are the same firms as the top two by revenue growth) was faster than the capital appreciation of the market; the middle firms’ profits grew at market rates; and the bottom two lagged. If there is industry-wide revenue or profit compression due to competition from index funds, I don’t see it in these graphs.

Yet the market folklore, and the views of analysts, challenge that conclusion. Perhaps the big declines in active management revenue and profitability are in the future, with competition from index funds and ETFs having only just begun to affect the bottom (and top) line. Let’s ask some equity analysts what they are seeing.

Analysts’ views of active management firms

Analysts are, of course, supposed to look to the future, not just study past trends. I interviewed Tim Clift of Envestnet and Greggory Warren of Morningstar. Envestnet is a premier turnkey asset management program (TAMP) provider to advisors. Morningstar is a leading financial information company, providing not only the familiar mutual fund star ratings but also individual-stock ratings and data. Both analysts cover publicly traded asset management companies.

Summarizing the last couple decades’ asset management trends, Tim Clift said, “I think the industry [has succeeded in separating] alpha and beta. As a result beta is cheap now, so if you've been a closet indexer in an active shop, you're in trouble.” A closet indexer is an asset manager that selects holdings close to those of the benchmark to minimize the risk of large differences between the portfolio’s return and the benchmark return. A recent Advisor Perspectives article, The 10 Largest Closet-Index Funds, discussed funds in this category.

But Clift does not think that the overall effort to beat the market -that is, to produce alpha - is in trouble. The firms that are best at alpha production will continue to do very well, while others, which may not add much value anyway, will lose market share or even fail.

Gregg Warren located the origin of active managers’ current troubles in the invention of the ETF:

We've been in a secular trend towards index funds for 30 years now. For a long time, the organic growth of index funds was in the 6% to 7% range annually. Once ETFs came out, though, and offered an even lower cost alternative, one that could be traded basically any time during the day and had some tax benefits to it, you saw a ramp up in the growth rate.

The real story has been what ETFs have done to the business. They've offered market performance at incredibly low fees compared to what you can get with active – even lower fees than we can get with some index funds. With that perspective it's becoming a real threat to the business.

Warren was particularly bearish on closet indexers who charge active fees. Specialist active managers who are not viewed as close substitutes for index funds should do better.

I asked Warren whether the DOL fiduciary rule would inhibit advisors from recommending active managers out of a fear of being sued for these managers’ potential underperformance and high fees. He responded:

A Trump administration or Republican-led Congress is likely to water it down, if not rescind it – but that wouldn't change much. You already have broker-dealer and advisor networks shifting their thinking, putting a keener microscope on active manager performance than they’ve done in the past. The broker-dealer networks have started culling the number of funds on their platforms, with poor performers being thrown out.

The broker-dealers and the advisors have the upper hand now, relative to the active-management firms, and that is detrimental for fees and for the profitability of the active managers going forward.

In my conversation with Warren, I wondered aloud whether active managers should just sit there and lose market share, given the challenge of fending off a new, radically low-priced competitor who delivers a product that, on average, is just as good or possibly better. Warren replied,

That's been the initial thought. They were cognizant of ETFs growing and they saw the markets changing, but the change wasn't hitting their bottom lines yet, given that we've been in a bull market for eight years now. Even after losing assets to outflows, active managers have still been hitting record levels of assets-under-management (AUM) in some firms and products.

But now they're all stepping back and looking at the business. You’re already starting to see asset managers cutting fees. Again, this is due to negotiations with broker-dealers and advisory networks, which keep up the pressure to both generate superior performance and reduce fees. This means giving up some profitability, but the industry can probably afford that, given that it is running 32 to 33 percent operating margins.

Envestnet’s Clift noted that there’s another trend affecting active managers:

[The trend is] away from single products and toward multi-asset solutions. The days of a wholesaler walking in and pitching an individual fund are gone. Fund providers really have to promote whole investment strategies, multi-asset solutions, and that's a major shift from the way business has been done in the past.

Thus, large fund companies with multiple products, and with asset allocation capabilities and the resources to implement multi-asset, one-stop solutions for individual investors, will have a competitive advantage. Truly superior single-product providers will too.

Active managers of no particular distinction will fade away.

The trend toward indexing and away from traditional active management has been widely discussed and studied. A helpful resource for further reading is McKinsey Global Institute’s lengthy report “Thriving in the New Abnormal.”[7]

Technology and asset management

In the search for alpha, many asset managers – cognizant that all alpha is earned at the expense of other alpha-seekers – are looking to technology to gain an edge in the marketplace. Much of this new focus on technology involves the creative use of “big data,” but there are many other emerging uses of technology in investment management, broadly grouped together as “fintech.”

