Until now, much of the growth in environmental, social and governance (ESG) investing has been concentrated among large institutional investors. But the number of financial advisors considering ESG investment products is starting to grow — whether because of idealistic convictions, updated investment guidelines or risk-reduction objectives.

The merits of ESG investing have been trumpeted for years. So why have asset flows to date lagged across retail and advisor channels? We believe that a disjointed array of investment approaches and weak risk-adjusted performance versus non-ESG alternatives has inhibited uptake. However, we also believe that the mainstream investor marketplace is eager for ESG products that combine an integrated approach to ESG best practices with enhanced risk-adjusted returns.

TO DATE, DISPARATE APPROACHES, LIMITED APPLICATION

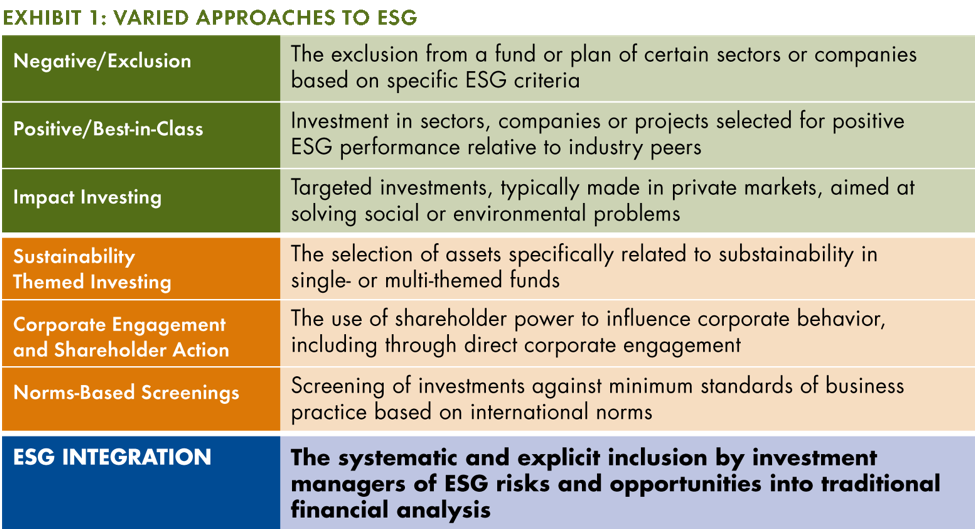

Seven distinct approaches to ESG investing have emerged over time (see Exhibit 1). These approaches did not evolve in linear sequence but, rather, sprang from a mix of top-down (e.g., boards of directors embracing ESG principles) and bottom-up drivers (e.g., investors demanding ESG accountability from public corporations).

Implementation varies from approach to approach, but the resulting approaches typically feature poor diversification and skewed returns that have been difficult to use in standard asset allocation models.

For example:

-

A negative exclusion approach may remove certain industries/sectors from investment consideration but cause increased tracking error versus market weighted benchmarks.

-

A sustainability-themed investment may concentrate risk in certain sectors.

-

Impact-type investors argue that the most effective way to get companies to address social or environmental problems is to become an “activist” shareholder. Progress is achieved by engaging with management to set goals and regularly disclose progress.

Whatever the approach, if an ESG product is not properly diversified, its application typically is limited.

SPOTTING AN OPPORTUNITY

Large institutional investors dominated the early stages of ESG investing because they possessed the requisite expertise and governance protections of well-resourced investment committees. Typically, they invest through separately managed accounts (SMAs) or overlays exhibiting limited asset diversification. Such account structures are not workable, by contrast, for retail and advisor channels, or for institutions that lack committees of investment experts, due to asset diversification requirements and account size thresholds. Herein lays the market opportunity to create a scalable, performance-driven ESG investment vehicle.

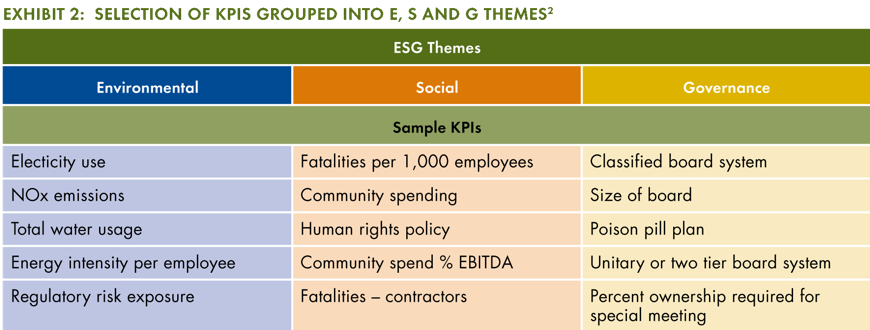

To facilitate product development applications, index providers have started to rely on key performance indicators (KPIs) reported by public companies in their regulatory filings. KPIs are quantitative and qualitative metrics that demonstrate how effectively a company is achieving its business objectives, which often include environmental, social or governance considerations.

For example, a typical KPI for governance reporting is “percent of women on the board of directors.” Most companies disclose some ESG-related KPIs, although scope and transparency varies from firm to firm. KPI metrics are more widely disclosed by large capitalization companies than by mid-cap and small-cap firms. Presently, more than 100 KPIs are reported that can be classified as fulfilling at least one environmental, social or governance theme1.

The development curve for identifying and using KPIs in ESG applications is in its early days. The catalog of ESG-related KPIs is extensive (see Exhibit 2), but not every KPI provides incrementally additive information. Still, it is now possible for asset managers to develop and apply systematic investment strategies that evaluate a company’s risk and opportunities by examining its environmental, social and governance indicators.

