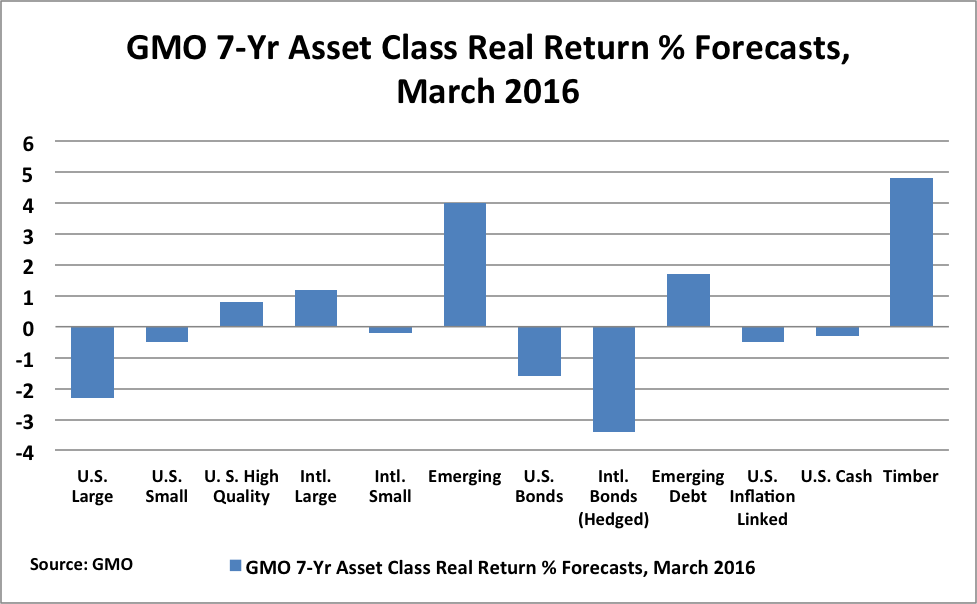

The English journalist and economist Andrew Smithers has called “stockbroker economics” the belief that all news is good news and stocks are always cheap. Advisors recognize the fallacy of that logic and rely on diversification to counter the inevitable asset-class volatility that markets deliver. But, according to many forecasts – including those from GMO – virtually all asset classes are likely to perform poorly over the next decade.

Portfolio diversification should give an investor exposure at all times to at least one asset class (and hopefully more) that’s poised to do well. Of course, practically, that means usually having exposure to poorly performing asset classes too. But the theory, as advisors know well and explain to their clients on a daily basis, is that, with diversification, you’ll damp volatility while enjoying decent returns over the long run.

To do well over a full cycle, however, you must purchase an asset class at a cheap price – or at least a reasonable one. It has to be priced to deliver good returns. And yet, most asset allocators prefer to avoid trying to value asset classes, viewing the exercise to be as pointless as index fans view the appraisal of individual stocks.

But viewing the exercise as pointless carries a contradiction. The same people who view asset class valuation as pointless often view stocks as perennially poised or priced to deliver strong, inflation-beating returns – which, of course, implies a valuation or return forecast. The contradiction is that one isn’t avoiding asset class valuation if one thinks stocks are perennially priced to beat inflation by a handsome amount (say, “Siegel’s constant” of 6.5%, real) and bonds are priced at least to keep up with inflation. One is merely defaulting to a naïve assertion.

Up until 2000, advisors had been able to engage in that contradiction without much worry. Since then, the S&P 500 has only delivered 4% or so annualized. But other asset classes have picked up the slack when stocks have faltered, vindicating widely diversified approaches to portfolio construction, if not simply “stocks for the long run.”

But there’s no law of finance that says that diversification must bail portfolios out when developed country stocks fail. There doesn’t always have to be a few cheap asset classes. In fact, it isn’t clear that any asset class currently offers compelling future returns, or that investors who diligently diversify will be rewarded for their discipline and efforts.

Asset class convergence

The financial crisis should have put doubt into advisors and consultants. Almost nothing performed well during that period except for U.S. Treasury bonds and agency mortgages, but almost everything performed well coming out of it except for emerging-markets stocks, which are down slightly.

Diversification didn’t help going into the crisis, and it hasn’t hurt coming out.

The second half of that observation comforts advisors, but it should also frighten them. After dropping simultaneously, asset classes have risen at once. And that may mean they are all expensive.

Before examining likely future asset class returns, it’s important to revisit the technology boom and bust because that’s the last time diversification worked well. Understandably, it’s also the story about diversification advisors are eager to tell – perhaps too eager.

