Jeffrey Gundlach predicts trouble for the equity, corporate and junk-bond markets if the yield on the 10-year Treasury bond goes above 3% in 2017. Even the housing market would suffer.

Jeffrey Gundlach predicts trouble for the equity, corporate and junk-bond markets if the yield on the 10-year Treasury bond goes above 3% in 2017. Even the housing market would suffer.

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital, a leading provider of fixed-income mutual funds and ETFs. He spoke to investors via a conference call on December 13. Slides from that presentation are available here. The focus of his talk was DoubleLine’s flagship Total Return Bond Fund (DBLTX).

Corporate bonds, as measured by the ETF LQD, have done poorly since the market bottom on July 8, returning -5.4%, but the junk-bond ETF JNK “massively” outperformed, returning 3.6% since that date, Gundlach said. But he said if the 10-year bond, which closed at 2.46% on the day he spoke, goes above 3%, then junk bonds would “fall into a black hole of illiquidity.”

Investment-grade corporate bonds are already “as overvalued as it gets,” he said, and are threatened by excessive leverage in the corporate sectors.

A push above 3% would cause investors to rethink their equity holdings and shift allocations to bonds, he said. Financial services – specifically banks – would suffer because their dividend yields would be significantly less than 3%.

That rate increase would translate to a 30% increase in mortgage payments for homeowners from the July levels, according to Gundlach. This would hurt resales, he said, since there is “no way” the median income would rise by nearly 30%.

Gundlach said that “3% is a really big number on the 10-year. It won’t happen soon, but it may happen in 2017.”

“If you are above 3% on the 10-year, it is no longer possible to make the case that the bull market in bonds is intact,” he said, “at least based on the charts.”

Let’s look at Gundlach’s take on the market implications of the Trump presidency and his other comments.

Why did Trump win?

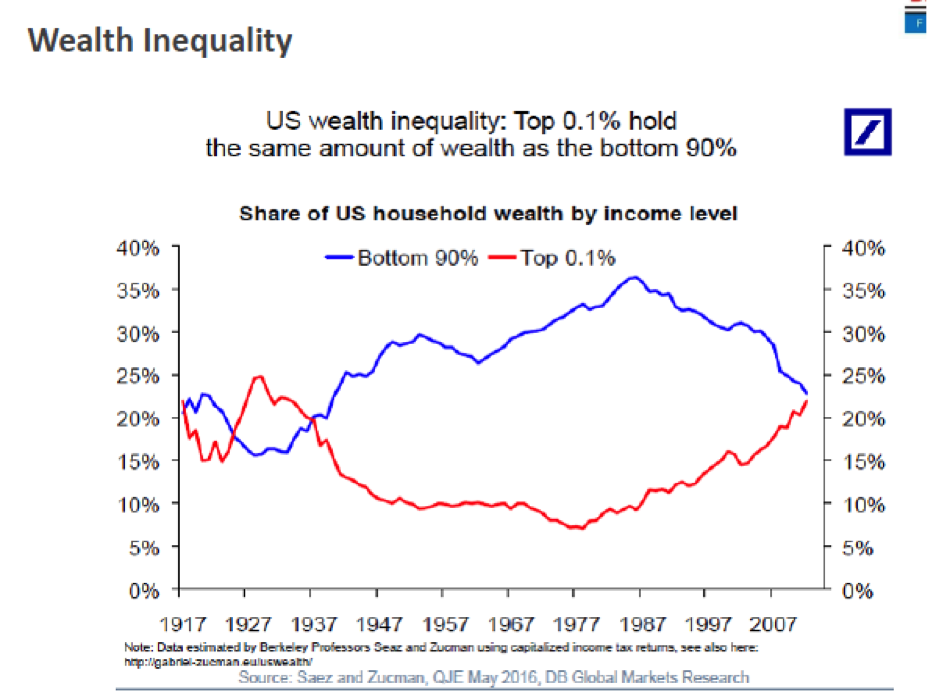

Gundlach, who predicted Trump’s victory starting in January, said that the election results could be summarized in this chart:

Over the last 30 years, the share of wealth for the bottom 90%, by income level, has gone from 35% to 22%, while the share for the top 0.1% went from 5% to the same 22%.

The bottom 90% have as much wealth as the top 0.1%.

Many voters in rural America are looking for Trump to fulfill his promise to “drain the swamp,” Gundlach said. He noted that phrase was originally used by Ronald Reagan, who also coined the slogan “let's make American great again,” and it was Trump who dropped the word “let's” at the beginning.

Gundlach compared the economy that Trump will inherit to what Reagan faced when he took office in 1982. In both cases, GDP growth was slow, but Reagan faced much higher inflation and bond yields. Stock market P/E ratios were in single digits for Reagan, but Trump will take office with a multiple of approximately 20.

Debt-to-GDP was a mere 31% in 1982, versus the 105% that Trump will encounter. “People have fallen asleep on this topic since 2011,” Gundlach said, when government shutdowns were a common topic of conversation. Trump’s policies threaten to push debt levels higher, as he will need to fund his infrastructure initiatives and plans for increased defense spending.

“There is a lot of debt in the economy and it will be hard to get a debt-based boom,” Gundlach said.

Manufacturing jobs are down 27% since NAFTA was signed in 1993, Gundlach said, and he doubts that Trump can bring back those jobs. “A lot of those jobs have been lost to robots,” he said, or will be lost to innovations such as driverless cars.