Combining this type of information with traditional financial analysis and security selection is a textbook example of ESG integration. This trend has advanced to a point where the information embedded in KPIs is able to be used to better align investors’ ESG goals with shareholder value (as evidenced through stock price appreciation and risk reduction).

It is not surprising that larger capitalization firms are leading the charge to proactively communicate the connection between ESG reporting and financial performance. It is an excellent way to appeal to investors with long-term perspectives. As ESG-related metrics focus and guide management decision-making, a constructive feedback dynamic evolves. Robust interest from investors pushes companies to disclose more, which leads to even greater investor interest and more disclosure. We believe this circular engagement between investors and companies, as they identify, disclose and monitor KPIs, is immensely important when it comes to steering a firm’s management towards constructive ESG behaviors that may also boost its share price.

THE STOXX APPROACH: ANALYZING ESG KPIS FOR RISK AND RETURN

FlexShares gravitated towards a hypothesis that the best way to innovate in the ESG space is to integrate ESG-related KPIs into an investment strategy. A basic way to do this is to identify the materiality of each key performance indicator. Ideally, material KPIs would significantly impact risk/return with strong predictability.

One such example is to focus on indicators that exhibit a substantive or material impact on the (longer-term) sustainability of a firm’s business model along with its share price performance. Analysis illustrated that some KPIs exhibit significant impacts while others present weak or duplicative effects. Likewise, the observed information content of ESG-related metrics across sectors tends to vary. For example, while KPIs for food producers are different from those for steel companies, so too is the utility and degree of information each provides.

For these reasons, research indicates it is prudent to evaluate the impact of KPIs on a sector-by-sector basis3. Incorporating information on companies’ strengths and weaknesses across distinct environmental, social and governance themes makes it possible to quantify a firms’ performance by thematic sub-scores, which can then be rolled up into a composite score. We believe combining the availability of disclosed ESG data with improved portfolio analysis and risk tools suggests it is possible to successfully integrate material, ESG-related KPIs into a diversified, tilted core equity investment methodology.

To explore this, FlexShares engaged STOXX, the globally integrated index provider, to perform a robust analysis of ESG KPIs to see if indicators that lead to long-term value creation for shareholders could be identified. STOXX’s research found indicators in each of the environmental, social and governance buckets that were most influential in determining risk and return. These value-impacting KPIs serve as the backbone of STOXX’s proprietary ESG index methodology.

Specifically, eligible securities are selected from the STOXX Global 1800 Index for prospective inclusion in FlexShares’ U.S. fund (ESG) and global fund (ESGG). Companies that do not adhere to the U.N. Global compact principles, are involved in controversial weapons or are coal miners are excluded from the list of eligible securities. A bottoms-up approach, using publicly available data, is utilized to evaluate 150+ KPIs having broad representation to the three distinct categories of criteria – environmental, social and governance. KPIs may be added or deleted during the annual index reconstitutions. An aggregate ESG score is determined for the eligible participants and the bottom 50% of companies are excluded from the index. The portfolio exposure is tilted in favor of constituents with higher aggregate scores in efforts to optimize risk-adjusted return. Sector, security and country constraints are employed to minimize concentration risk.

We believe measuring the impact of KPIs on security performance provides a holistic and diversified approach to ESG investing. Specifically, KPI integration improves bottoms-up security selection while removing data-provider bias. The methodology builds an ESG index by essentially coding at the “root” level versus applying an overlay or top-down ESG strategy; it parallels the best behaviors of portfolio managers when it comes to evaluating, sorting and selecting companies for investment.

APPLYING ESG KPIs to ETFs

The FlexShares STOXX US ESG Impact Index Fund (ticker: ESG) and FlexShares STOXX Global ESG Impact Index Fund (ticker: ESGG) artfully integrate ESG key performance indicators into their respective core equity investment strategies. We think clients with long-term investment objectives will come to see ESG integration as an opportunity to invest in sustainable companies while reducing portfolio risk and enhancing long-term investment performance.

FOR MORE INFORMATION

If you would like to learn more about our approach to ESG integration and how the FlexShares STOXX ESG Impact funds can help socially responsible investors pursue their investment objectives, call us at 1-855-FlexETF (1-855-353-9383) or visit FlexShares.com.

IMPORTANT INFORMATION

Before investing, carefully consider the FlexShares investment objectives, risks, charges and expenses. This and other information is in the prospectus, a copy of which may be obtained by visiting flexshares.com. Read the prospectus carefully before you invest. Foreside Fund Services, LLC, distributor.

In addition, the Funds are subject to environmental, social and governance (ESG) investment risk, which is the risk that because the methodology of the Underlying Index selects and assigns weights to securities of issuers for non-financial reasons, the Funds may also underperform the broader equity market or other funds that do not utilize ESG criteria when selecting investments. The Funds are also at increased risk of industry concentration, where they may be more than 25% invested in the assets of a single industry. The Funds may also invest in derivative instruments. Changes in the value of the derivative may not correlate with the underlying asset, rate or index and the Funds could lose more than the principal amount invested. Investments in foreign market securities involve certain risks such as currency volatility, political and social instability and reduced market liquidity.

An investment in FlexShares STOXX US ESG Impact Fund and FlexShares STOXX Global ESG Impact Fund is subject to numerous risks, including possible loss of principal. The Funds are subject to the following principle risks: asset class; authorized participant concentration; concentration; counterparty; derivatives; equity securities; issuer; large cap; management; market trading; mid-cap stock; new fund; passive investment; tracking error; US issuer; and valuation. Funds' returns may not match the returns of the respective indexes. A full description of risks is in the prospectus.

1 The European Federation of Financial Analysts Societies, version 3.0 (9/2015)

2 ibid

3 CFA Institute, Environmental, Social, and Governance Issues in Investing: A Guide for Investment Professionals (2015).

Read more articles by FlexShares ETFs