Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article is intended for the educated layman. It was written as part of a continuing series of articles on a variety of investment topics. To view all the articles in this series, click on “More by the same author” in the left margin.

God, grant me the serenity to accept the things I cannot change,

The courage to change the things I can,

And wisdom to know the difference!

Reinhold Niebuhr

Part 1: What is Social Responsibility, and Who Exercises It?

An apparent conundrum nestles at the core of the philosophy of investing.

For all the knotty difficulties of defining investment concepts and then drawing out their implications, nearly all systematic thinking about investing begins with just four basic and required elements: return, risk, the assemblage of interrelationships among different investments’ returns over time, and the investor’s ability to tolerate risk. The first three elements, however they are defined, are given to us by the market or, more broadly speaking, the economy. The fourth is a matter of individual circumstance and psychology. (The third may be hard to grasp and is often forgotten by the layman, but it’s why we hold a portfolio, not just a single investment; it gives rise to the potential benefit of diversification.) Whether one goes about investing as a sport or as a science, whether one plays with these four elements or assembles theoretical structures from them, one must either estimate or assume (consciously or not, explicitly or not) their future values, after which one buys, sells, or holds investments to make money or to preserve wealth.

But there are some activists who object that those who accept this philosophy of investing merely interpret the economy; the point is to change it.

The activists seem, at first glance, to have nothing in common with the traditional investors, and to inhabit a separate conceptual world.

Vocabulary

A vocabulary for talking about these two ways of addressing investments, and a framework for organizing our thinking about both at the same time, was created by the late Albert O. Hirschman, in his book Exit, Voice and Loyalty (1970).

Hirschman was an economist who is much admired by intellectuals and seldom cited by other economists.[1] His death, at the age of 97 in 2012, brought his work back to public attention, which was sustained with the publication shortly thereafter of a great, thick biography.[2] More than the typical academic economist, he led, in his youth, a life of action, but he was no swashbuckler, and afterward, he refused to talk of his experiences in the resistance during the Second World War. He spent most of his professional career in the sub-discipline of development economics, which seldom graces the business pages, and his reputation outside this field depends mostly on a number of short books and essays that he produced later in middle age.

In Exit, Voice and Loyalty, he explained that the book was inspired by his initial puzzlement over the sorry state of the railway in Nigeria, where he was a consulting economist. Major producers of goods had abandoned the railroad and were moving their products by truck. Standard thinking about free markets suggested that the railroad should either have failed altogether, or that the competition ought to have motivated it to improve its service. Yet neither happened.

Hirschman intended his book not just as an explanation for observable economic phenomena like this, where he perceived a failure of economists’ traditional thinking about competitive market forces, but also as an attempt to establish common ground between economic theory and political science. He applied his ideas not just to corporations, but also to civic associations and political parties.

And, in passing, he added that his approach added richness to the “Wall Street Rule”: that one should ditch the stocks of companies with bad prospects.[3]

This is what Hirschman called exit. Voice, another of his terms, would be continuing to own the stocks while speaking up and becoming an activist to change the issuing companies for the better.

Exit and voice, while complementary, are not mutually exclusive. For example, voice without the threat of exit might lack force and influence.

When – to continue with the case of stocks – we invest in a stock, we do so because we fancy the investment prospects of the company that issued it. If we believe that the prospects for a company are poor, then we don’t buy the stock in the first place, or, if we already own it, we sell it. We might also short the stock. (Shorting is an ancient practice of profiting from the fall of a stock; the investor borrows the stock from another owner and sells it, with the expectation that the price will fall, so that he can buy it back at a lower price and return it to the original owner.) If that’s what we do, then we are exiting.

Alternatively, we may believe that when we buy a stock, we become partial owners of the company that issued it, and usually (though not always), as owners, we nominally have a voice in and a vote on how the company is managed. If we don’t like how the company is being managed, we ostensibly have some opportunity, however small, to ask or demand that management change its practices. To seize that opportunity, to exercise that option, is voice. And we can add force to that voice with the threat to sell the stock, and exit.

Loyalty, another concept developed by Hirschman, creates conditions for the exercise of voice. Loyalty to the spirit and ideas of capitalism can explain why even someone who believes that the stock market is rigged against the common man might nonetheless continue to invest in stocks, whereas a Communist or an unhypocritical socialist would likely not invest in stocks in the first place.

What does shareholding confer?

The idea that ownership of a stock confers the right to influence management was current long before 1970, and, indeed, it was and is something of a commonplace that when you own a stock, you are a part-owner of the issuing company. But like nearly all commonplaces, it’s not strictly true at all times and in all cases, and this one doesn’t hold up to close scrutiny. Both the shareholders and the managers of the first company to issue publicly traded stock, the Dutch East India Company (in the early 1600s) would have been dumbfounded at the suggestion that the outside shareholders were actually owners of the company and were entitled to a say in how its affairs were managed.[4]

Then again, and although there are some these days who work themselves into a lather at the suggestion that any voting system other than “one person, one vote” might be democratic and fair, there were, in the early years of the United States, some corporations set up in such a way that holders of fewer shares actually had greater per-share voting power than holders of more shares, because this seemed more just. [5] (The use of this structure gradually fell away during the nineteenth century.)

