Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Considerable research argues that retirees benefit from creating guaranteed income streams through single-premium immediate annuities (SPIAs). The research finds higher success rates (not running out of money), along with higher average spending, higher minimum spending and greater utility with at least partial annuitization. I have referenced several papers that discuss this finding, and Pfau (2013) does a succinct and thorough literature review that covers the evolution of this topic.

This paper analyzes one aspect of this discussion – whether or not to use inflation-adjusted versus fixed SPIAs, and how a retiree can create inflation-adjusted income using fixed (nominal) SPIAs alongside an investment portfolio. Pfau (2013) finds that an efficient frontier for retirement income includes stocks and SPIAs, but not necessarily inflation-adjusted SPIAs, variable annuities (VAs) or bonds. Pfau states, “[F]ixed SPIAs dominate inflation-adjusted SPIAs in the retirement portfolio.” He references a comment by Joseph Tomlinson that “either because of a lack of competition or because of the difficulties of hedging inflation risks, inflation-adjusted SPIAs are not priced competitively with fixed SPIAs.”

One conclusion is that retirees who want inflation-adjusted income should purchase fixed SPIAs and “invest the difference” in order to protect against inflation by drawing down an investment portfolio as needed. My analysis tests that assertion. I consider various return and inflation paths to determine an appropriate asset allocation that would enable annual inflation adjustments for fixed SPIAs. I find that if retirees are willing to accept some probability of failure – perhaps less than 10% – they can create their own inflation adjustment and leave additional funds for liquidity needs or a legacy. However, risk-averse retirees who choose to use SPIAs may decide that inflation-adjusted SPIAs are worth the additional cost for their guaranteed inflation adjustments.

Methodology and assumptions

I start by looking at current payout rates for a 65-year-old married couple for a 100% joint and survivor SPIA. These rates are based on the current average quote provided by Vanguard Annuity Access powered by Income Solutions (quotes provided based on payment start date of April 1, 2016). Based on a hypothetical $100,000 deposit, the couple could get $3,884 per year from the inflation-adjusted SPIA. Alternatively, they could choose to use only $69,670 to purchase a $3,884 fixed SPIA, which had an average payout rate of 5.575%. If the fixed SPIA option were chosen, it would free up $30,330 to be invested separately.

I want to determine how this $30,330 could be invested among stocks and bonds in order to make up for the lack of annual inflation adjustment in the fixed SPIA. In order to analyze this, I ran a bootstrapped simulation that created 10,000 different return streams of stocks, bonds and inflation.

This method works by first drawing months at random using monthly data from January 1926 through January 2016. For each draw, there is a corresponding stock return, bond return and inflation. Using the randomly selected draws, the simulation creates 10,000 unique return streams of 50 years. This process assumes that returns are independently distributed, meaning that there is no serial correlation. However, by choosing the returns associated with a given month across all three data series, I maintain the historical correlation and volatility of stocks, bonds and inflation. In other words, if I draw June 1956 as the return in a certain simulation, I use the stock, bond and inflation returns associated with June 1956.

