Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Smart beta. Empirical finance. Evidence-based investing. These terms, which were in the periphery of the investment vernacular just 10 years ago, have become the investment world’s most popular memes today. Why?

Investors have been disenfranchised from traditional forms of active management. After all, performance-obsessed investors can’t fail to notice that a majority of active mutual funds in almost every category consistently fail to outperform their passive benchmarks, year after year, over every meaningful investment horizon.

Factor-based investing replaces stock-picking guru

What is factor-based investing? Larry Swedroe and Andrew Berkin offer an incredibly comprehensive answer in their newest book, Your Complete Guide to Factor-Based Investing: The Way Smart Money Invests Today. In nine dense chapters complemented by 10 detailed appendices, Swedroe and Berkin provide a broad and deep overview of the most salient factor literature, replete with over 100 citations from the most respected academics and practitioners in the field.

If a factor you’re considering can’t be found in this book, it isn’t worth considering.

Factor-investing godfather Cliff Asness, a founding partner of the Connecticut-based investment firm AQR, wrote the foreword to the book. Asness defines factor-based investing as “defining and then systematically following a set of rules that produce diversified portfolios.” Consistent with the general tone of the book, Swedroe and Berkin make this concept more concrete. They describe factor-based investing as “in part about the academic community’s search for that secret sauce – specifically, the characteristics of stocks and other securities that both explain performance and provide premiums (above market returns).”

These definitions move us closer to an understanding of what factor-based investing is about, but there is still a great deal of ambiguity. After all, the factor literature extends back over half a century. Dozens of papers have identified hundreds of potential factors. Some prominent practitioners have described factor-based investing as a “zoo,” in reference to myriad exotic factors that appear to have little practical substance.

What factors should I consider, and why?

Perhaps the book’s greatest contribution is the framework the authors propose to evaluate the factors. Each factor is subjected to a rigorous analysis under this framework to determine if it is worthy of investors’ attention. Specifically, all worthy factors must:

- Be persistent over a long period of time and across several market cycles

- Be pervasive across a wide variety of investment universes, geographies and sometimes asset classes

- Be robust to various specifications

- Have intuitive explanations grounded in strong risk and/or behavioral arguments, with reasonable barriers to arbitrage

- Be implementable after accounting for market impacts and transaction costs

Factors that survive this analytical gauntlet (usually with lots of room to spare) are recommended for investor consideration and receive a full treatment in the book’s main chapters. Factors that struggle to overcome one or more criteria are relegated to the book’s abundant Appendices. However, even the less noteworthy factors receive extremely detailed discussion, with balanced views on their pros and cons.

This analytical framework guides the structure for almost every chapter of the book. Each chapter begins with a brief introduction to the seminal research on the factor and proceeds to subject the factor to rigorous scrutiny informed by the analytical framework. The most salient literature on each factor is presented and carefully evaluated with detailed summaries of each paper’s conclusions and discussion of what is implied in terms of the factor’s robustness.

In emails with Swedroe, I discovered that he keeps a library of over 3,000 academic articles. This might seem overwhelming, but the authors have curated their collection with surgical precision to offer the right balance of rigor and brevity. If the authors felt that just 100 articles out of 3,000 were worth mentioning, you can bet that they reviewed and eventually discarded an order of magnitude more.

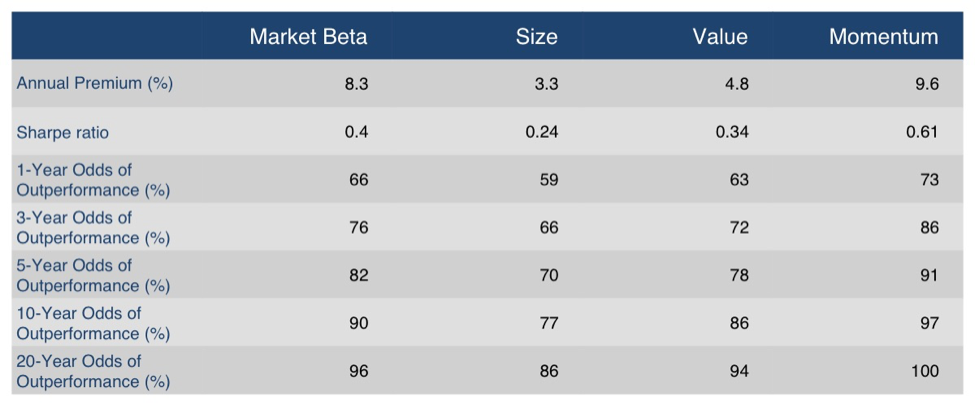

It might have been relatively easy, given the strong analytical significance of many of the factors the authors consider, to present factor returns as somewhat of a “free lunch.” But Swedroe and Berkin successfully avoid this trap. Rather, they spend a great deal of time describing why factor-based investing can be very challenging. One great feature of the book is that each chapter contains a table describing the percentage of periods when each factor produces positive excess returns (i.e. above Treasury-bills) over 1-, 3-, 5-, 10- and 20-year periods. The following table is taken from Chapter 4: Momentum and quantifies the percentage of historical periods with positive premiums for the Market, Size, Value and Momentum factors applied to U.S. stocks from 1927 to 2015.

Figure 1. Persistence of Market Beta, Size, Value and Momentum Risk Premiums, 1927-2015

Source: Larry Swedroe and Andrew Berkin, Your Complete Guide to Factor-Based Investing (Buckingham 2016)

Aside from the fact that factor-based investing can produce negative premiums for years on end, there are other reasons why these methods are challenging for investors to maintain over time. The authors devote an entire Appendix to the most potent challenge: tracking-error regret. Investors who diversify their portfolio into factor-based strategies must realize that they are pursuing a different approach in pursuit of better long-term results. But diversification also has a cost; that is, the pain of missing out when a more traditional investment approach is producing dominant performance.