Even today, stockholders don’t have equal rights per share owned. Anyone who attends an annual meeting of the New York Times Company or Facebook or Ford with the expectation of voting for a change in corporate policy will meet with disappointment. Those are three examples of companies that issue two classes of shares. If your name isn’t Sulzberger or Zuckerberg or Ford, yours can never be more than a soft, muffled voice, no matter how many shares you own. Exit is the only option. This is because the controlling families don’t simply own more shares than anyone else; they own special shares that confer superior control over their companies. (These are usually called “Class A shares” and “Class B shares,” but there’s no rule that says which letter designates the class that has greater rights.)

What share-ownership confers is defined by law, not by a popular understanding of ownership. (Financial economists now regard a publicly-traded stock as more akin to a very long-term option than to a share of ownership of a company. If this doesn’t make sense to you, don’t worry; it’s of little practical importance.)

Perhaps the most important difference between an ordinary understanding of corporate ownership and what share ownership in a public company actually confers is the limiting of liability; so that, if a public company incurs massive financial losses and racks up huge debts, its shareholders merely lose all the value of their shares, and they aren’t on the hook for any of the debt, once all the assets of the company have been used to pay back the bondholders to the extent possible. The limitation of the liability of corporate shareholders required legislation in the developed countries of the nineteenth century, and it wasn’t uncontested, since this went against common notions of justice and personal accountability. [6]

This is not to say, however, that it is necessarily a mistake to want company management to think of the shareholders as owners. Warren Buffett (1930- ), for example, has famously said that he treats investors in his company, Berkshire Hathaway, as “partners,” and he prefers to invest in companies that treat their shareholders likewise:

[B]y far [the] most common…board situation is one in which a corporation has no controlling shareholder. In that case, I believe directors should behave as if there is a single absentee owner, whose long-term interest they should try to further in all proper ways. Unfortunately, “long-term” gives directors a lot of wiggle room. If they lack integrity or the ability to think independently, directors can do great violence to shareholders while still claiming to be acting in their long-term interest. But assume the board is functioning well and must deal with a management that is mediocre or worse. Directors then have the responsibility for changing that management, just as an intelligent owner would do if he were present.[7]

From what Buffett says, it follows that an investor who selects individual companies in which to invest should identify those whose boards of directors, as well as management, think of the shareholders as Buffett does, as partners. (Whether such selection would actually result in superior investment performance is another matter, which I’ve addressed elsewhere.[8])

The role of the directors is critical, because the interests of management are seldom perfectly aligned with those of the shareholders, and the directors, more than anyone else, are expected to represent the interests of the shareholders. For one thing, corporate executives want, above all, to keep their jobs. For another, they may enjoy the social and professional status that comes from building and presiding over a corporate empire, to say nothing of the merely venal interest in treating the company as if it were their own piggy bank. The executives’ first concern is shared with the stockholders, if, indeed, those executives are doing a good job at running their companies and causing the price of the companies’ stocks to rise at an appropriate rate. In contrast, building empires and drawing upon the companies’ financial resources are seldom, if ever, in the stockholders’ interest, and if so, only by accidental coincidence. Furthermore, even if a company’s directors and management choose to think of you, the shareholder, as a rightful owner of the company and as a business partner, this is not really the same as giving you an actual say in how the company is run.

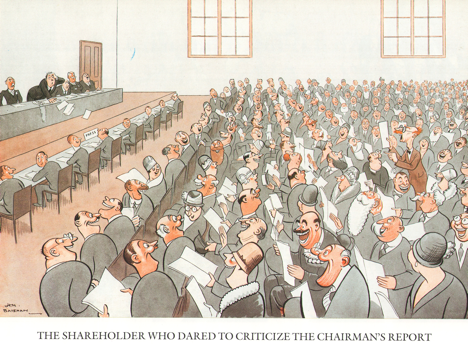

H.M. Bateman, in The Tatler

One of the most egregious recent presentations of management’s undisguised contempt for shareholders, at least at a large public corporation, was at the 2006 annual shareholders’ meeting of Home Depot, when Robert Nardelli (formerly one of Jack Welch’s lieutenants at General Electric),was chief executive officer. Here is an excerpt from the account in the Financial Times:

Only about 50 shareholders attended the meeting, in Wilmington, Delaware, more than 700 miles away from the home improvement retailer’s Atlanta headquarters. No board members were in attendance except for Bob Nardelli, chief executive, who refused to answer questions and ended the meeting after 35 minutes.

“I have never seen another annual meeting run in such an anti-shareholder manner,” says Richard Ferlauto, director of pension and benefit policy at AFSCME, a public-sector union. “In the space of half an hour, Bob Nardelli made himself the pariah of the shareholder activist community.”

Mr Nardelli was a ripe target even before last week’s meeting – his pay has been soaring during a period when Home Depot’s shares have slumped. In the almost six years since joining the company from General Electric, he has received nearly $250m in compensation, including stock options. Over the same period, the company’s shares have fallen 12 per cent, compared with a near-tripling in those of Lowe’s, its biggest rival.

Last year, Mr Nardelli’s pay was more than double that of Lee Scott, chief executive of Wal-Mart, and almost four times greater than his counterpart at Lowe’s…

Activists were furious that no directors except Mr Nardelli were in Wilmington to hear their complaints. It is highly unusual for a company’s board to miss an annual meeting.

Rattled by the outcry, Home Depot later issued a statement saying its “departure from past practice should in no way be construed as either a lack of respect for our shareholders or a lessening of our commitment to high standards in corporate governance and transparency”.[9]

This case was striking, but more to the point, company performance was so poor under Nardelli, that he was soon out of a job. (It’s Ok; you can dry your tears. After a brief spell at a private equity firm, he was elevated to chairman of Chrysler.)