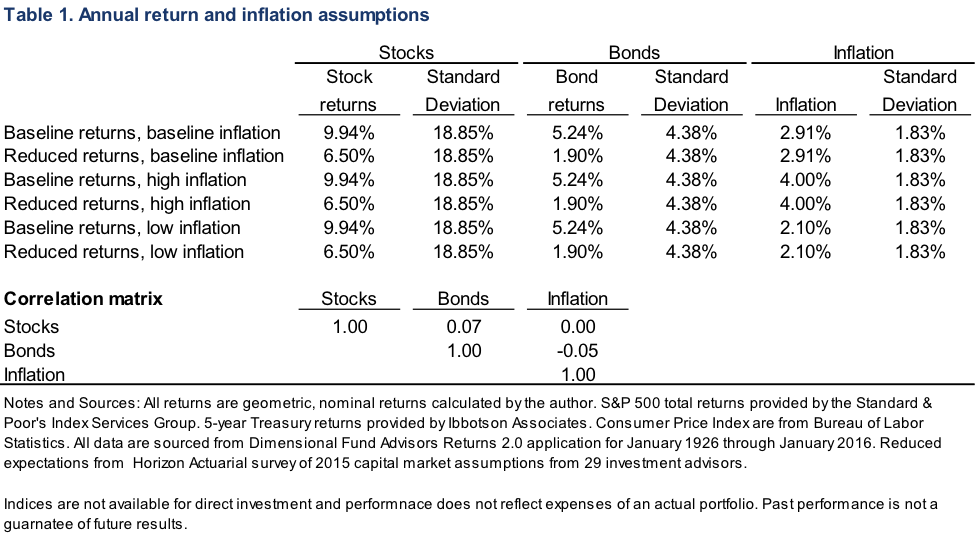

I use two variations of returns: baseline and reduced returns (in order to provide a more conservative estimate). In the baseline simulation, I draw historical returns from the S&P 500 (total return) for stock returns and historical data from 5-year U.S. Treasury securities for bond returns. In the reduced return model, I universally reduced historical stock returns by 0.2666% per month and bond returns by 0.2697% per month. These reductions cut the average returns to 6.5% per year for stocks and 1.9% per year for bonds. These assumptions are based on the 25th percentile prediction for 10- to 20-year returns from Horizon Actuarial Services’ 2015 Survey of Capital Market Assumptions.

For inflation assumptions, I used three versions: baseline, high and low inflation. Baseline inflation is the historical rate of inflation. Under the low inflation scenario, I universally reduced historical inflation by 0.0883% per month to get a 2.1% annual rate, which is also the 25th percentile projection from the survey mentioned above. In the high inflation scenario, I universally raised inflation by 0.0657% to get an annual rate of 4.0%.

Return assumptions and correlations are listed in the table below. Note that standard deviations and correlations are consistent whether we use baseline or alternative assumptions. This is the result of the universal decrease or increase under alternative assumptions.

My goal is to evaluate the performance of various allocations when we invest the $30,330 in stocks and bonds (this amount is the difference we have by purchasing a fixed SPIA instead of an inflation-indexed SPIA). I assume an investment withdrawal that makes total income equal to the income for an inflation-protected SPIA with the same starting payout. This is an engineered inflation-protected income stream.

I evaluate combinations of stocks and bonds in 10 percentage point increments. There are 11 such combinations. I run each of these combinations through the 10,000 simulations to determine how often the investment portfolio would run out and how much would be left on average over any period of time. The portfolio is annually rebalanced to the original allocation.

Finally, I use 2011 period life tables from the Social Security Administration to determine the probability of at least one spouse surviving to any age. Using these probabilities, I calculate a weighted average likelihood of exhausting the pool of money by drawing inflation adjustments and a resulting weighted average median value remaining at the end of life. I hope to determine a balanced investment approach that minimizes the likelihood of exhausting the pool while also providing a potential bequest or additional liquidity during retirement.

