Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I’ve heard a lot about recently about how investing is a “battlefield” and only those who are working hard can achieve outsized returns in this “environment.” As an advisor focused on long-term performance, prudent diversification and costs, my experience has been much different. I find the current environment quite conducive to positive returns. If anything, I’m worried about investor complacency.

The battlefield story is important for high-fee advisors and money managers because it justifies their existence. Morningstar offers a category of funds labeled “tactical allocation,” which sounds to me like what you would need on the battlefield.

Tactical allocation funds aim to provide better risk-adjusted returns to investors through changes in portfolio allocation based on a range of investment strategies. Some funds shift assets globally based on projected returns in different markets. Some funds shift back and forth between stocks and bonds. Some have broad mandates that allow a wide range of investment opportunities. And some have a narrow mandate that must keep an equity allocation in a specified range and has a limited set of possible investments. These funds earn their fees by going to battle every day.

The question is whether any of these tactical allocation mutual funds have shown any ability to outperform a simple, passively managed 60/40 portfolio. The answer, at least for the last five years, is a resounding “no.”

Jeffrey Ptak of Morningstar wrote an article in 2012 that highlighted the poor performance of tactical allocation funds. He compared the performance of the universe of tactical allocation funds in Morningstar’s database against the performance of Vanguard’s Balanced Index (VBIAX). He found that “very few tactical funds generated better risk-adjusted returns than Vanguard Balanced Index’s over the extended time period we studied.”

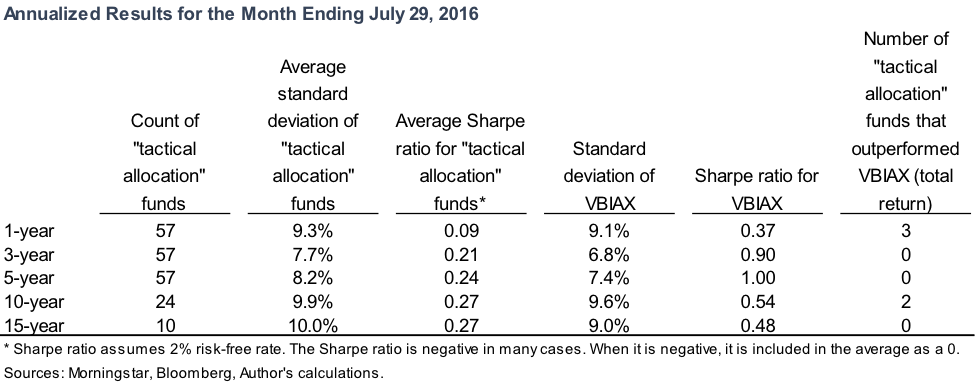

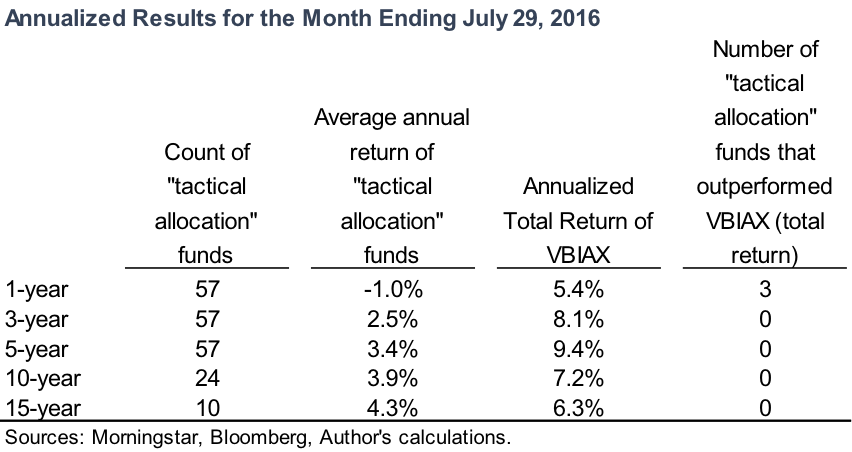

I decided to update this research to look at the most recent five-year period. I started by pulling the universe of funds in Morningstar’s database with a fund category of “tactical allocation.” I only included funds with data for at least the last five years. Through Morningstar’s fund screener, I selected only the lowest-cost share class of each fund, which left me with 57 funds. This is smaller than Ptak’s original universe of funds, but he told me that Morningstar has only recently created the peer group and it has stricter rules for inclusion than his original dataset. Notably, I only included funds that have survived for the last five years, meaning any funds that were shut down are not included in my analysis. This should theoretically bias results upward.

I then pulled total returns (gross of dividends, net of fees) for these 57 funds and for Vanguard’s VBIAX fund from Bloomberg. Based on Ptak’s research, I expected that only a handful of tactical allocation funds would outperform the Vanguard index after fees. Fees on the 57 funds range from 0.55% to 2.47%, with an average of 1.38%. The fees on VBIAX are 0.08%.

What I found was surprising. Not only has the group of tactical allocation funds underperformed, but not a single one of them outperformed the simple, low-cost, passive fund.

There was not a single outperformer in the bunch. One would think, by chance alone, that at least one of these funds would outperform. But no, their performance has been universally lousy. I also looked at the 10- and 15-year performance, over which time there were exactly zero outperformers. On the plus side for tactical managers, three of the 57 funds have shown outperformance over the last one-year period.

I figured I must be looking at something wrong. Maybe the goal of these funds isn’t outperformance. Perhaps the goal is just to reduce volatility and create better risk-adjusted returns. I looked next at the Sharpe ratio of these funds to see whether they outperformed on a “risk-adjusted” basis. No dice.