Owners, managers, and stakeholders

The theoretical consequences of owners and managers having different interests are the subject of an entire field of economics, principal-agent theory, which, although ostensibly addressing practical applications, such as how to design pay structures for executives in order best to align their incentives with the interests of shareholders, quickly became more than a little abstruse, and has had little practical influence, apart from providing convenient excuses for the consultants who are brought in by corporate boards to design executive compensation packages.

To some small degree, the little shareholders do have one way to talk back to the self-interested or the merely misguided managers of corporations: through their tribunes or representatives (so to speak), that is, the portfolio managers of their mutual funds and institutional pensions. Even if these portfolio managers cannot (as I have argued, most of them usually cannot) beat their benchmarks for investment performance, still, the more diligent and perspicacious among them serve the public interest by turning up at the meetings and conference calls where the corporate executives regularly report on their firms’ past performance and plans for the future, and the challenges that their companies face. The executives’ purpose is to persuade the portfolio managers that the firms’ futures are bright, or at least not as bad as they might otherwise seem. But the best portfolio managers pester them with probing questions and bluntly suggest what the executives ought to do to make their stock more valuable. The portfolio managers are not intentionally serving the public interest, of course. In some cases, they may just be explaining to the executives why they’re not buying the stock. In other cases, they may have already bought the stock because they think that the executives will ultimately do what ought to be done, and then the stock’s price will shoot up, accordingly. But regardless, the public interest is served when these portfolio managers and analysts hold the executives to account. Whether the executives heed them is another matter. The institutional money managers’ intervention, though it does remind corporate executives of the shareholders’ interest in a way that they can’t dismiss outright, nonetheless is little more than voice, and a little less than influence.

The portfolio managers who intercede in this way have one concern only: the value of the corporations’ stocks. And the executives, even when their actions tell us otherwise, almost always claim that their interest is the same, and that they know better than the portfolio managers and analysts how to increase that value. But not everyone believes that the sole aim of corporate managers ought, in principle, to be making stocks as valuable as (legally) possible.

There are entire countries with modern, functional economies whose corporate cultures regard others besides the shareholders as stakeholders, who have a legitimate interest in the results of corporate behavior. Germany, for example, enshrines this in law. As Thomas Piketty writes:

Suffice it to say that the lower market values of German firms appear to reflect the character of what is sometimes called “Rhenish capitalism” or the “stakeholder model,” that is, an economic model in which firms are owned not only by shareholders but also by certain other interested parties known as “stakeholders,” starting with representatives of the firms’ workers (who sit on the boards of directors of German firms not merely in a consultative capacity but as active participants in deliberations, even though they may not be shareholders) as well as representatives of regional governments, consumers’ associations, environmental groups, and so on. The point here is not to idealize this model of shared ownership, which has its limits, but simply to note that it can be at least as efficient economically as Anglo-Saxon market capitalism or “the shareholder model” (in which all power lies in theory with shareholders, although in practice things are always more complex), and to observe that the stakeholder model inevitably implies a lower market valuation but not necessarily a lower social valuation.[10]

The stakeholder concept from time to time gets an airing elsewhere. Great Britain, which other countries often bracket with the United States as sharing the “Anglo-Saxon” corporate culture, was, before Mrs. Thatcher became prime minister in 1979, considerably more social-democratic than it is now or the U.S. ever was. Yet when the 1977 “Bullock Report” of the Committee of Enquiry on Industrial Democracy, sponsored by the Labour government, recommended the inclusion of worker representatives on the boards of large corporations, the proposal issued stillborn.

Even in the United States, General Motors has had a union representative on its board since 2014, as compensation to the workers for the concessions they made as part of the company’s restructuring during its bankruptcy in the Great Recession, but such union representation is extremely rare in this country.

So, while the shareholders’ interest is, almost inevitably, the value of their stock, and corporate executives agree, in principle, that this is as it ought to be, the politico-economic presuppositions of a society or country, especially as expressed by its legal system, may determine that management has additional obligations that may lessen that value.

What is a manager to do?

Milton Friedman (1912-2006), perhaps more than any other economist, developed the intellectual grounding for the idea that the only social obligation of corporate boards and management ought to be the maximizing of shareholder value. He expressed this idea at least as early as 1962, in his book Capitalism and Freedom; by 1970, he was a celebrity economist, and he popularized this view in an oft-cited essay in the New York Times.[11] He accepted as axiomatic that shareholders are, indeed, the owners of a corporation – an assumption that, I showed above, is neither legally unambiguous nor historically accurate – and therefore the employers of the corporate executives. From this, he argued further:

What does it mean to say that the corporate executive has a "social responsibility" in his capacity as businessman? If this statement is not pure rhetoric, it must mean that he is to act in some way that is not in the interest of his employers. For example, that he is to refrain from increasing the price of the product in order to contribute to the social objective of preventing inflation, even though a price increase would be in the best interests of the corporation. Or that he is to make expenditures on reducing pollution beyond the amount that is in the best interests of the corporation or that is required by law in order to contribute to the social objective of improving the environment. Or that, at the expense of corporate profits, he is to hire "hardcore" unemployed instead of better qualified available workmen to contribute to the social objective of reducing poverty.

In each of these cases, the corporate executive would be spending someone else's money for a general social interest. Insofar as his actions in accord with his "social responsibility" reduce returns to stockholders, he is spending their money. Insofar as his actions raise the price to customers, he is spending the customers' money. Insofar as his actions lower the wages of some employees, he is spending their money.