The authors describe how three behaviors cause investors to fall victim to tracking-error regret: relativism, recency bias and impatience. Relativism is the tendency for investors to compare how their portfolios are performing to some index that has little relevance to the investor’s financial goals. Recency bias occurs when investors focus myopically on how their portfolios have performed in the recent past, while giving little thought to the long-term character of their chosen approach. Many investors become impatient when their unconventional approach fails to produce excess returns for three or even five years. But as Figure 1 illustrates, even stock market beta has underperformed cash for as long as ten years at least 10% of the time.

The peril of a short-term view

Of course, the weakness of empirical finance, which applies to factor-based investing as well, is that all of the research is backward looking. That prompts the question, “Now that these factors are well-known, will arbitrage capital flow into factor-based portfolios and eliminate the associated premiums?” The authors draw primarily on two recent papers (Caluzzo, Moneta, Topaloglu and McLean and Pontiff) to answer this question for U.S.-based factors and draw two conclusions. Factor-based return predictability persists after publication and remains statistically significant. Second, institutional arbitrage capital does flow toward portfolios consistent with published anomalies, and these flows have reduced factor returns by about 32% on average across many factors.

However, the authors note that while studies show some post-publication decay for U.S.-based factor portfolios, investigations of factor persistence in international markets yielded contrasting results. Specifically, a 2016 paper by Heiko Jacobs and Sebastian Muller titled “Anomalies Across the Globe: Once Public, No Longer Existent?” studied pre- and post-publication return predictability for factor portfolios across 39 stock markets accounting for almost 60% of global market capitalization and more than 70% of global GDP for the period 1981 to 2013. Jacobs and Muller’s analysis confirmed a small decline in factor premiums in U.S. markets, but also found that none of the 38 international markets yielded a significant post-publication decline in anomaly returns. Rather, they found that returns to factors in international markets had actually increased.

Swedroe and Berkin go on to examine the pre- and post-publication performance of the factors they endorsed and find that premiums have indeed declined post publication. However, in every case the post-publication factor returns remained positive and statistically significant. The authors then make a strong case for why investors should expect factor premiums to continue to persist in the future. Arguments include the fact that many institutional investors, who provide the bulk of global arbitrage capital, are prohibited from taking short positions. Other arguments include an aversion to short positions in general because of the potential for unlimited losses and limits on leverage. Arbitrage requires that investors can capitalize on pricing inefficiencies in both directions, but short constraints prevent this. These structural barriers to arbitrage should allow mispricings to persist and contribute to future factor-based investing returns.

As practitioners themselves, Swedroe and Berkin would not deem the project complete until they offered concrete guidance on how factor-based investing can be used to improve the risk/return balance of investor portfolios. The authors find that their preferred factors have a low correlation with one another and with stocks in general. For example, value and momentum factors exhibit a substantially negative correlation with market beta, and with each other, over the past half-century. As a result, due to the power of diversification among uncorrelated return streams, an equally weighted portfolio of factor exposures produces over twice as much return per unit of risk as an investment in U.S. market beta alone.

If I had to quibble with the book, it would be with the authors’ choice to exclude time-series momentum from their list of preferred factors. For those new to the factor literature, cross-sectional momentum refers to a process of sorting securities on the basis of how they have performed relative to other securities. Top performing securities over the recent past have higher expected returns over the next few weeks than poorly performing securities. In contrast, time-series momentum – sometimes referred to as “absolute momentum” or “trend-following” – sorts securities on the basis of their own past returns. Securities with positive performance over the recent past have higher expected returns over the next few weeks than securities with negative returns.

The authors’ treatment of the time-series momentum factor in Appendix F makes it clear that it survives every test of robustness with flying colors. Specifically, the authors cite a study by D’Souza, Srichanachaichok, Wang and Yao entitled “The Enduring Effect of Time-Series Momentum on Stock Returns over Nearly 100-Years,” which found that time-series momentum may actually subsume cross-sectional momentum for individual stocks. In addition, time-series momentum is effective for stocks across all sub-periods, while the same cannot be said for cross-sectional momentum. Moreover, the t-stats for time-series momentum appear to be about twice as large as those for cross-sectional momentum.

I asked Swedroe about why they chose to move the chapter on time-series momentum to the Appendix given its highly robust character. He replied that they had debated about where to put the chapter and finally decided to keep it in the Appendix to avoid confusion with the more commonly cited cross-sectional momentum factor. In any event, the authors clearly concluded that time-series momentum is very effective, and that most investors should consider an allocation to it (via Managed Futures) for some portion of their accounts.

Notwithstanding this very minor quibble, I have no reservations about recommending Your Complete Guide to Factor-Based Investing to any investor at virtually any level of experience. Swedroe and Berkin explain fairly nuanced concepts in approachable ways and regularly allude to some of the investing theatre’s most recognized characters in order to make a point. The opening discussion about how Warren Buffett is a “closet factor investor” is a special revelation. At the same time, with over 100 citations, the book represents a surgically curated and brilliantly distilled survey of the most important articles in the factor literature, which should appeal to even the most experienced factor enthusiasts.

If the time of factor-based investing has come, then this is the ultimate guidebook for success.

Adam Bulter is CEO of ReSolve Asset Management, an asset management firm specializing in global ETF managed portfolio solutions and multi-asset factor investing. Visit investresolve.com.

Read more articles by Adam Butler