One of the defining distinctions for retirement income planning, as opposed to traditional wealth management, is that the focus shifts to best meeting an ongoing spending objective in retirement. Traditional target-date funds (TDFs) aren’t designed to meet a spending objective; their focus is on growing nominal account balances while also managing account balance volatility. However, a stable account balance does not necessarily translate to stable income. Dimensional Fund Advisors’ (DFA) new target-date retirement income funds bridge this divide by providing a target-date fund that uses a more complete risk management framework that manages volatility of expected affordable retirement spending.

In 2012, I wrote here about Dimensional’s Managed DC® pension. At that time, greater effort was made by DFA to encourage the purchase of an inflation-adjusted income annuity at the retirement date. Its focus has always been on the income side and a more complete risk management framework. Since that time, however, DFA’s approach has evolved to include a mutual fund offering in their new target-date retirement income funds.

Advisors serving retirees should pay attention to these developments.

Retirement goals: Manage wealth or spending?

The essential point to understanding how target-date retirement income funds differ dramatically from traditional target date funds is to realize that controlling account balance volatility and spending volatility are two entirely different matters. It is easy to overlook this point in our world where something like the 4% rule tends to be the default retirement strategy. The 4% rule indicates that an inflation-adjusted income equal to 4% of the retirement-date wealth level will be sustainable from a portfolio of stocks and bonds. Its success is justified because it worked historically or can be expected to work on average, rather than because any effort is made to link how current interest rates or capital market expectations relate to a sustainable spending rate.

Target-date funds focus on controlling portfolio volatility as the target (retirement) date approaches. This focus may be due either to the belief that capital preservation becomes the primary concern of the retiree near their target date, or due to a naïve belief (because something like the 4% rule is in the back of one’s mind) that reduced portfolio volatility is equivalent to sustainable and non-fluctuating spending power.

To understand why a stable account balance does not necessarily translate into sustainable income, we must take a step back to view the spending objective for retirement. Because target-date funds, by design, must be generalized to provide a reasonably close approximation to the typical investor needs, DFA views the spending objective for the target-date income fund to provide support for 25 years of inflation-adjusted spending commencing at the target date. This could reflect ages 65 to 90, for instance. Twenty-five years extends beyond the life expectancy for 65 year olds, but there is still risk of outliving this time frame. However, lengthening time frames require spending less to extend assets out for longer, and DFA views 25 years as a reasonable compromise between supporting longevity and supporting higher income for the typical investor.

The next step is to recognize which variables create the largest impact on the amount of wealth needed to support 25 years of inflation-adjusted spending. General market volatility may be important for those seeking a higher income through the inclusion of growth assets with a risk premium, but it is important to assess the importance of interest rates and inflation. This is why traditional target-date funds fail to support a retirement spending objective. They rarely make sufficient effort to coordinate the investments to provide proper hedging for interest rate and inflation variability.

