Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The financial crisis of 2007-2008 and the resulting deep bear market challenged conventional wisdoms as well as modern portfolio theory. Strategies such as buy-and-hold suffered significant drawdowns. Diversification did not provide enough protection as most asset classes became highly correlated. Fearing continued market volatility and subsequent downturns, investors searched for better risk-management alternatives.

Tactical asset allocation (TAA) strategies, which have the flexibility of allocating among different asset classes without any constraint, offered a promising solution.

Driven by investors’ demand, TAA experienced renewed interest after the financial crisis. A new class of TAA managers, who use ETFs extensively and are often referred to as “tactical ETF strategists,” emerged. As of December 2015, Morningstar tracked 271 tactical ETF strategies. Assets under management and the number of tactical ETF strategies, a subset of all ETF-managed portfolios (excluding hybrid and strategic strategies), tracked by Morningstar grew exponentially between 2011 and 2014. The total AUM/AUA reached $46 billion at the end of 2013 (see Figure 1), before declining to $26 billion at the end of last year.

Figure 1: AUM and Total Number of Tactical ETF Strategies*

Source: Morningstar. * The data does not include Strategic and Hybrid ETF strategies.

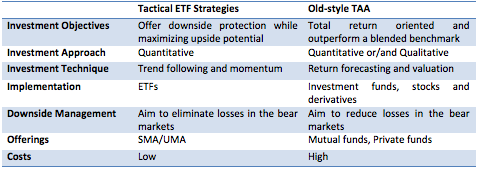

The post-crisis TAA strategies had some distinct characteristics as compared to the old-style TAA (see Table 1). Many emphasize downside protection and employ various flavors of trend-following or momentum approaches, which have proved to be the most effective ways for limiting downside losses by commodity trading advisors (CTAs) and global macro hedge funds. In addition, the new TAA strategies use ETFs extensively as they offer the ability to efficiently gain the desired market exposure after the tremendous growth of the ETF industry in last 20 years.

Table 1: Comparison of Tactical ETF Strategies with Old-style TAA

In recent years, two of the largest tactical ETF strategists (Ed. note: these were F-Squared Investments and Good Harbor Financial) struggled with some regulatory or performance issues. As a result, the tactical ETF strategies space experienced some asset outflows. However, the median tactical ETF strategy performed in line with investors’ expectations and limited the downside risks and provided diversification over the past 10 years.

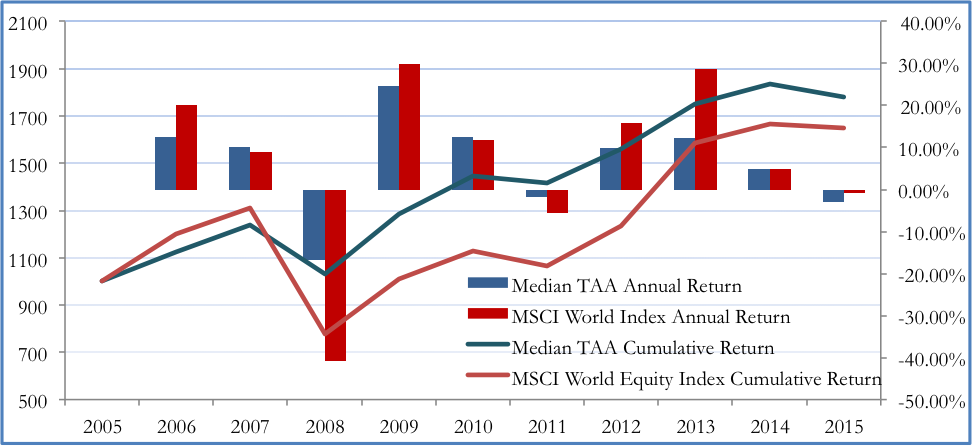

Figure 2 shows that the median TAA strategy still cumulatively outperformed MSCI World Equity Index despite the equity bull market we have experienced during the past seven years. More importantly, during the market downturn of 2008, the median TAA outperformed that index significantly. Over a full market cycle, TAA strategies have the potential to outperform general markets.

Figure 2: Historical Returns of Median Tactical ETF Strategy vs. MSCI World Index

Data Sources: Morningstar, Bloomberg.

