Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Every four years, investors guess what the outcome of the presidential race will mean for the stock market and their portfolios. This topic is contentions and infused with partisan bias. I’ll provide some useful context for those discussions, for your formal presentations to clients or for casual cocktail party fodder.

The conclusions reached by those who have researched the topic are often contradictory, as you can see in the examples below:

“Presidential election years generally have coincided with favorable markets, particularly when the incumbent party wins.” - T. Rowe Price.

“Over the past century, which party occupies the White House has had no discernible or consistent impact on US equity markets.” – BlackRock.

“[The authors of the 2003 Journal of Finance article] found 9% higher stock market gains for large stocks in Democratic administrations since 1928.” - Pete Davis, CapitalGainsandGames

“Most of the studies show quite an advantage for equities following the election of Democrats, but a Federal Reserve study concludes there is no consistent relationship if you correct for market volatility and test back to 1852.” - Pete Davis, CapitalGainsandGames

Jeremy Grantham’s study

Before I present my own findings, let’s first review the most-widely cited research on presidential cycles and market performance, which is the work of Jeremy Grantham.

Based on observations of presidential election cycles made by Grantham, co-founder and chief investment strategist of Boston-based Grantham Mayo van Otterloo (GMO), pre-election years (the third year of the four-year term) have historically been good for equity investors, especially over the past century.

On average, the pre-election year has seen a 10.4% gain since 1833. So, generally speaking, the year before the presidential election and even the actual presidential election years are historically good for the stock market.

But my article asks a different question. Specifically, what has happened to stocks when there is a change in party leadership? Does is matter to investors which party is in power? In order to focus on the potential impact of a change in leadership, I limited my research to the first 12 months after a change in leadership took place. I wanted to find out how the market reacted to the initial burst of policy initiatives that every new president proposes, using the political capital that comes from wresting control of the levers of power from the opposing party.

The sample size is too small and there are too many possible time frames one can choose for measuring the correlation between presidential elections and stock market returns. Rather than trying to make a case for causality based on questionable statistical methodology, I chose to look at past presidential elections and note what happened in the stock market.

I leave it up to the reader to draw his or her own conclusions about what, if anything, might be relevant to the upcoming change in tenants at 1600 Pennsylvania Avenue.

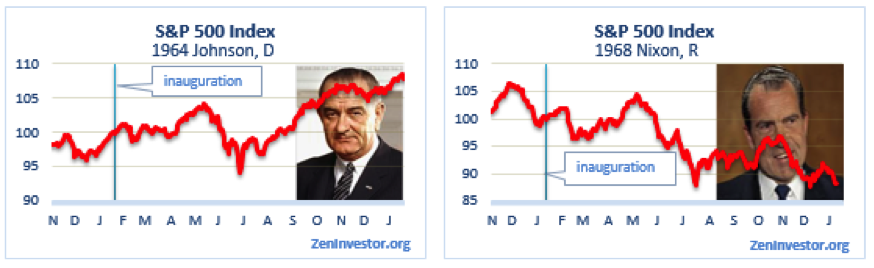

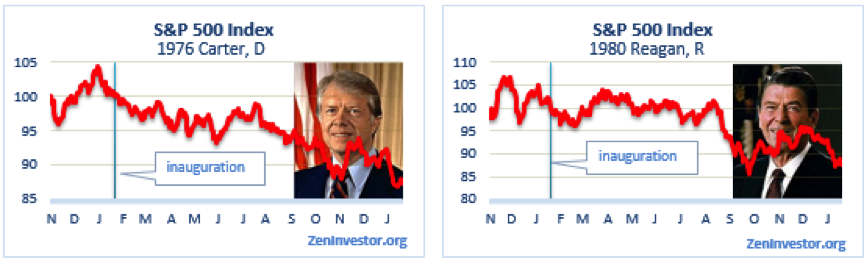

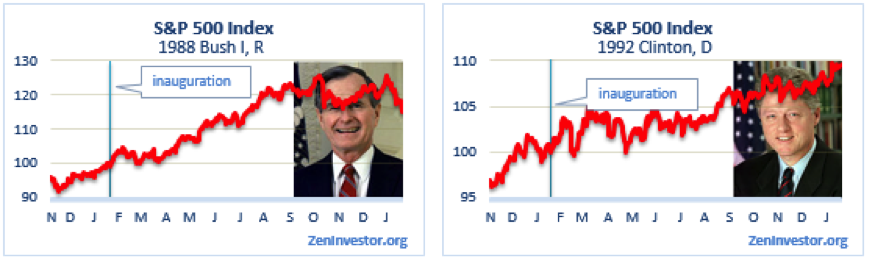

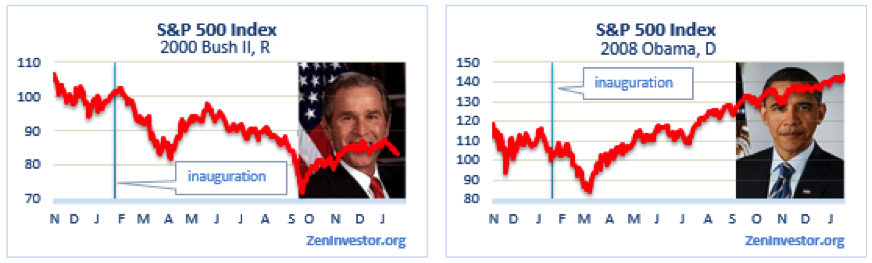

First, some ground rules. I limited my research to the “modern era” – from 1952 to present day. I did so because I wanted to avoid two world wars, the Great Depression and anything that pre-dated the establishment of the Federal Reserve. In other words, I wanted to limit my research to the election of presidents to whom I can relate. (I was in grade school when Eisenhower was elected, and I can remember seeing “I Like Ike!” banners, yard signs and buttons everywhere. I didn’t know what it all meant, but I could see that people were going crazy for the guy.)