The stockholders or the customers or the employees could separately spend their own money on the particular action if they wished to do so. The executive is exercising a distinct "social responsibility," rather than serving as an agent of the stockholders or the customers or the employees, only if he spends the money in a different way than they would have spent it.

But if he does this, he is in effect imposing taxes, on the one hand, and deciding how the tax proceeds shall be spent, on the other.

Friedman goes on to argue that corporations cannot be deemed to have responsibilities, because they are not persons except in a narrow, technical, legal sense, and only persons can have responsibilities. If, he argues, the shareholders have in mind other social responsibilities, they could, as individuals, spend their private funds, which they may even have earned through share ownership, in support of those purposes.

It is safe to say that had Friedman written his opinion piece a few years later, he would very likely have recast his argument to take account of the complications introduced by principal-agent theory, which did not yet exist, and yet the direction and conclusion of the argument would have remained the same.[12]

Nova et vetera

Friedman’s conclusion, that the business of a business is making money for its shareholders, is the ultimate outcome of a revolution in economic thinking that took off in the eighteenth century, with the rise of modern capitalism and the industrial revolution. Samuel Johnson (1709-1784) best encapsulated the nascent attitude toward business with his assertion that “There are few ways in which a man can be more innocently employed than in getting money.”[13] While this may strike a present-day reader as simultaneously naïve and passé, in light of the bad behavior by corporations that has been documented from the nineteenth century to the present, Dr. Johnson was actually very modern in outlook. His apothegm overturns the ancient Christian notion that “Radix malorum est cupiditas,” [14] which held through the Middle Ages and into the early modern era. (Not that Dr. Johnson was not a devout Christian.) This pre-modern notion has not entirely vanished among the more pious, and it still manifests itself sometimes as anti-capitalism, sometimes as the dissolution or abjuration of private wealth, and sometimes as both. To the extent it persists, it’s not held exclusively by lefties. Even the very conservative businessman Tom Monaghan (1937- ), the founder of Domino’s Pizza and a devout Roman Catholic, holds this older view, but he limits his expression of it to the expenditure of his personal wealth, which he is spending down on charitable and religious causes dear to him, often related to the Church, and he has forsaken the ostentatious trappings and possessions of the plutocrat. He most definitely did not run his business, when he ran it, as if it had larger social responsibilities.

But this is today very much a minority attitude, and those who hold it perforce have little influence on the larger economy. The religious question of obligations incurred by wealth and money has so far receded that even a recent mainstream textbook on Christian theology entirely neglects it,[15] and charity has become a secular value.

Friedman’s Times article appeared when there was ferment in ideas about corporate governance. This was when Hirschman published his book. And it was also about this time that Michael Jensen (1939- ), a financial economist then at the University of Rochester and later at the Harvard Business School, took Friedman’s argument one giant step further. After consideration of the principal-agent problem – he was among those who first developed principle-agent theory – and concluding that the interests of shareholders, whose control was diffuse, and the interests of managers could not be properly aligned, he provided the intellectual foundation for what became the leveraged buyout (LBO) boom of the 1980s, which, when it revived in the 2000s, was rebranded as private equity. This is a matter of a few owners using both debt and capital to buy up publicly-held companies to gain control and to take them private (meaning that their shares no longer trade in the public markets). The new owners, being very concentrated, then have direct control of the managers, and often themselves become the managers, and they rearrange the companies to make them more profitable – at least in theory. It’s not really that simple. In order to raise capital to execute the buyout, the buyout specialists establish different classes of ownership – sound familiar? – of which there are general partners and limited partners. The general partners are the ones who take command, the ones who actually work at the private equity firms. The much more numerous limited partners are the others who put up capital in the hope of earning a good return, but they don’t exercise control. In general, more of the returns accrue to the general partners, who, after all, are doing most of the work. Also, in order for the general partners to be able to rely on their sources of capital, they usually specify “lock-up” periods of several years, during which the limited partners can’t withdraw their contributions. In short, the limited partners are in the worst possible position: They have little voice and no possibility of exit.[16]

Still, ostensibly, by concentrating ownership, private equity firms ought to be better able than the shareholders of publicly-traded companies to direct management to increase corporate value. And indeed, there is some evidence that privately-held companies are less driven by quarterly results than publicly-held companies are. That is, they are less subject to what is popularly decried by populist left-wing politicians and journalists as “short-termism” (and more drily by economists as the use of too-high discount rates).[17]

By 1993, Jensen was able, after poring over the data, to make the empirical case that activist investors, through the markets for corporate control, whether public or private, were able, in aggregate, to boost the value of corporations by eliminating wasteful activity and increasing efficiency, and that the LBO boom of the 1980s was therefore, on the whole, beneficial to the U.S. economy.[18] But he did not evaluate the returns earned by shareholders of the different classes.