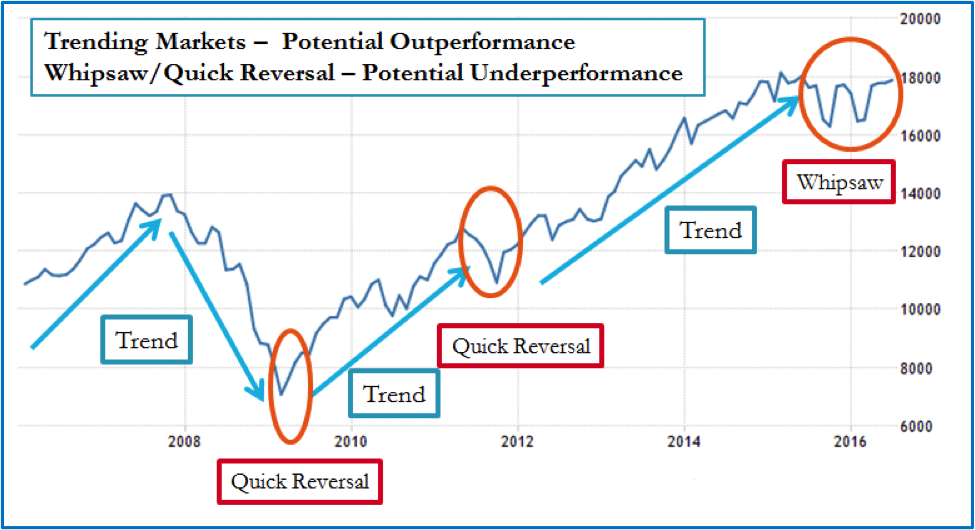

Like any other investment, TAA strategies have their own “good” times and “bad” times. Historically, the strategies performed well during the trending markets and underperformed during trendless “whipsaw” markets (see Figure 3).

In reality, the markets exhibit identifiable trends quite frequently for various economic and behavioral reasons. The economy and monetary policies usually move in cycles. The economy follows a business cycle, moving between expansion and contraction. To manage the economy, the Fed normally adopts a loose monetary policy in a contraction and a tight monetary policy in an expansion, therefore creating a liquidity cycle between “tightening” and “loosening.” Accordingly, the equity markets trend up and down, following a boom and bust cycle. Investors’ overreaction to market movements tends to extend the market trends beyond what fundamentals justify. The “whipsaw” occurs when the economy and markets start changing direction or external events shock the markets.

Figure 3: Illustration of Trending and “Whipsaw” Market Environments

Using Dow Jones Industry Average as an Example

Data Source: Tradingeconomics.com

As the current bull markets have been ongoing for over seven years, many investors have become more concerned about potential market downturns. While some investors may look to other options for downside protection, they all have their own risks or drawbacks relative to TAA strategies. Those other options include:

- Buy high-quality bonds. This is the most straight-forward choice. High-quality corporate and Treasury bonds often perform well in the bear markets. However, under the current low interest rate environment, the return expectation of high-quality bonds is diminishing. Holding high-quality bonds for the long run may not meet investors’ goals. TAA strategies offer a solution of higher expected returns than high-quality bonds over the long run.

- Buy put options. This is another natural way to hedge downside risk. However, options are prohibitively expensive. Unless you purchase put options with excellent timing, buying options is almost a sure way to lose money. Most options expire worthless.

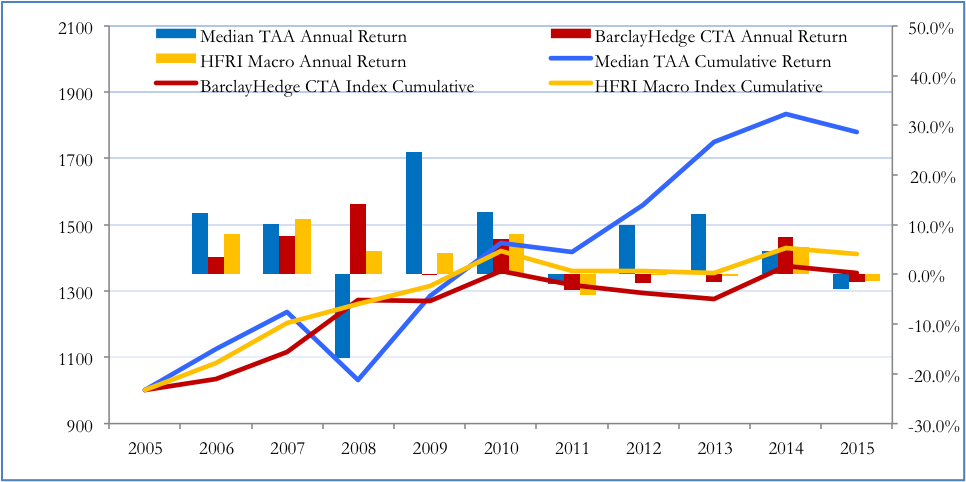

- Invest in managed futures or global macro funds. Hedge funds are expensive, normally charging a 2% management fee and 20% performance fee. The after-fee returns of managed futures and macro funds have not been as attractive as those of TAA strategies, though they performed better than TAA in 2008 (see Figure 4).

Compared to these three options, TAA strategies offer efficient and cost-effective solutions that provide better upside potentials. Investors should use TAA strategies as complements to other downside-protection strategies. The TAA strategies space will continue to grow despite recent hiccups. From an investor’s perspective, the best way to utilize TAA strategies is to allocate part of his/her portfolio to high-performing TAA strategies along with other strategies like CTAs or macro funds.

Figure 4: Historical Returns of Median TAA, CTA Index and Macro Hedge Fund Index

Data Sources: Morningstar, BarclayHedge, Hedge Fund Research

Dr. Henry Ma is the president at Julex Capital. He spent 20 years as a hedge fund manager and a director of quantitative research with Geode Capital, Loomis Sayles, Fortis Investments and John Hancock. He earned a Ph.D. in economics from Boston University and a BA from Beijing University.

Email: [email protected] Address: 101 Federal Street, Suite 1900, Boston, MA 02110

Read more articles by Henry Ma, Ph.D., CFA