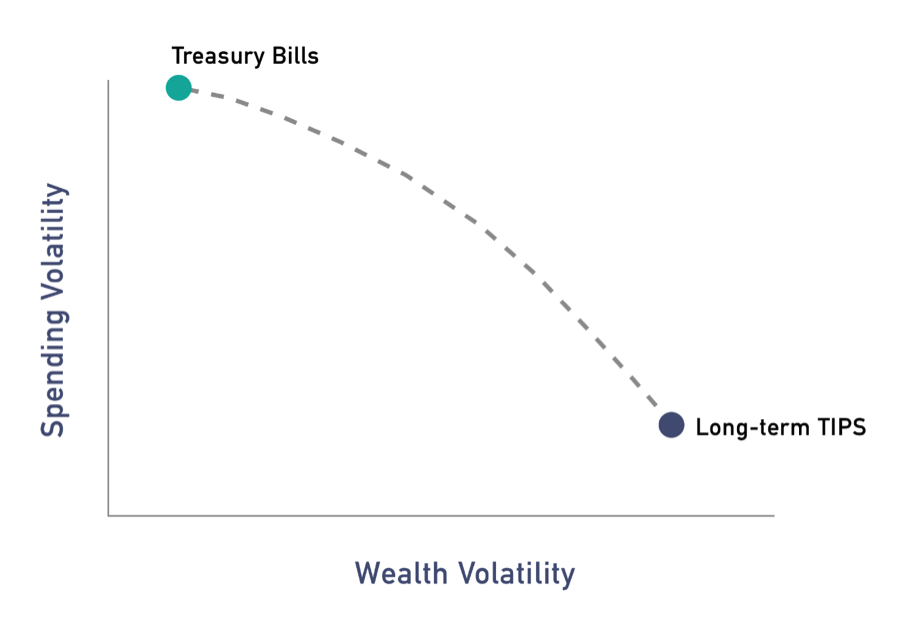

DFA illustrates this situation by comparing a portfolio of Treasury bills with a portfolio of Treasury Inflation-Protected Securities (TIPS). The former are short-term nominal investments, while the latter are specifically designed to have a duration that matches the duration of the 25-year spending objective. For a portfolio of Treasury bills, nominal wealth remains fairly stable, with growth reflected by what is offered with short-term interest rates as they fluctuate over time. However, when framed from the perspective of the amount of real retirement spending a portfolio of Treasury bills can sustain has lots of volatility. Rising inflation and decreasing real interest rates will decrease the amount of real spending that the portfolio can support over 25 years. High inflation means that required spending may grow faster than the portfolio balance, and decreasing real interest rates increase the present value of the spending stream. Since the value of Treasury bills does not grow sufficiently when interest rates drop, sustainable spending falls. Though Treasury bills can keep wealth stable, the real spending these investments can support is actually quite volatile.

Contrast this with a portfolio of TIPS with the same duration as the spending goal. TIPS provide inflation protection. If inflation rises, TIPS support greater income to match what is needed for the real spending goal. And as financial advisors know, the duration of a bond portfolio reflects the sensitivity of the portfolio’s value to fluctuations in interest rates. When the TIPS portfolio is created to have the same duration as the spending objective, interest rate fluctuations are hedged. When interest rates decrease, the cost of the spending objective increases and the value of the TIPS portfolio rises accordingly. If interest rates rise, then the TIPS portfolio loses value, but the cost of meeting the spending objective also decreases. Interest rate risk is hedged.

For a portfolio of long-term TIPS, the account balances may be quite volatile as inflation and interest rates fluctuate, but the sustainable amount of inflation-adjusted spending remains reasonably level. Figure 1 illustrates these ideas: Treasury bills support low wealth volatility but high spending volatility, while TIPS support low spending volatility but high wealth volatility.

The question then becomes: What is the appropriate tradeoff between those outcomes for the typical target date investor?

Figure 1: Tradeoffs in retirement

Dimensional’s target-date retirement income funds

The next step is to understand the objectives of the retirement saver. As our world has transitioned from defined-benefit pensions to defined-contribution pensions, the focal point of retirement has transitioned from a monthly or annual income amount to a portfolio value. The typical target-date fund investor seeks a sustainable income in retirement, but the number they see on their financial statements is the aggregate wealth in their account. As we just reviewed, aggregate account balances do not directly translate to sustainable spending. The portfolio can remain quite stable, while sustainable income fluctuates in ways that most investors do not realize.

Traditional target-date funds reflect this same problem. As they generally transition from stocks to nominal bonds as the retirement date approaches, their objective is to provide some stability for portfolio fluctuations while also seeking some growth. But without the efforts to provide inflation-protection or duration-matching through the growing fixed income portion of the portfolio, the ability for an account balance to support the spending objective is hampered.