LBOs were not the only sort of corporate restructuring in the 1980s. This was also the beginning of the era of hostile takeovers of corporations by other public corporations. And because these were hostile (to the existing management), the managers of the target corporations (and the lawyers who advised them) devised means of entrenching themselves and their ways of conducting business, against the interests of their shareholders, who stood to earn considerable returns from the takeovers. In doing so, they would enlist the support of workers, who feared losing their jobs, and those sentimental members of the public – including shareholders – who are discomfited by a dynamic economy, and prefer that the world remain, in Robert Burton’s phrase, “the same still; still, still the same, the same.” Unquestionably, some of these takeovers were farcical and disastrous, but economists mostly agree that, on the whole, they benefited both shareholders and the nation’s economy.[19]

Two schools of thought on corporate responsibility

One undeniable virtue of the argument propounded by Friedman is that it is uncomplicated. It is clear. And in making his case so vigorously and lucidly, he forced proponents of more expansive views of the purposes of the corporate governance to develop their ideas further. At the same time, those who agree with Friedman have reformulated his argument in terms of principal-agent theory, suggesting that when a company concerns itself with corporate social responsibility (CSR), this reflects management’s pursuit of its own (social) interests at the expense of shareholders. The result is that since his time, there have been two schools of thought on this matter, with one or the other gaining the upper hand, depending upon how one reads the business press and interprets current events.[20] Since the 2008-2009 financial crisis, there is a general sense that the value-first school has lost ground to the school advocating broader corporate responsibility.

One significant drawback to the case for broader corporate social responsibility is that it is very difficult to say concisely what corporate social responsibility actually is, if it isn’t just making money for the shareholders. Friedman made precisely this point in his essay, when he complained, “The discussions of the ‘social responsibilities of business’ are notable for their analytical looseness and lack of rigor.”

And he wasn’t the only one to point up this deficiency in arguments for corporate social responsibility. Even advocates of the broader approach recognize this. A recent short book entitled Corporate Social Responsibility says:

Numerous definitions of CSR are offered by academics and commentators, and by business, civil society, governmental and consulting organizations. Overall, the definitions capture the following key features:

- business responsibility to society (i.e. being accountable)

- business responsibility for society (i.e. in compensating for negative impacts and contributing to social welfare;

- business responsible conduct (i.e. the business needs to be operated ethically, responsibly, and sustainably);

- business responsibility to and for society in broad terms (i.e. including environmental issues); and

- the management by business of its relationships with society

Nevertheless, CSR can be difficult to pin down.[21] [Italics added]

Not least of CSR’s definitional problems is that its practice cannot be neatly disentangled from the pursuit of shareholder value (as Friedman acknowledged when he qualified his objection with the words, “Insofar as his actions … reduce returns to stockholders”). Some corporate activities that have the outward appearance of fulfilling social responsibility, like the sponsorship of a charitable event or the local public radio station, can do double duty as advertising and good public relations. These might thereby help smooth the way when the company wants a favor from government, like a zoning variance, or is trying to avoid a costly restriction, like product regulation. Generous corporate subventions of civic organizations may suborn otherwise inquisitive journalists and politicians and help to evade unwanted scrutiny. Corporations have understood, since the nineteenth century, that paternalistic treatment of their workers can discourage unionization, which may impose even greater costs than the benefits provided to the workers at a company’s volition. (With the steep decline in union membership, present-day corporations have less economic incentive to be paternalistic.) Such socially-responsible corporate actions ought not to be superciliously written off as merely self-interested. For who among us, in making charitable contributions or volunteering time to public service organizations, is without an admixture of self-interest among his motives, from the Zegna-draped board member of the Metropolitan Opera, photographed for the society pages, to the contributor to the church bake sale hoping to win kudos for his cheesecake, to the telephone responder at the public television pledge drive hoping to score a date? And the U.S. tax code rewards individuals and corporations alike for exercising charity. Society is little worse for such mixed motives.

Corporate social responsibility even in the most expansive view is not, however, all-encompassing. The expression does not normally, although it could, include job preservation for workers (and management) and the maintenance of corporate stasis, as in the “stakeholder model.” Yet it does recognize stakeholders other than shareholders. For example, you might find proponents of corporate social responsibility expressing concern about coal miners’ safety and the environmental damage caused by coal mining – if they held coal stocks, which they don’t – but you wouldn’t find them opposing alternative energy sources and power plant conversions out of fear of large-scale unemployment in Appalachia. There is also an honest difference of opinion on whether tax avoidance should be considered socially irresponsible. Curiously, it seems that corporations that rank more highly on measures of social responsibility are also more energetic in avoiding taxes.[22] (Remember that “avoidance” is legal; “evasion” is illegal.) These limitations on the definition of corporate social responsibility may matter when we come to consider the investment performance of companies that express social responsibility.

Seeing the two opposing ideologies of corporate social responsibility, and perhaps teetering on the edge of a chasm of anomie, the interested shareholder may be asking, “What is to be done?” If he or she wants to take advantage of share ownership to effect change in society, or even, passively, to let personal ethical values guide the choice of investments in order not to earn “blood money,” how can either be done when the collective of shareholders has so little influence on corporations, and there are no universally agreed standards for guiding the governance and management of corporations?

Two responses

The 1980s, a decade that saw a recrudescence of Wall Street culture under the vision statement that “Greed is good,” also saw two complementary answers to this question, both of which were amplifications of voice. One was the creation of institutions for improving corporate governance, the most prominent of which was Institutional Shareholders Services (ISS), founded by the investment activists Robert A.G. Monks (1933- ), a consummate corporate insider, and Nell Minow (who is also a film critic and a daughter of Newton Minow, the former chairman of the Federal Communications Commission, famous for his 1961 description of bad television as a “vast wasteland”). ISS is a corporation that consults to and advises investment institutions on how best to address issues of corporate governance in the companies in their portfolios.[23] The renewed focus on corporate governance was partly a reaction to the contemporaneous use of new means to entrench management in the face of hostile takeovers, mentioned above. Michael Jensen would not regard this answer as irrelevant to the pursuit of increasing corporate value. And there is some evidence that this response has been fruitful. Eugene Fama (1939- ), one of the founders of the theory of efficient markets, has gone so far as to say that activism in the pursuit of better corporate governance is an “obligation” and will lead to better corporate performance.[24]

But we are more interested here in the other, rather paradoxical answer, the populist movement toward socially responsible investing (SRI, also known in the UK as “ethical investing”). Anyone pursuing this answer faces a nearly overwhelming challenge: If managers can’t easily be persuaded even to make as much money as possible for their shareholders, how much more difficult must it be to persuade them to assume corporate social responsibility?

