Ladies and gentlemen of the jury, we are here today to consider the case of a defendant who ought to be familiar to anyone who has watched its many advertisements on TV, or seen its iconic brands marketed in magazines and on the Web – the bull, the rock, the interlocking trapezoids that form a kind of circle with a square in the middle. It goes by many aliases, but whenever I point across the room at the defendant, I will refer to two of the defendant’s many names interchangeably: the brokerage industry, or simply Wall Street.

The defendant is charged with a number of crimes: of deliberately and systematically employing deceptive business practices; operating a cartel; deliberately (and successfully) undermining consumer protections; engaging in anti-competitive behavior against the emergent financial advisory profession; exerting undue and improper influence on Congress and the regulators; raking in excess profits and thereby harming the American economy that it originally was created to benefit.

I will ask you to find it guilty of acting as a detriment to society itself. And at the end, I will propose a penalty, should you find the brokerage industry guilty of these various acts of creative mischief based on the evidence I am about to present.

As we consider this evidence, I will ask you to suspend much of what you think you know about this defendant. Month in, month out, the financial services trade press launches articles detailing the lobbying battles between advisors and the large Wall Street brokerage houses, about fiduciary versus sales-related suitability standards and manifest customer confusion about regulatory oversight and the misleading titles (financial advisor, investment advisor, vice president of investments) their sales reps put on their business cards. We read about shifts in market share, Financial Industry Regulatory Authority (FINRA) efforts to take over regulation of advisors, and “harmonized” regulation.

These articles give the impression that two parties – the advisory profession and Wall Street – are roughly equal parties simply engaged in a battle for market share. They leave us with the false impression that the brokerage industry is nothing more than a competitor in the economic landscape.

Ladies and gentlemen of the jury, I hope to convince you that all of these individual skirmishes between Wall Street and the emergent advisory profession are part of a much bigger picture that must now be exposed.

I intend to make the case that the large brokerage firms are blocking – in the financial services world – the consumer revolution that has long since swept through the rest of the American economy. I will show that the defendant’s attempt to strangle the emergent advisory profession in its cradle is part of a much larger effort to stifle evolutionary impulses which have created price competition and broader choice for consumers in virtually all other sectors, from the decline of the large retail brands (Sears, Woolworth, Montgomery Ward etc.) in the late 1900s to the more recent broadened consumer access to competitively-priced products and services provided through the Internet.

At the same time, I hope to show that an industry that ought to be functioning like a public utility – aggregating capital so it can be allocated where it is needed in the U.S. economy – is actually shuttling money where it will benefit Wall Street the most, creating financial instruments that exist purely to serve Wall Street’s profit margins, placing itself aggressively between investors and entrepreneurs so that it can exact tolls over and over again whenever money flows, siphoning an alarming percentage of the all the profits of all corporations into its bonus pools while providing, in many cases, nothing productive or beneficial in return.

I hope to show that today’s defendant functions like a cartel. Ladies and gentlemen of the jury, I hope that at the end of our proceedings, you will agree with my premise that if these activities were conducted anywhere else in our economic system, they would be considered illegal and predatory.

I also hope show that the scope of this enterprise is enormous, and so, too, is the scale of the achievement. You will see that Wall Street spends many orders of magnitude more than consumer advocates on Congressional campaigns and lobbyists. It exerts so much influence on regulators that we can plausibly talk about regulatory capture by the industry – or, as you will see in the case of FINRA, direct control of its board of governors. At the same time, the industry exerts a remarkable degree of influence on the U.S. presidency itself.

Our proceedings today will provide you with a big picture review of an industry’s largely successful effort to maintain the ability to benefit itself at the expense of competitors, consumers and the American economy.

I call it The Case against Wall Street.

IPO cartel

In the lobbying debate, it is sometimes forgotten that there are three sides to the Wall Street industry – and Wall Street lobbyists use this to their great advantage. They ask with a hint of incredulity in their voices how the dreaded fiduciary standard can be applied to brokerage firms because this would then extend to their IPO sales activities. They would be forced to benefit their retail investment customers rather than the companies for which they’re raising capital. On the second side, they would no longer be able to sell creative pooled investments and derivatives under the “buyer beware” standards that apply to retail manufactured products.