Can manager selectors and their clients turn these new technologies to their advantage? Unfortunately, it’s not clear that they can. We do not know yet whether the use of “big data” conveys an advantage so selecting managers by relying on those who say they are making progress on that front is an uncertain bet.

Moreover, technology – of any kind – has virtually no chance of picking good managers in advance. A whole industry of pension consultants, data providers, bank custodians and others have tried for at least 30 years to turn manager selection into a science. Mostly, they’ve found that it cannot be done. If you could do it, the method would fail because everybody would pick the same managers, forcing them to buy the whole capitalization of the market and diluting the alpha until it reached zero (or worse).

Manager selection is an art, based on personal judgment of the manager’s ability to have an edge over other managers. A 55%-60% success record is outstanding and all that can be reasonably hoped for.

Conclusion

The days of allocating to actively managed funds just because they are active are over. We all know that, on average, active managers will be beaten by the market after costs. Best practices for individual investors and their advisors in the future will be more like best practices for institutional investors in the last 20 years: the base case is an index fund, with active managers used when they present convincing evidence, both historically and in the process they intend to use in the future, that they have a good chance of beating the relevant benchmark after costs.

I emphasize “a good chance” because there cannot ever be a guarantee of active management beating its benchmark. As a result, advisors face some risk in recommending active managers – fees are higher and the manager could underperform. Still, there is little evidence that the DOL fiduciary rule will eradicate active management in principle; it will just make it easier to recommend index-based strategies and harder to justify recommending active funds. For a given investor, index funds and ETFs will represent the majority of allocations and carefully selected active managers, expected to deliver return patterns significantly different from the benchmark, will represent a minority.

While index funds and ETFs have had a huge run, active management companies are still prospering. However, if current trends continue (and there is every reason to expect them to), they will prosper less in the future. Active managers will have a significantly smaller share of a business that is growing only gradually – and there will be relentless pressure on fees.

Moreover, active managers’ expenses will continue to be high. Even with some firms letting analysts go, the best analysts (the only ones worth having) will still command high salaries, and sales and marketing budgets, currently stagnant, will need to be bolstered. As a result, active asset management firms as an investment category can be expected to struggle. The best alpha producers will do well, but others will shrink in scale and importance; many will close. A half-century after Eugene Fama promulgated the Efficient Market Hypothesis, the market is finally becoming more efficient.

Larry Siegel is the Gary P. Brinson Director of Research for the CFA Research Foundation. Prior to that, he was director of research in the investment division of the Ford Foundation. He is a member of the editorial boards of The Journal of Portfolio Management and The Journal of Investing and serves on the board of directors and program committee of the Q Group. He may be reached at [email protected].

Anna Sachar assisted in the research for this article.

[1] As reported by http://www.FinancialEngines.com on December 12, 2016 (under “Actual Fees,” per annual report).

[2] There is a third type of fund, “smart beta” or factor-based index funds that hold something other than the cap-weighted market portfolio. For the current purpose we’ll classify these as active managers, despite their low fees, because they have to earn their alpha at the expense of other active investors; if they earn more than the (cap-weighted) market return, someone on the other side of whatever bet they’re making will earn less than the market return.

[3] The fiduciary rule applies to 401(k) plan assets, IRAs, and certain other qualified retirement accounts. It does not apply to other (“taxable”) investments.

[4] Here I focus on equities and on the United States. That is where the data are and, to some extent, where the money from active management fees is. While active management and index funds are both very important – and indexing is growing – in non-U.S. markets, it’s hard to get reliable information in those markets, hence our domestic emphasis.

[5] The $6 trillion figure for U.S. equity-focused mutual funds is from the Investment Company Institute 2016 Factbook, table 3 on page 174, and does not include multi-asset-class funds.

Net flows into equity mutual funds, that is, index funds’ and ETF’s gain in excess of active managers’ loss, are accounted for by new savings and by re-allocation from other asset classes into equities, minus redemptions for the purpose of spending and for re-allocation from equities into other asset classes.

[6] This may be due in large part to its reliance on Bill Miller, whose stellar track record began to erode in 2006.

[7] You can request the report here: http://www.mckinsey.com/industries/financial-services/our-insights/thriving-in-the-new-abnormal-north-american-asset-management. Note that McKinsey requires a work e-mail or student e-mail address; a generic “gmail” or similar e-mail address will not suffice.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All