Results

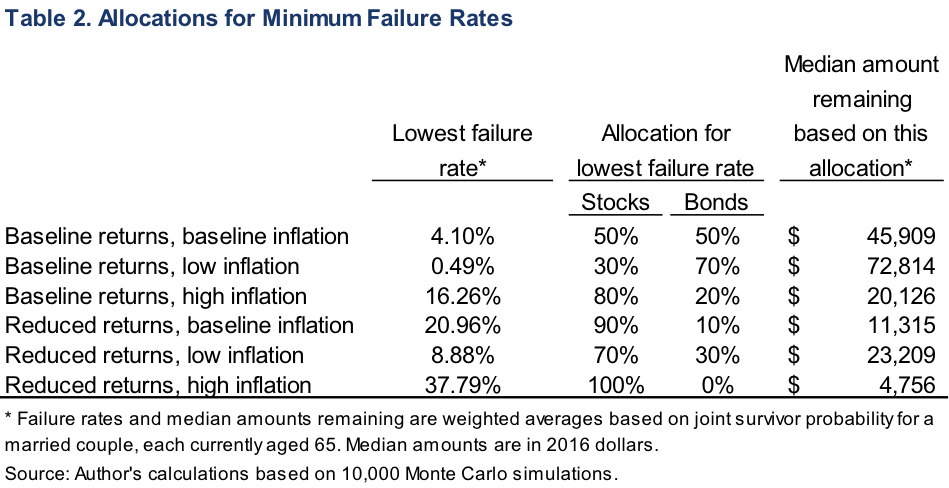

In three of the six return scenarios I tested, there was a portfolio allocation that provided for weighted average failure rates less than 10%. This means that there is less than a 10% chance that the pool of money would run out if it were used for inflation protection with a fixed SPIA.

For example, using historical (baseline) returns and inflation rates, a portfolio comprised of 50% stocks and 50% bonds would have run out in 4.1% of simulations. This level is weighted by survival probabilities. For comparison, this same 50% stock and 50% bond portfolio ran out by year 30 in 5.9% of simulations. The allocations that provide the lowest failure rates are shown in the table below.

In general, I find that if a client is willing to accept a low likelihood that the pool dedicated to inflation adjustments would run out, it is advisable to invest in a portfolio comprised of roughly 50% stocks and 50% bonds. Under reduced return assumptions, it is preferable to allocate an increased share to stocks instead of bonds.

Pay special attention to the reduced returns and baseline inflation scenario. In this scenario, a client would need to accept a nearly 21% failure rate and allocate a significant portion of the investment account to stocks. A 50/50 allocation under this scenario leads to failure in 26.4% of simulations. Under this 90/10 allocation, the client could expect a median legacy of about $11,315 (this amount is given in current dollars, and it therefore represents about 11.3% of the $100,000 available for investment). This potential pool of money would also be available for liquidity needs that might arise.

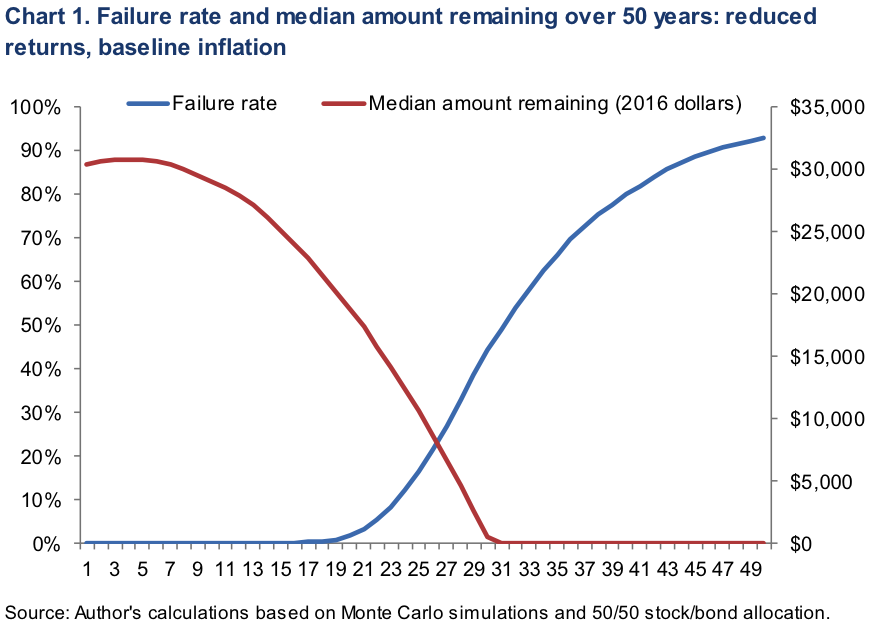

Finally, I look at how the median amount remaining and failure rates change over time under this assumption of reduced returns and baseline inflation. We look at a portfolio comprised of 50% stocks and 50% bonds.