And on the third side, when Wall Street firms are trading for their own accounts, they ask whether their professional traders and flash boys should be required to make trades that benefit the counterparties in their transactions. Preposterous! After all, we don’t require day traders or lay investors to adhere to a fiduciary standard when they buy and sell securities

Ladies and gentlemen of the jury, let’s first of all be clear. No lobbyist for the emergent advisory profession has ever proposed that fiduciary standards, or even standards of plain decency, be applied to any part of Wall Street other than its retail-facing brokers. Trying to apply consumer protections to the other Wall Street activities is purely a straw man for brokerage lobbyists to trot out at their convenience.

But as I build my case, let’s take a moment to delve into the alleged value that Wall Street provides the economy with these activities, and see whether there’s a strong case to be made that they ought, after all, to be prohibited or at least controlled more closely than they are today.

Start with IPOs and capital formation. To bring a substantial company public in the U.S., you have little choice but to work with one of the larger Wall Street firms, which package the product for sale to the public. Ideally, one might expect this to be a very efficient balancing act that raises as much money as possible for the company without overpricing the offering and ripping off consumers.

Ladies and gentlemen of the jury, I invite you to consider: How well has Wall Street passed this simple, intuitive test of its effectiveness on behalf of our economy, investors and companies that require capitalization?

A 2002 article published by the National Bureau of Economic Research found that the average IPO that Wall Street brought to market from 1980 to 2002 jumped in price by more than 18% on the first day. Put another way, the issuers lost 18% of the capital they might otherwise have raised for their operations due to this mispricing – more broadly, due to their decision to have Wall Street firms raise their capital for them.

This is the average, understand. Renaissance Capital lists the top one-day movements from the initial offering price, and identifies 10 IPOs since 2001 whose first-day price jump exceeded 121%. A 2013 paper authored by Tim Loughran and Bill McDonald of the University of Notre Dame found a mean first-day movement of 34.8% – with some initial mispricings as high as 173.9% in favor of IPO investors on the first day of trading. (see here)

In addition, the larger brokerage firms all famously charge 7% of the total dollars raised for their IPO services. Does that sound like cartel pricing to you? Ladies and gentlemen of the jury, I invite you to ask yourselves: Is cartel-like price collusion legal in America?

But there’s more. In addition to their fees, the Wall Street firms all demand a hefty allocation of these shares which always seem to jump dramatically in value on the first day, which they then dole out to prospective customers and friends of the firm – i.e., as a marketing budget, but which some would consider a bribe. (see SEC news release 2002-14.) In fact, court documents in a lawsuit surrounding an IPO of eToys revealed that the issuer, Goldman Sachs, followed a standard industry practice of underpricing shares, selling those soon-to-appreciate shares to potential customers, and then asking for up to half the money back in the form of new business—raising more money from this source than the IPO fees themselves. Specifically, according to Joe Nocera, who reported on the case:

Goldman carefully calculated the first-day gains reaped by its investment clients. After compiling the numbers in something it called a trade-up report, the Goldman sales force would call on clients, show them how much they had made from Goldman’s I.P.O.’s and demand that they reward Goldman with increased business. It was not unusual for Goldman sales representatives to ask that 30 to 50 percent of the first-day profits be returned to Goldman via commissions, according to depositions given in the case.

Interestingly, Goldman didn’t reveal any of these excess revenues to the executives at eToys. (See here)

If we stick with the averages, then 25% of the capital the average company might have otherwise raised went into the pockets of Wall Street firms, directly or indirectly – representing monies that would otherwise have been deployed in productive enterprises. Ladies and gentlemen of the jury, Wall Street firms argue that they should not have to act as fiduciaries to the buyers of IPOs, since they are forthrightly selling the shares on behalf of the companies that engage them. But shouldn’t they be required to do a better job of watching out for the interests of the companies who are their customers? Or is all this simply a very expensive toll that Wall Street collects for the privilege of having capital raised in America?

And do companies going public have any choice but to pay this toll? Not under our current system, where the rules for selling shares to the public literally require a brokerage firm to handle the transaction.

It is possible that in the 1950s, when there were limited vectors to reach investors, it made sense to concentrate investment banking activities in the hands of a few firms with detailed expertise. But today, we have something called the Internet, which has the potential to create Dutch auctions, raise capital directly and match investors with companies much more efficiently than an army of tens of thousands of salespeople could.

Alas, raising money through the Internet is at this time confined to smaller pools of cash. The SEC’s interpretation of Title III of the JOBS Act limits businesses that raise money through crowdfunding to $1 million of crowdfunded investments per 12-month period. Moreover, the offering must take place through FINRA-registered entities. At that rate, it would have taken Facebook 104,000 years to take its company public.