Trump has said he will attack the trade deficit, but Gundlach was skeptical he would make much progress toward that goal, since China is our biggest trading partner and it is unlikely we can increase exports enough to offset Chinese imports.

Gundlach said that Trump’s plan to decrease the corporate tax rate may have a limited impact on the deficit, since those taxes are only 11% of federal revenues; the bulk of federal tax revenue comes from individuals, he said.

Trump has talked about building a stronger defense, but that too may not have a big effect on GDP growth. Defense spending has been incredibly stable since 1970 on an inflation-adjusted basis, Gundlach said, but only about 3% of GDP, plus or minus 1.5%, has been allocated to defense.

Net interest is an incredibly small part of federal spending, Gundlach said, and hasn’t grown in the past 15 years on an absolute basis. But Gundlach has predicted that 10-year rates would go to 6% in the next four to five years, about the time of the next presidential election, and he said that level of rates “would be a problem.”

If there is a view among voters that Trump is successful, Gundlach said the Senate will “get lopsided” in 2018, since many Democrats are up for reelection in states that Trump won or closely lost.

Trump and the markets

Gundlach said he agrees with Trump that there is a need for infrastructure spending. He predicted that Trump will “give it a try to deficit-spend on infrastructure and defense.” But Gundlach does not give a lot of credence to the idea that the new Congress will oppose this and insist that the increased spending be offset by increased revenues (taxes) or decreased spending in other areas. More aggressive spending is “what Trump campaigned on,” Gundlach said. “That will lead to another leg up on debt, which is not friendly for bonds.”

The market has warmed up to that idea. Gundlach said that 10-year rates have risen from 1.72% to 2.53% since Trump’s victory.

What really matters in the stock market are sectors, Gundlach said. Financials, industrials and energy stocks have all have done well since the election, he said. Healthcare has been a loser, as have consumer staples and utilities, which Gundlach called “a bond proxy.” He showed data illustrating that it is very common for the market to rally after an election and then level off until around inauguration day, when investors realize the president “doesn’t have a magic wand.”

Gundlach predicted an equity sell off around inauguration day. But he added that he doesn’t expect a recession, although one often occurs in the first year of a new president’s term.

The global markets and Fed policy

Conditions in Europe reflect instability and the risk of a fracture in the European Union (EU).

Gundlach cited polls showing that European citizens gave a mixed review on whether they have a favorable view of the EU, although in some countries, such as France, the view is very unfavorable. With elections coming in 2017, Gundlach said he would closely monitor developments in France. He said polls showed a “massive disapproval” of refugee handling, and that was viewed nearly as unfavorably as the EU’s handling of the economy.

Unemployment in Europe has gone from 11% to 8.3% since the start of 2013, but Gundlach noted that is still significantly higher than levels in the U.S.. Sovereign debt yields in Europe are up 60 basis points since July, he said, and spreads have widened from 1.5 to 1.9%. Spreads in Italy are a clear indicator of the likelihood of it leaving the EU, he said, but he did not predict if or when that would happen. Italian bond yields are lower than those in the U.S. and Gundlach said he can’t imagine why anyone would own Italian bonds.

Bond yields are rising globally, he said, and noted that yields in Japan are now positive.

The duration of global bond market has risen from 9 to 13.5 since 2009, he said, which represents significant interest rate risk. Gundlach advised a “continued defense stance” in the bond market, but said, “If you are nimble you can make money on bonds at current levels.”

“Fed policy exists within the context of the fiscal stimulus,” Gundlach said. He said he is 100% certain the Fed will hike rates in December and the question is what the Fed’s narrative will be about its policies given the election results.

Inflation is rising, he said, but it is not driven by food or energy prices. Instead shelter and other “sticky” things are pushing inflation higher. If food and energy prices spike, Gundlach said inflation could be over 3%.

He is not sure past is prologue, but Gundlach said that in prior rate cycles the Fed has tightened until “something broke,” and then there was a “massive reversal.” The question is what level of the Fed funds rate will cause something to break. People are used to very low rates, he said. Don’t think that if rates rise there will be a positive stock market based on an expectation of economic growth, Gundlach warned.

In the past, market expectations of rate increases have been more modest than what Fed governors have indicated. But the Fed has “capitulated,” Gundlach said, and it no longer believes it knows more than the market. The market and the Fed are predicting two rate hikes in 2017, he said. But Gundlach warned that “capitulation usually happens at the wrong time. So don’t count on two rate hikes.”

The overarching question

The big uncertainty for investors is the long-term trend in interest rates. Is the 35-year bull market in bonds over or will the current spike in rates be a temporary phenomenon?

Gundlach did not give a precise answer to that question. A lot depends on if and when the 10-year yield reaches 3%.

But he was clear about the reasons behind the general trend in rates.

Global yields are on the rise because markets have realized a belief that “negative-interest rates are with us forever” has lost out to a recognition that they don’t work, he said.

In regards to negative rates, he said, “You can’t keep doing the thing that doesn’t work. We’re moving on to fiscal stimulus.”

Read more articles by Robert Huebscher

Jeffrey Gundlach predicts trouble for the equity, corporate and junk-bond markets if the yield on the 10-year Treasury bond goes above 3% in 2017. Even the housing market would suffer.

Jeffrey Gundlach predicts trouble for the equity, corporate and junk-bond markets if the yield on the 10-year Treasury bond goes above 3% in 2017. Even the housing market would suffer.