The longer the retirement period, the more likely the pool of assets is to run out under these relatively conservative return assumptions. This may encourage the types of risk-averse and long-lived clients who opt for SPIAs to decide to use inflation-adjustment SPIAs and forego this additional risk.

Conclusion and further considerations

This analysis looks only at two asset classes and could easily be extended to include others. The most likely candidate would be TIPS. Another candidate would be gold or other precious metals, which some claim to be good hedges against inflation. This analysis also only considers funding from qualified accounts such as an IRA, which would be taxable. A similar assessment that looked at non-qualified assets found that the tax benefit of inflation-adjusted SPIAs may make them relatively more attractive (Schirripa 2009). Finally, this analysis ignores any costs associated with portfolio management; those costs would reduce overall returns. These considerations could be assessed in future research.

In general, investing the difference in cost between fixed SPIAs and inflation-adjusted SPIAs provides a reasonable likelihood of success for “self-managed” inflation adjustments throughout retirement. An allocation of 50% stocks and 50% bonds will likely enable a client to provide these inflation adjustments, but the client should be willing to accept some probability that they will “lose the gamble” and exhaust the pool of money before the end of retirement. This potential for losing the gamble should be considered against the potential for increased legacy and/or increased liquidity during retirement, and many risk-averse retirees may instead opt for inflation-protected SPIAs, despite their increased costs.

Luke F. Delorme is the director of financial planning at American Investment Services, Inc. He has published articles in AAII Journal, Journal of Financial Planning, Retirement Management Journal and the Journal of Nonprofit Management and Leadership. He received his MBA from Boston College and received the Wall Street Journal award for the top finance student. His email is [email protected].

References

Ameriks, John, Robert Veres, and Mark J. Warshawsky. 2001. “Making Retirement Income Last a Lifetime.” Journal of Financial Planning 14, 12 (December) 60–76.

Chen, Peng, and Moshe A. Milevsky. 2003. “Merging Asset Allocation and Longevity Insurance: An Optimal Perspective on Payout Annuities.” Journal of Financial Planning 16, 6 (June): 52–63.

Huang, Dylan W., Matthew M. Grove, and Todd E. Taylor. 2012. “The Efficient Income Frontier: A Product Allocation Framework for Retirement.” Retirement Management Journal 2, 1 (Spring): 9–22.

Edesess, Michael. 2012. “Can you Beat SPIAs with Long Term Bonds?” Advisor Perspectives, July 17, 2012.

Malhotra, Manish. 2012. “A Framework for Finding an Appropriate Retirement Income Strategy.” Journal of Financial Planning 25, 8 (August) 50–60.

Pfau, Wade D. 2012. “Choosing a Retirement Income Strategy: A New Evaluation Framework.” Retirement Management Journal 2, 2 (Fall): 33–44.

Pfau, Wade D. 2013. “A Broader Framework for Determining an Efficient Frontier for Retirement Income.” Journal of Financial Planning 26, 2 (February): 44-51

Schirripa, Felix. 2009. “Immediate Annuity: Fixed vs. Inflation-Protected, A Cost Comparison.” Elm Income Group white paper.

Tomlinson, Joseph A. 2012. “A Utility-Based Approach to Evaluating Investment Strategies.” Journal of Financial Planning 25, 2 (February): 53–60.

Tomlinson, Joseph A. 2012. “Are Inflation-Adjusted Annuities Right for Clients? The Product and Its Prospects.” Advisor Perspectives, November 20, 2012.

Webb, Anthony. “Providing Income for a Lifetime: Bridging the Gap between Academic Research and Practical Advice.” AARP Public Policy Institute, June 2009.

Read more articles by Luke F. Delorme

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.