The origins of socially responsible investing

The full history of socially responsible investing has yet to be written, so much of what I write here is my surmise about its development.

The idea of corporate social responsibility took root long ago. We have already looked at the established German culture of favoring stakeholders, and, of course, Friedman in 1970 was reacting against advocates of the existing idea. Socially responsible investing, too, has a long prehistory, interwoven with but different from the history of the idea of corporate social responsibility, and during which investors chose not to invest in the stocks of companies to whose products and practices they had ethical or religious objections. For example, the First Church of Christ Scientist has long not invested and still does not invest its endowment in the stocks of pharmaceutical companies. And this is not the only case of religion determining which stocks to avoid; there is also the comparatively recent Ave Maria family of mutual funds (begun at the instigation of Tom Monaghan and advised by, among others, Phyllis Schlafly), which is guided by conservative Roman Catholic principles, and engages in what the advisor firm calls “Morally Responsible Investing” (MRI), and therefore won’t invest in companies that produce abortifacients or use embryonic stem cells, or even that make contributions to Planned Parenthood.(These funds also won’t buy the stocks of hotel chains that offer adult films on pay-per-view, but they will invest in weapons manufacturers.)[25] But it was in the 1980s, I believe, that the idea arose of an identifiable systematic practice identified by name as “socially responsible investing,” as activists were contemplating how to apply economic pressure to large corporations in order to achieve social ends.

My guess is that many of these social activists were aware of the tradition of infusing religious morality into investing. (In its early years, the Social Investment Forum of Boston convened at the offices of the Unitarian Universalist Association.) At the same time, the more astute among them also pondered the history of political and social movements applying economic pressure through boycotts, and the imposition, through legislatures, of governmental regulation and of tariffs and bans on the products of foreign companies. But boycotts would not work with large corporations whose products could not practically be forgone by consumers, like the gasoline producers, or whose products were bought mainly by other corporations, not consumers, like the manufacturers of industrial machinery. The social activists realized that they could take a leaf out of the playbook of the professional investment managers and, though they, themselves, were unlikely to have sufficient wealth to exercise voice through the threat of selling shares or refusing to buy them, they could amplify their voice through the endowment funds and pension funds of organizations in which they had some say.

The first big test of this tactic was the movement for divestment from companies doing business in South Africa, in order to pressure the apartheid regime.[26] Opposition to South Africa’s apartheid regime, even in the U.S., stretched back to its origin in 1948, when the white minority government codified the system through legislation.

Gradually, American opposition organized, and in the 1970s, the Interfaith Council on Corporate Responsibility (ICCR), which had been working with and against American corporations doing business in South Africa, recruited the Reverend Leon Sullivan (1922-2001), a rare combination, especially for his time, of civil rights worker, with a church in Philadelphia, and activist investor. In March 1977, Sullivan, in coordination with the Department of State under newly-elected President Jimmy Carter, announced what became known as the “Sullivan Principles” for American corporations doing business in South Africa. Even at the time, they seemed uncontroversial. The first three were:[27]

- Nonsegregation of races in all eating, comfort, locker rooms, and work facilities.

- Equal and fair employment practices for all employees.

- Equal pay for all employees doing equal or comparable work for the same period of time.

In the course of the year, Sullivan persuaded a number of companies to sign on: American Cyanamid, Burroughs, Caltex, Citicorp, Ford, General Motors, IBM, International Harvester, 3M, Otis Elevator, and Union Carbide.

The idea that activism against apartheid should be limited to inducing companies to subscribe to and abide by these principles seemed inadequate to many anti-apartheid activists, even the ICCR, which monitored and reported on compliance with them (and to whose reports the investment management profession looked for guidance[28]). Contemporaneous with the pressure for corporations to adopt the Sullivan Principles was the movement to force large investors, namely pension funds and endowments, to divest themselves altogether of the stocks of companies doing business in South Africa. By 1986, reliance on voice seemed too little, with no discernable effect, and Sullivan threw in the towel; he called a press conference to announce that he supported total U.S. corporate divestment from South Africa, the breaking of diplomatic ties, and a U.S. trade embargo.[29] That is, exit and slamming the door. Some American authorities, like Chester A. Crocker (1941- ), Assistant Secretary of State for African Affairs under President Reagan, either because they actually believed that the paternalistic case they were making carried force or because they weren’t especially bothered by apartheid – Crocker was married to a white Rhodesian – argued against disengagement from South Africa on the grounds that it would hurt black workers, who would be thrown out of their jobs, and instead for what they called “constructive engagement.” That corporate disengagement from South Africa would have caused black unemployment is indisputable, but against this should be weighed the statements of South African anti-apartheid leaders, like Archbishop Desmond Tutu, who argued, even when it was illegal in South Africa to do so, that total economic disengagement was necessary to force change upon the white minority government. In 1992, President F.W. De Klerk entered into negotiations with Nelson Mandela, and in 1994, South Africa for the first time elected a government of the majority.

I’ll return to the case of South African divestment in Part 2 of this essay, when I consider the effectiveness of socially responsible investing.

