Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Monte Carlo (MC) analysis is the most common tool planners employ when projecting clients’ finances, yet it contains an inherent optimistic bias that has largely, if not completely, gone unnoticed. This article outlines why bias exists in MC, provides two cases that demonstrate the potential impact of MC bias and describes the factors that influence the degree of bias.

The effects can be sizeable. For a 20-year-old with moderate risk tolerance who invests a lump sum to draw upon for income at age 80, MC underestimates the recommended investment amount by almost five times. For a very conservative investor, MC can underestimate required savings by 24 times.

The cause of optimistic bias

The bias occurs because MC presumes the input assumptions for return mean and standard deviation have no error. In some applications, this is true. For instance, the probability of pulling a particular card from a standard deck of playing cards is precisely known. However, in finance, we will never know the true returns distribution exactly, so we often estimate the underlying probability distribution by using historical mean and standard deviation as inputs to MC. Doing so is analogous to being shown only five cards from a deck of unknown size and composition. With financial data, the historical parameters always contain sample error of unknown size and direction.

Before going further, two concepts are often confused that should be made clear: sample error and bias.

Sample error gauges the inaccuracy of only one sample, whereas bias is an average of the errors. For instance, when a fair coin is flipped 10 times, the resulting number of heads is likely to have sample error, such as six heads instead of five (an error of +1). If the experiment is performed correctly and repeated many times, the sample error will have a mean value of zero, and thus no bias. In other words, individual sample errors can vary -- +1, -2, -4, etc. -- but when observing an infinite stream of sample errors, the average should be zero. If bias is present, the average sample error will not be zero.

As mentioned earlier, the historical market returns fed into MC represent a sample with unknown error. Even if the input is unbiased, the sample error can produce an optimistic bias in MC predictions.

It is easy to imagine how this can happen with a biased input, but how is it possible when the sample is unbiased? The concept is demonstrated with another coin example. Assume a person has three coins in her pocket, and heads are the preferred outcomes. One coin has two heads, another coin has two tails, and a third coin is fair. The two unfair coins represent an extreme form of sample error, either plus or minus 50%. On average, the sample error of all three is zero, and there is no bias.

If the person randomly removes one coin from her pocket and flips it 10 times, what are the odds that tails will come up every time? If we assume the mean percentage of heads is 50%, as with MC and many other tools, the chance is one in 1024. Thus, MC advises that the probability of all tails is about 0.1%. However, the true odds are approximately 33% because there is a one in three chance that the two-tailed coin is pulled. The MC prediction is wildly optimistic because it does not account for sample error. Even though the sample errors of the three coins average to zero, the errors influence the outcomes in a way that does not average out. MC ignores the impact of the sample errors, thus leaving a bias in forecasted values.

The same effect occurs when using MC to predict market returns. Failing to account for the fact that historical data has sample error leads to optimistic bias in the predictions. While the historical mean and standard deviation can be replaced by expert estimates, this substitutes unknown human error and bias for sample error. The bias is not corrected, and the projection accuracy is most likely degraded. A much better approach is to replace MC with an unbiased estimator (UE) that appropriately characterizes sample error and corrects the bias. The UE is an analytical approach (i.e., direct equations) rather than simulation. The UE estimates the distribution of future returns from the historical mean and standard deviation in a manner that accounts for potential sample error and eliminates bias.

Case studies

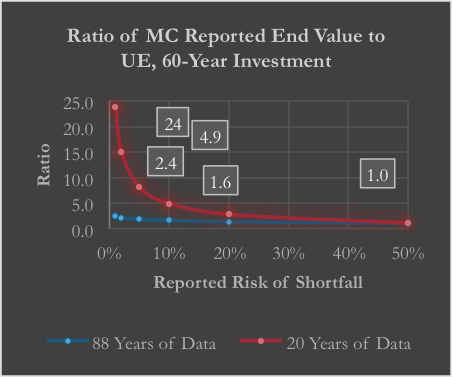

Investors between the ages of 20 and 45 invest for 60 years or more. Figure 1 shows the ratio of 60-year end-value predictions between MC and a UE using a 60% stock, 40% bond portfolio. Results are given for two sets of historical data: 20 years (red line) and 88 years (blue line).

Consider the Garcias, a couple who are both 30 years old. They would like to know how much to invest now to produce an income of $50,000 in today’s dollars by the year they turn 90, with 10% risk of shortfall. MC suggests investing $4,100 to reach their goal. In reality, if their advisor uses funds in existence for 20 years, they would need to invest 4.9-times more, or $20,100, as shown in Figure 1. If the advisor uses long-term indices that have 88 years of data, the biases are less, but still significant. The proper investment amount is 60% larger than MC recommends, or $6,600 instead of $4,100.

Figure 1

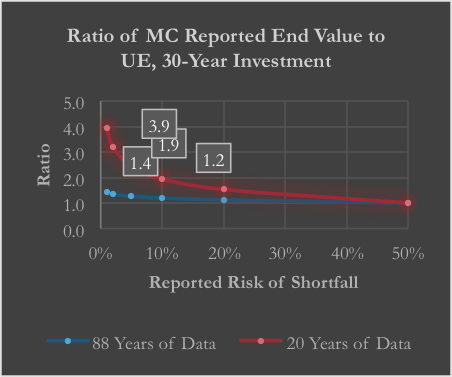

Investors between the ages of 35 and 75 will often invest for 30 years or more. The Smiths are both aged 60 and plan to invest with the same characteristics and goals as the Garcias, except their time span is 30 years instead of 60. They intend to liquidate the portfolio for income to be utilized in the year they reach age 90. Their advisor suggests a portfolio of funds with 20 years of data, and his MC program projects that a $19,000 investment will achieve an income of $50,000 with 10% risk of shortfall. However, from Figure 2, MC overestimates the end value by 1.9 times. The Smiths need an initial investment of $36,100, a 90% increase over the $19,000 MC prediction.

If the advisor instead recommends a similar portfolio with 88 years of data, the required investment is $22,800 rather than $19,000, and the Smiths need to boost their savings by 20%. As with the Garcias, more data lessens the bias. Furthermore, compared to the Garcias, the MC risk projections for the Smiths are not as severely understated, implying that a shorter investment duration lessens the bias.

Figure 2

For both 30-year and 60-year investments, a final factor is seen by examining various levels of risk. The magnitude of the bias is far greater at lower levels of risk. Figure 1 shows that for very conservative investors investing in 20-year-old funds, MC will underestimate the amount to be saved by 24 times. Sadly, the most conservative investors with the most critical needs are the most poorly served by MC.

In summary, MC’s inherent optimistic bias causes it to underestimate the amount that a client should save by 24 times or more for the most critical long-term needs. The bias in MC is due to its inability to handle sample error in the input assumptions, even when the inputs themselves are unbiased. Three factors increase the magnitude of the MC bias: longer investment duration, fewer data samples and lower risk.

Rather than trying to adjust the input assumptions, which introduces new forms of subjective error, the bias can be eliminated by employing an unbiased estimator.

Jim Lear is a comprehensive, fee-only financial advisor and a principal of Guideway Financial, LLC, an RIA in Austin, Texas. Guideway is a member of the Alliance of Comprehensive Planners (ACP). Jim is also the owner of PortfolionPlanning.com, a financial software company that develops and licenses retirement planning solutions based on the patented Portfolion® Planning methodology. Jim spent over 15 years as an electrical engineer in the semiconductor industry, during which time he developed optimization algorithms for high-performance circuits in microprocessors and developed high-speed simulation techniques for s-domain transfer functions. He can be reached at [email protected].

Read more articles by James Lear