Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Leading economic indicators are pointing toward a weakening economy. Most economists are still reluctant to call a recession, although the likelihood is higher than it has been in the recent past. However, that is not a signal for investors to adjust their portfolios.

The American Institute for Economic Research’s (AIER) index of leading indicators showed a reading of 38 in April and May. This “diffusion index” suggests that fewer than 50% of the 12 indicators are showing expansion. AIER says that it is too early to call recession. AIER points out, “There have been previous instances (months in 2003 and 2005, for example) when the index dipped below 50 but bounced back the following month. On one occasion in 1995, it fell below 50 for an extended period, yet no recession occurred.”

Nonetheless, the threat of recession is real. The revised reading on first quarter 2016 GDP came in at 0.8%. With such a narrow margin above zero, this means a stiff breeze could knock GDP into the red. The technical definition of a recession is two consecutive quarters of negative GDP. Although most economists believe that GDP will rebound during the course of 2016, recessions are difficult to predict and could be triggered by some yet unforeseeable force.

So, it’s certainly possible that a modest recession begins in the not-too-distant future and lasts for a short time. The question is really whether investors should do anything about it.

I would argue that most people should consider doing nothing at all.

The trigger for the next recession may not be some huge event like the fall of Lehman Brothers or a stock market crash, but rather a mild slowdown in hiring as corporate earnings fail to impress investors, possibly compounded by some strange weather phenomenon, increased unrest in the Middle East or something else that we can’t know in advance. There is no huge imbalance (“bubble”) like there was in 1929 or 2006-2007. This is business cycles being business cycles. There is not much investors can do to prepare, nor should they.

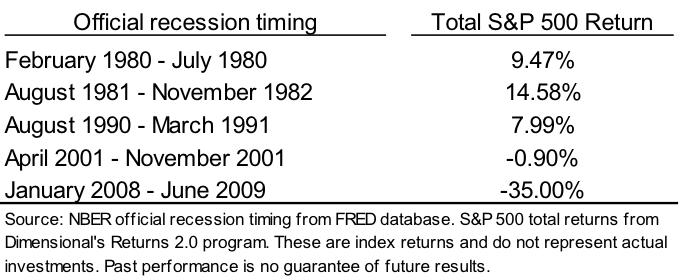

If we look at the four recessions that occurred before the most recent one, we see that not all recessions were synchronized with huge market pullbacks like the one that we last lived through. Scurrying to get out of stocks, even at exactly the beginning of the recession, would have been unnecessary during three of the last five recessions. Add that to the fact that it is impossible to predict when the market will peak and when it will bottom, and most long-term investors are better off staying put.

Admittedly, this isn’t a rigorous statistical analysis. But based on the five recessions that have occurred since 1980, it is clear that even with perfect foresight about when these recessions started it would be impossible to know whether investors should change anything at all.

This shouldn’t be surprising. The stock market is commonly recognized as a leading indicator of the business cycle, not the other way round. Even this link is tenuous, however, as Paul Samuelson famously quipped in 1966 that the stock market had successfully predicted nine out of the past five recessions.