Movements for divestment have continued, in order to punish foreign governments for violations of human rights and to motivate reform, with calls at various intervals to apply the practice to companies doing business in Northern Ireland, Myanmar (Burma), and into the present, Israel (for which yet another literal triplet has been devised, BDS, for Boycott, Divest, and Sanction). The names have changed as the political regimes in the countries or regions have changed. But there seems to be a certain amount of ethical fashion, rather than systematic analysis, in the choice of polities to target. Why, for example, Myanmar, and not also the many oriental despotisms of the Middle East? (Because the latter tend to build their economies on the export more of petroleum than of figs and dates, they now have become indirect targets of the efforts to divest from companies that produce fossil fuels.) To be fair, though: The investment professionals at large firms that specialize in SRI portfolios tend to be better informed and more systematic than the activists who divert the news media.

The 1980s saw not just the rise of the particular investment strategy of divestment in support of human rights. SRI at the same time encompassed the selection or rejection of stocks for portfolios in order to encourage or coerce corporations to assume other social responsibilities, while often relegating to secondary consideration their return on investment (or, as the advocates often argue, their short –term return on investment). The broader criteria of social responsibility came to include, notably, matters pertaining to the environment and environmental sustainability.

This was when there first appeared portfolio management companies dedicated to SRI, many of them in Boston, including the first, Trillium Asset Management (originally Franklin Research & Development), Winslow Management Company (now absorbed into Brown Advisory Investment Group), the old U.S. Trust of Boston (which has since disappeared into a larger corporation, and should not be confused with U.S. Trust of New York, now a division of Bank of America), and Kinder, Lydenberg, and Domini (also vanished), which concerned itself primarily with the portfolios of individuals, not institutions.

Institutional structures to support and further SRI also appeared during that decade, including the Social Investment Forum and the Ceres organization, which promulgated the Ceres Principles (see Appendix A of Part 2) for sustainability and the environment. The Ceres Principles were later complemented by the Global Sullivan Principles (see Appendix B of Part 2), concerning the role of employees, a generalization of the original Sullivan Principles, and which were set forth by Sullivan a couple of years before his death.

In the succeeding decades, the practice has grown and spread, around this country and abroad. London, being a center of international investment management, is also the world’s center for the practice of SRI.

What is socially responsible investing?

Almost from inception, SRI, like the corporate social responsibility that it supports, has not had one clear definition, as even its practitioners acknowledge. The preferred expansion of “SRI” is now “Sustainable, Responsible, and Impact” investing, two adjectives and a noun. As the Social Investment Forum says, “Depending on their emphasis, investors [define SRI] as: ‘community investing,’ ‘ethical investing,’ ‘green investing,’ ‘impact investing,’ ‘mission-related investing,’ ‘responsible investing,’ ‘socially responsible investing,’ ‘sustainable investing’ and ‘values-based investing,’ among others.” Increasingly, at least within the investment management profession, “SRI,” as a term, is being superseded by the abbreviation “ESG,” which stands for “Environmental, Social, and [corporate] Governance” investing. I can’t satisfy everyone, and for simplicity, I will continue to use the expression “socially responsible investing” over the course of this essay, except when the more expansive “ESG” is clearly more fitting. Please interpret it in the broadest sense.

This isn’t just a semantic problem, but a practical one, too. As I will discuss in the last section of this essay (in Part 2), an investor who wants to invest her funds in a socially responsible fashion has to evaluate prospective investment managers not just on their fees and their investment results, but also on their purposes with respect to social responsibility, and then she has to confirm that the managers’ practices conform to their stated purposes. It’s also entirely possible that the investor will not be able to find an investment manager who, as a matter of course, is already managing funds in a way that matches the investor’s purpose.

When SRI began, investment management companies were constructing stock portfolios customized to their clients’ preferences. There soon followed SRI stock mutual funds, usually managed by firms that made a specialty of this sort of investing, and available to smaller and individual investors. There are also now a few SRI exchange-traded funds (ETFs).

Within the broad scope of ESG investing, there are further alternatives for individual and institutional investors, not just in the social concerns that are addressed, but in the means by which these are addressed. Originally, ESG investing encompassed publicly traded stocks. Bonds were barely even a secondary concern, and in the 1980s, few investors in the U.S. held the sovereign debt of any other countries, let alone countries with despicable governments. Now, however, one option for investors is “green bonds,” which the World Bank (one of their issuers) defines as being “issued to raise capital specifically to support climate-related or environmental projects.” Of course, no one would or should construct a bond portfolio entirely from green bonds, but they offer a way to give a positive environmental bias to a portfolio, which can’t be achieved simply by avoidance of bonds that finance undesirable or unsavory companies and governments. Green bonds have yet to achieve much popularity in the U.S., but institutional investors abroad have embraced them, and even China, not heretofore distinguished by a concern for sustainability, is getting into the act.[30]