Diversification pays off during the tech bust

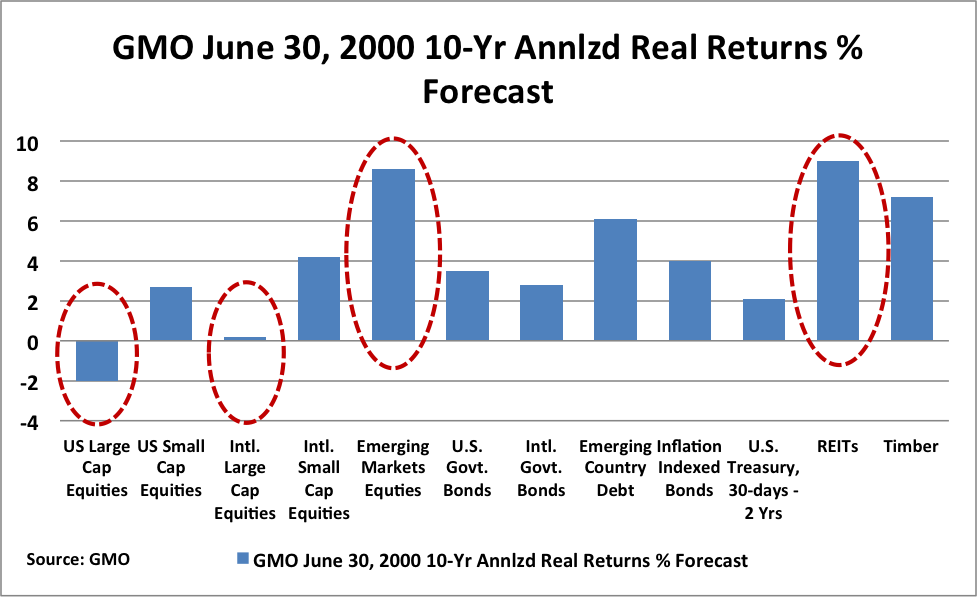

During the climax of the technology boom, the Shiller PE (price relative to the past 10-years real average earnings) of the S&P 500 reached its all-time high of 44. The ensuing decade was predictably unkind to the index, as it produced just under a 1% annualized return. Appropriately, it is often called the “lost decade” for stocks – or at least U.S. large-cap stocks.

But in their mania for large-cap technology stocks, investors neglected other parts of the stock market and other asset classes. Small-cap and mid-cap stocks uninvolved in technology were forgotten. REITs – bricks-and-mortar with the prosaic collection of rent -- were the epitome of unfashionable, “old economy” stocks.

Emerging-market stocks, with their emphasis on energy and materials, were also orphaned. Pulling commodities out of the ground was so boring compared to software development and anything related to the Internet. These were the days when Fidelity rolled out Select Networking and Infrastructure and Select Wireless funds, only to shutter them both after 80%+ cumulative drops in the years after the bubble’s peak.

Bonds also looked like they were suitable only for people deep into retirement, if anyone at all. Why waste your time with 5% when technology funds like Fidelity Aggressive Growth FDEGX (long since renamed) returned 103% and a slew of Janus funds returned over 70% in 1999? Even high-yield bonds seemed too tame to investors and, thus, were mostly forgotten.

In other words, almost everything besides developed country large-cap stocks and especially technology stocks was poised to deliver solid returns in 2000, and some asset classes were poised to deliver outstanding returns. Diversification away from U.S. and European large-caps paid off in spades. Anyone who had the courage to underweight the S&P 500, with its 44 Shiller PE, in 2000 could have chosen nearly anything else and justifiably felt vindicated at the end of the decade.

Misleading charts and “stockbroker economics”

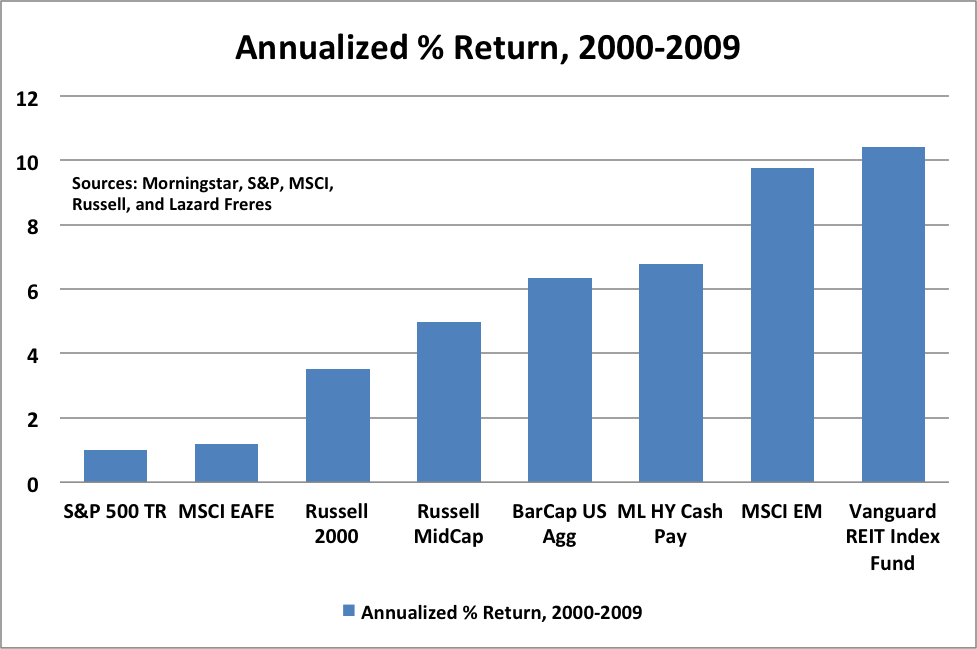

The problem is that many are eager to spin a tale that diversification will pay off again. Therefore, charts like the following one proliferate on reports from asset managers and on the blogs and Twitter feeds of social media-savvy advisors.[i]

The problem with the chart is not that it’s false. Those are the returns of those asset classes over that time frame. But it is misleading because, in addition to being a single random time frame, it has no reference to starting dividend yield and valuation for stocks or starting yield for bonds. It also gives the impression that because diversification worked starting in 2000, it can work again.

Therefore, the chart is a version of Smithers’ stockbroker economics.

Developed country large cap stocks may not always be poised for strong returns. But, given how many other asset classes did well from 2000 through 2009, it’s no wonder brokers, advisors and consultants use the chart to put prospects and existing clients at ease.