If the public wants to do business directly with a new startup entity, buy through a new website or purchase a newly created product, the transaction is legal. If the public wants to invest in a company that is going public, the transaction has to be funneled through Wall Street and its various tolls and fees. In this corner of the industry, at least, the consumer revolution has been effectively thwarted. Later, we will look at the defendant’s successful efforts to control legislation and regulation that govern its activities, and you will perhaps be less surprised that these restrictions on non-brokerage competitors in the IPO world are strict and strictly enforced.

Let’s take a moment to consider additional lines of business that Wall Street engages in, including the manufacture of investment products for sale to institutions and (sometimes) individual investors. These business lines famously include pooled mortgages and consumer loans, plus the vast array of creative products known collectively as derivatives.

The stories of Wall Street salespeople using asymmetrical information to sell carefully-crafted junk to municipalities (Orange County, among others), institutions (Odessa College, among others), and miscellaneous pools of capital (including the Shoshone Indian Tribe) are by now familiar from the 2008-2009 economic collapse. To cite one example, an individual who referred to himself as Fabulous Fab and others at Goldman Sachs were able, under the brokerage industry’s suitability-related consumer “protections,” to sell an investment constructed of synthetic collateralized debt called Abacus Investments, which they knew would fail, and then allow a hedge fund manager bet against this built-to-fail investment product – and Goldman profited greatly on both sides of the transaction.

Just a day after this article was written, JP Morgan was hit with a settlement of more than $300 million because it didn’t disclose its preference for putting its customers in its own investment products.

Here again, the case against Wall Street depends on how you answer a simple question: Does this creative financial engineering benefit or harm the U.S. economy? If you chose “harm,” then I invite the members of the jury to brainstorm a bit. What other industry is allowed to do systematic harm to the U.S. economy, and profit enormously from it, and enjoy government-sponsored bailouts when its reckless behavior leads it into financial trouble? Before you blurt out an answer, I might point out that even the tobacco industry has had to compensate states and the government for the harm that its products do to the public’s health.

Financial toll booths

The second business activity conducted by Wall Street firms is trading for their own account, and here again brokerage firm lobbyists are able to ridicule the idea of a fiduciary standard as it would apply to “their firms.”

But ladies and gentlemen of the jury, I invite you to wonder what economic purpose is served, to the general economy, when Wall Street firms use their considerable consolidation of market power and research information to trade against, among others, their own customers. Even if we leave aside the so-called flash traders and their incremental siphoning off of pennies per transaction, should Wall Street firms be permitted to offer retail investment advice, and also function as retail investors for their own account?

Should that manifest conflict of interest be permitted in the U.S. economy? Should our defendant be allowed to comb his portfolio for stocks which seem to be tanking, and order his retail brokers to recommend those very stocks, sold out of the company’s own portfolio, as “excellent investment opportunities?” Should our defendant be allowed to cherry-pick the investment opportunities it happens upon in the course of its research, and buy the most attractive opportunities for his own account, rather than recommending them to his retail customers?

And if we decide that these activities should be allowed, shouldn’t they be regulated at least as stringently as the trading activities of SEC-registered RIAs, who have to disclose their personal trading activities and those of their employees so that examiners can look for evidence of preferential trading patterns?

If you add up these two sides of the Wall Street money machine, you discover something quite remarkable: Wall Street firms have gradually interjected themselves so deeply into the flow of capital that they are now raking in a sizable percentage of the total profits in America.

Ladies and gentlemen of the jury, the toll road that is the brokerage and financial industry accounted for roughly 8% of all domestic corporate profits in 1948, and this percentage bounced above and below 10% until 1985, when it began rising. The percentage jumped dramatically immediately after the 1999 repeal of the Glass-Steagall Act of 1932, when banks and brokerage firms were once again allowed to consolidate operations. By 2003, the brokerage industry was raking in an astonishing 40% of all the profits of all the public companies in America. This figure dropped to something under 10% back in 2008 (remember those bailouts), and then quickly rose to 30% again in 2012. (This is based on Bureau of Economic Analysis data.)

Table 12 of the most recent BEA data (see here) shows that in the first three quarters of 2014, the most recent time period when we have reliable statistics, the brokerage and financial sector generated $1.24 trillion in profits. In aggregate, all manufacturing firms in America generated $1.46 trillion in profits during the same time period. A relatively small number of individuals moving money around generated nearly as much in profits as all of America’s manufacturing companies that were actually making things.