Another option for the socially concerned investor is “impact investing,” whose definition is hard to pin down.[31] Depending upon the speaker, the meaning can range from a synonym for the original socially responsible investing to something of a cross between investing and philanthropy. Its proponents may claim that it will earn returns like those of the broad market, but that claim is questionable (a point to which I will return), and in any case, for those who engage in impact investing, returns are not always as important as purpose. Many of the financial vehicles for impact investing may not be available to the mass market, and for these, an investor must fit the federal government’s definition of an “accredited investor,” the qualification for investing in hedge funds, private equity, and other risky investments not subject to the same level of regulatory scrutiny as publicly-traded stocks and bonds. (The current definition of an accredited individual investor is someone who has a net worth of at least $1,000,000 in financial assets, had an annual income of more than $200,000 in each of the last two years, and is expecting at least the same income in the current year. Congress, in its continuing bipartisan effort to remove legal protections for investors, is attempting to relax these restrictions, though it may also index these numbers to the rate of inflation, which would actually be an improvement.) But this is big business. For example, in April 2015, Bain Capital, the large private equity firm, hired Deval Patrick, the former governor of Massachusetts, to create an impact investing practice. In the words of the firm’s press release, “This new business will focus on ‘double bottom line’ investments that improve overall quality of life or that create economic opportunities in communities which are economically distressed, overlooked by investors or otherwise in need of investment capital.”[32]

Adam Jared Apt, CFA, is a financial advisor and the owner of Peabody River Asset Management, based in Cambridge, MA.

[1] Perhaps I’m being unfair. Not being an economist, I’m unfamiliar with the full range of literature that might draw upon his work; it’s possible that he’s often cited by his fellow development economists.

[4] For the early history of the sale and trading of the stock of the Dutch East India Company, see Lodewijk Petram, The World’s First Stock Exchange, trans. Lynne Richards (New York: Columbia University Press, 2014).

[5] Eric Hilt, “History of American Corporate Governance: Law, Institutions, and Politics,” in Annual Reviews of Financial Economics, Vol. 6, 2014, ed. Andrew W. Lo and Robert C. Merton (Palo Alto: Annual Reviews, 2014), p. 6; As an example of the public ire that even theoretical work on alternative voting systems may arouse, you may recall President Clinton’s dumping of his nomination of Lani Guinier in 1993 to be head of the civil rights division of the Department of Justice, in the face of strong political opposition and after, he said, he belatedly read her scholarly publications on this subject and found them objectionable.

[6] Gilbert and Sullivan popularized the Companies Act of 1862 in their operetta Utopia, Ltd. (1893), but actually most of the relevant legislation, in both the U.S. and the U.K., came earlier in the century.

[9] Andrew Ward, “Investors Feel Locked Out at Home Depot,” Financial Times, 1 June 2006.

[10] Thomas Piketty, Capital in the Twenty-First Century, trans. Arthur Goldhammer (Cambridge, Mass.: Harvard University Press, 2014), pp. 145-146. Remember also that Volkswagen is 20% owned by the state of Bavaria; we now know, if we didn’t before, that state ownership has done very little to optimize its value for shareholders.

[11] Milton Friedman, “The Social Responsibility of Business is to Increase its Profits,” New York Times, 13 September 1970.

[12] Friedman does, in passing, use the expressions “principal” and “agent”: “The whole justification for permitting the corporate executive to be selected by the stockholders is that the executive is an agent serving the interests of his principal.” Perhaps this sentence was an inspiration for the theory’s founders.

[13] You may be wondering if Dr. Johnson intended this ironically. He did not.

[14] “For the love of money is the root of all evil.” I Timothy 6:10. The full history of Christianity and its attitudes toward money is far more complex than this caricature. As I think we all know, there is no holy writ so self-consistent, no scriptural imperative so nearly absolute, that a spiritual leader cannot wring from the text whatever inference suits his purposes. In Christian antiquity and the Middle Ages, there existed wealth, of course, and its holders were inevitably influential. There were tensions between those, like Augustine, who argued that wealth should be applied to the mitigation of poverty and the support of the Church, thereby expiating sin, and radicals like Pelagius, who argued that wealth must be simply and totally renounced as in itself evil. These early Christian attitudes toward wealth overturned the opinion of classical antiquity, that the rich man was obliged to contribute to the well-being of his city. Julius Caesar, for example, in Shakespeare’s words, “hath left you [Romans] all his walks, his private arbours and new-planted orchards, on this side Tiber. He hath left them you and to your heirs forever – common pleasures, to walk abroad and recreate yourselves.” See Peter Brown, Through the Eye of the Needle: Wealth, the Fall of Rome, and the Making of Christianity in the West, 350-550 AD (Princeton: Princeton University Press, 2012), p. 308-321, and The Ransom of the Soul: Afterlife and Wealth in Early Western Christianity (Cambridge, Harvard University Press, 2015), passim.

[18] Justin Fox, The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall Street (New York: HarperCollins Publishers, 2009), pp., and Michael C. Jensen, “The Modern Industrial Revolution, Exit, and the Failure of Internal Control Systems: Presidential Address to the American Finance Association,” Journal of Finance, July 1993, pp. 831-880.

[19] For an overview of LBOs and other hostile takeovers, especially in the 1980s, and their economic results, see Gregg A. Jarrell, “Takeovers and Leveraged Buyouts,” in The Concise Encyclopedia of Economics, David Henderson, ed. (Indianapolis: Liberty Fund, Inc., 2008).

[23] In the marketplace for such services, ISS has been joined in the present century by the firm Glass Lewis.

[25] Beverly Goodman, “Keeping the Faith,” Barron’s, 6 July 2015, p. 33.

[28] The reports were prepared under contract to the ICCR by the long-established corporate consulting firm Arthur D. Little, Inc. (which imploded in 2002 following the bursting of the dotcom and telecom bubble).

[29] Massie, op. cit., p. 638.

[31] For more on impact investing for the high-net-worth investor, see “Impact Investing: How to Do It Right,” a special “Penta” supplement to Barron’s, 30 November 2015.

Read more articles by Adam Jared Apt