Next, I only looked at elections where the occupant of the White House changed. I figured that if we re-elected a president for a second term, it meant that things were going well and I wasn’t interested in how the market reacted to it. But the rise of a new leader is a big deal, and I wanted to know what happened to the market when there was a changing of the guard.

I struggled with the time frame. I eventually settled on the period starting on Election Day in November, through the first 12 months of the new president’s term. That gave me a total of 14 months of market action to look at. Even though the new commander-in-chief doesn’t actually start the job until January 20th, the stock market is a forward-looking mechanism. So as far as the market is concerned, Election Day is the beginning of the new regime, notwithstanding the formality of the inauguration.

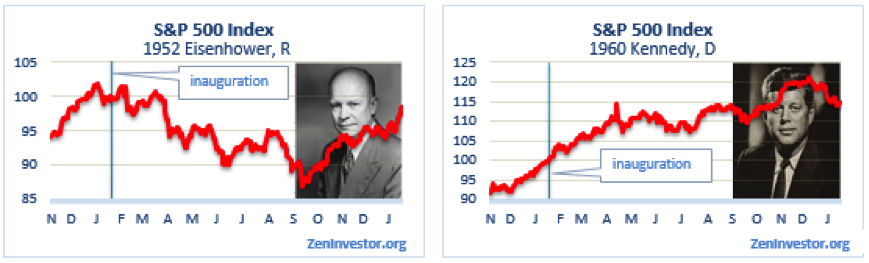

In order to draw attention to the period between Election Day and inauguration day, and to make each episode consistent, I drew the charts so that they all start at a base of 100 on inauguration day. That way we can see what happened between Election Day and the start of the term, and then we can compare market performance on an apples-to-apples basis for the first full year of the new president’s reign. The market performance comparison is from inauguration day on January 20th to January 20th of the following year – 12 full months.

Conventional wisdom suggests that Republican administrations, which are ideologically more business-friendly than Democratic administrations, would be more bullish for the stock market. But a review of the record since 1950 shows something different. History shows that the stock market does better, by a considerable margin, when the occupant in the White house changes from a Republican to a Democrat. Again, I’ll leave it up to the reader to determine why this is so.

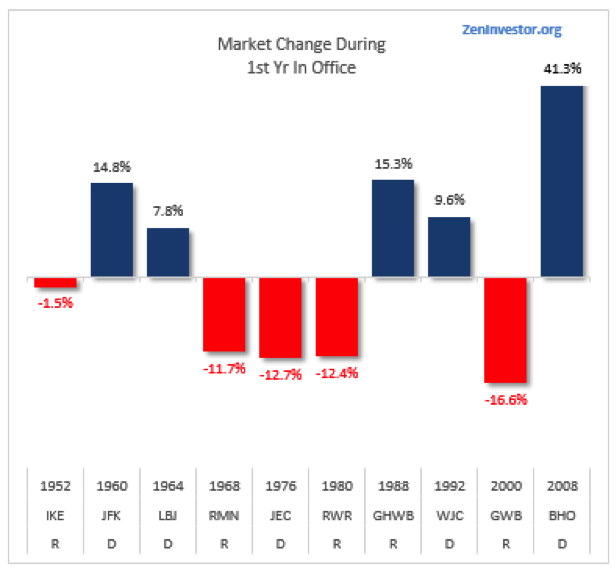

Chart 1. Change in S&P 500 during the first 12 months of a new administration

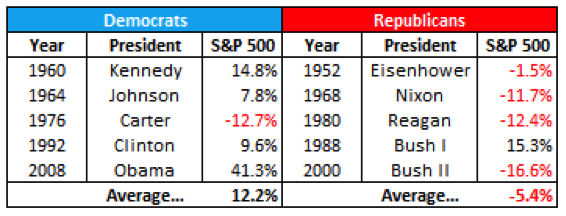

The market has averaged a gain of 12.2% during the first year of a Democratic administration. For Republicans, the market has produced a loss of 5.4% on average. That’s a stark contrast. Now let’s look at the numbers for each party separately.

Chart 2. Market performance during first year, by party

Investors do care which party occupies the White House. But this is a two-way street. The stock market has a good track record for predicting which party will win the election. If the stock market is up during the three months leading up to the election, the incumbent party has the advantage. Losses over those three months favor the challenger.

In the 22 presidential elections since 1928, 14 were preceded by gains and 8 by losses. In 12 of the 14 market-positive, pre-election run-ups, the incumbent (or the incumbent party) prevailed. And in seven of the eight market-negative run-ups, incumbents lost. This means there were only three exceptions out of 22 races: 1956, 1968 and 1980. Put another way, the S&P 500 has an 86% success rate in forecasting the election results. It will be valuable to see what happens in the market during August, September and October of this year.

Lastly, I’ll leave you with 10 individual charts showing the track of the market during the 14 months between Election Day and the end of the first full year of each new president’s term.

Charts 3 – 7. First year market performance for each new administration since 1950

What might a Trump or Clinton presidency mean for the stock market? Nobody knows. But it’s interesting to look back in time and see how the market has reacted to changes in leadership.

Erik Conley is the former head of equity trading at Northern Trust Co. in Chicago. After a 30-year career in trading and portfolio management, he now runs a nonprofit investor education and advocacy organization called ZenInvestor NFP. His website is www.ZenInvestor.org and you can reach him at [email protected]

Read more articles by T. Erik Conley