As I sum up the first part of my case against Wall Street, I would suggest to the ladies and gentlemen of the jury that moving money around for its own profit, standing between investors and companies and exacting tolls whenever money is needed, are not positive contributors to the health of the American economy. If we are searching for an apt analogy in our biosphere, I would suggest that the most appropriate would be to ask whether the health of the animal population would be enhanced if we were denied protection from bloodsucking ticks and leeches.

The never-ending war of distinction

Ladies and gentlemen of the jury, let’s focus now on the most visible (to the public) aspect of the defendant’s business model: the retail-facing army of some 100,000 brokers. In my opening remarks I alluded to the fact that Wall Street firms are engaged in a lobbying battle over the fiduciary standard and how their brokers will be regulated, and I talked about strangling the fiduciary financial advisory profession in its cradle. I hope to show that our current fiduciary debate is actually part of a conscious, long-standing effort to mislead the public – a pattern of behavior that stretches back for decades.

In every emerging profession, there is an eternal war between professionals and sales agents over how they will be recognized by the public. Professionals – in this case professional advisors – are constantly trying to draw a distinction between those who offer service that is in the best interests of the client, and those who are posing as professional advisors in order to hide their sales agendas. Of course, the sales agents want to blur this distinction. They benefit from a reduction in sales resistance when the public is confused about who is, and is not, acting in their best interests.

Wall Street and financial advisors have actually gone through several rounds of this ongoing battle. The first and most primal distinction was between an advisor (or registered investment adviser) and a broker. The Investment Advisers Act of 1940 and the Securities Exchange Act of 1934 attempted to make this distinction very clear: Advisors (advisers) are acting on behalf of the public. The sales agents at the brokerage firms were to describe themselves otherwise.

To make this distinction even more clear, those who provide investment advice for a living, and hold themselves out as providers of advice, were required to register with the SEC. Brokers were exempted from registration only if their advice was/is solely incidental to effecting transactions.

Ladies and gentlemen of the jury, I invite you to consider how brokers and representatives of Wall Street firms refer to themselves today: as advisors, financial advisors, investment advisors, wealth managers and vice presidents of investments. The SEC has allowed not only this misleading terminology; it has also allowed the reps who so self-describe themselves to evade registering as registered investment advisors. The SEC commissioned a study to find out whether consumers were clear about which “advisors” were representing their interests, and regulated under fiduciary rather than suitability standards, as the law of the land clearly intended. The resultant study, released by the Rand Corporation in 2008, found that after being subjected to decades of advertising obfuscation, consumers have no idea whether they are working with a broker or an advisor, or the difference in the regulations they are obligated to operate under.

In a few moments, we will see how the brokerage firms have managed to get the SEC to do pretty much whatever they want, from a policy standpoint. Suffice it to say for now that this initial battle was won by Wall Street.

A second distinction emerged in the 1970s, when a small group of individuals referred to themselves as “financial planners.” Very quickly, the brokerage firms began creating financial plans to facilitate “needs-oriented selling.” Their plans recommended whatever product the brokerage firm wanted or needed to sell, or they were generic in nature, and the broker had wide latitude how to implement the generic investment advice.

This led to practices still in effect today in the independent broker-dealer world, where reps are said to wear a fiduciary hat when giving advice, and then switch to a sales hat when recommending the investments that will implement the advice. If they were actually wearing different colored hats as they switched from advice to sales, this might have benefited the public. In fact, no actual hats are ever worn or visibly switched.

The wirehouses won round two in a knockout.

The third distinction created by an increasingly desperate profession was “fee-only,” giving up all commissions or sales-related revenues. This distinction became extremely popular with the press and the high-net-worth clientele.

The response from the industry, ladies and gentlemen of the jury, was a stroke of genius. Brokers and other reps began referring to their compensation model as “fee-based,” and the public never was able to divine the (rather large) distinction between fee-only and fee-based. Firms were able to pay out generous commissions, AUM-like compensation for gathering assets, bonuses that look suspiciously like commissions, and incentive trips and perks to those who sell most effectively – without letting the public in on the joke.

Round three, ladies and gentlemen of the jury, also went to the defendant.

We are currently in round four of this battle to distinguish (or not) sales agents from fiduciary advisors, and this time the war is over the term “fiduciary,” loosely defined as giving advice solely for the benefit of the customer. This somewhat esoteric distinction served as a bright line for those consumers who understood the concept, until the brokerage industry proposed to “harmonize” the fiduciary standard with the brokerage sales model. It is unclear whether this initiative will succeed, but it has already managed to confuse the issue. And, as we will see shortly, ladies and gentlemen of the jury, the defendant’s stranglehold on legislative and regulatory initiatives suggests a preordained outcome.