This is where DFA’s Target-Date Retirement Income Funds enter the scene as an alternative to traditional TDFs. These funds share the same philosophy as TDFs pre-retirement in terms of accounting for the relative size of human capital and financial capital over time and reducing the stock allocation as human capital decreases with age. A globally diversified portfolio of stocks and bonds is designed to grow the portfolio and the sustainable income base. But rather than transitioning from stocks into duration mismatched nominal bonds as the target date approaches, DFA’s funds transition into a portfolio of TIPS with the same duration as a 25-year real spending objective beginning at the target date. This allows the investments to better lock-in an inflation-adjusted income stream for retirement. It provides a more effective way to achieve the actual objectives of the typical TDF investor to support their retirement spending by managing the risks related to inflation and interest rate fluctuations while still leaving some assets to focus on growth.

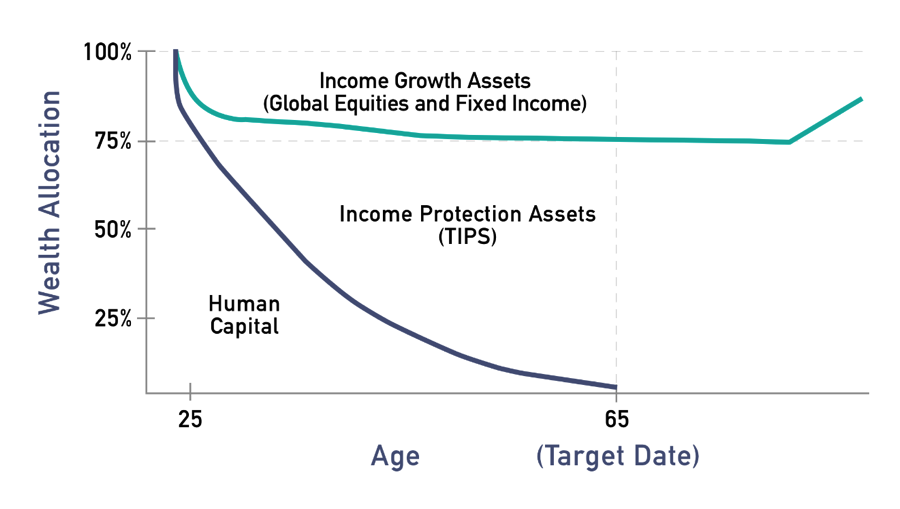

Figure 2 provides a generalized illustration for the allocation of household wealth over the investor’s lifetime using target-date retirement income funds. When the investor is far from the target date, household wealth is presumably held primarily as human capital. It is future labor earnings. For the smaller investment portfolio, the asset allocation focuses on growth, primarily with global equities. For example, at the end of 2015, DFA’s 2060 Target Date Retirement Income Fund was invested 94.9% in global equities and 5.1% in global bonds. As the investor gets to be within 25 years of the target date, global equities begin to give way to more fixed income, and this is when the TIPS investments play a larger role. For instance, DFA’s 2030 target-date retirement income fund (15 years to the target date) had an allocation of 63% global equities, 14.7% global bonds and 22.3% TIPS by the end of 2015. At the target date, asset allocation is designed to be 25% global equities and 75% TIPS. There are no global bonds at this point. Human capital is also depleted and household wealth is primarily held in the investment portfolio. The equity allocation still seeks wealth growth to support more future income, while the fixed income assets are specifically designed to support a 25-year inflation-adjusted spending objective. DFA provides a calculator on their website to help users determine the amount of sustainable income their assets can be expected to provide.

Figure 2: Lifetime allocation of household wealth

The bottom line

DFA’s target-date retirement income funds have grown out of efforts to provide a seamless way for investors to receive a defined-benefit styled income from their defined-contribution account. This is based on work initiated by Nobel-laureate Robert Merton with his company, SmartNest, which was purchased by DFA. DFA’s new target-date retirement income funds exist entirely within the world of a mutual fund solution covered by the Investment Company Act of 1940. While not providing as pure form of longevity protection, these funds do provide a much more effective way for TDFs to meet the actual retirement objectives of most clients.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management, helping to build model investment portfolios that can be integrated into comprehensive retirement income strategies. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Read more articles by Wade Pfau