I would suggest that even this bare-bones recital of the battles in this war would lead you to three simple conclusions:

- There is no obvious end to this succession of efforts to obscure the line between professionals and Wall Street agents;

- The Wall Street firms are very good at these battles, sometimes winning so quickly and easily that their effort seems perfunctory; and

- Each time Wall Street wins, the consuming public is returned to a state of confusion, uncertainty and the kind of disempowerment that accompanies a lack of information.

I invite you to conclude that here, once again, Wall Street’s net effect is not only harmful to society, but anti-consumerist by any definition you would want to apply.

Undue influence

It is time to ask ourselves: How does the brokerage industry get away with exempting itself from SEC registration, openly flouting the law of the land by marketing its advice and using terminology to describe its brokers that was supposedly reserved for professionals who sat on the same side of the table as their clients?

We can start with Congress, which makes the laws of the land, but even more usefully, also holds hearings that can be used to intimidate regulators, and also controls the funding for our regulatory organizations, including the SEC.

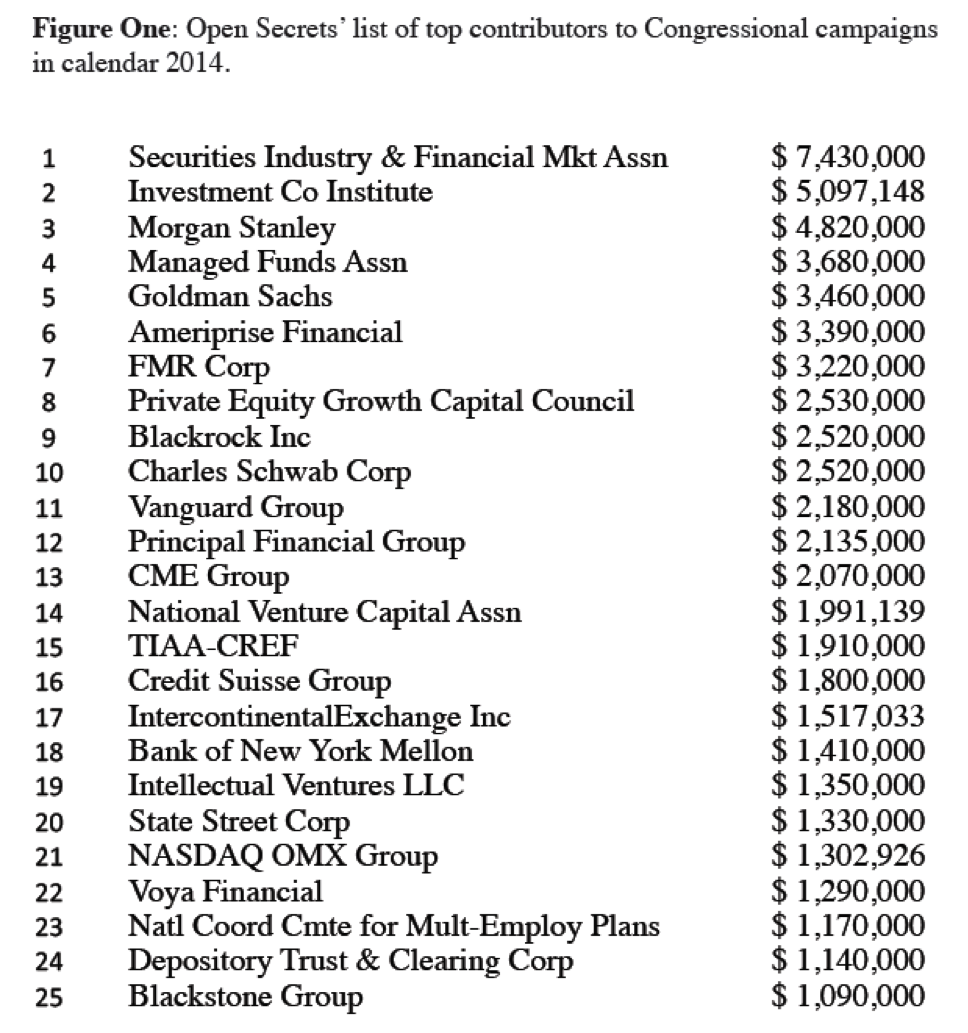

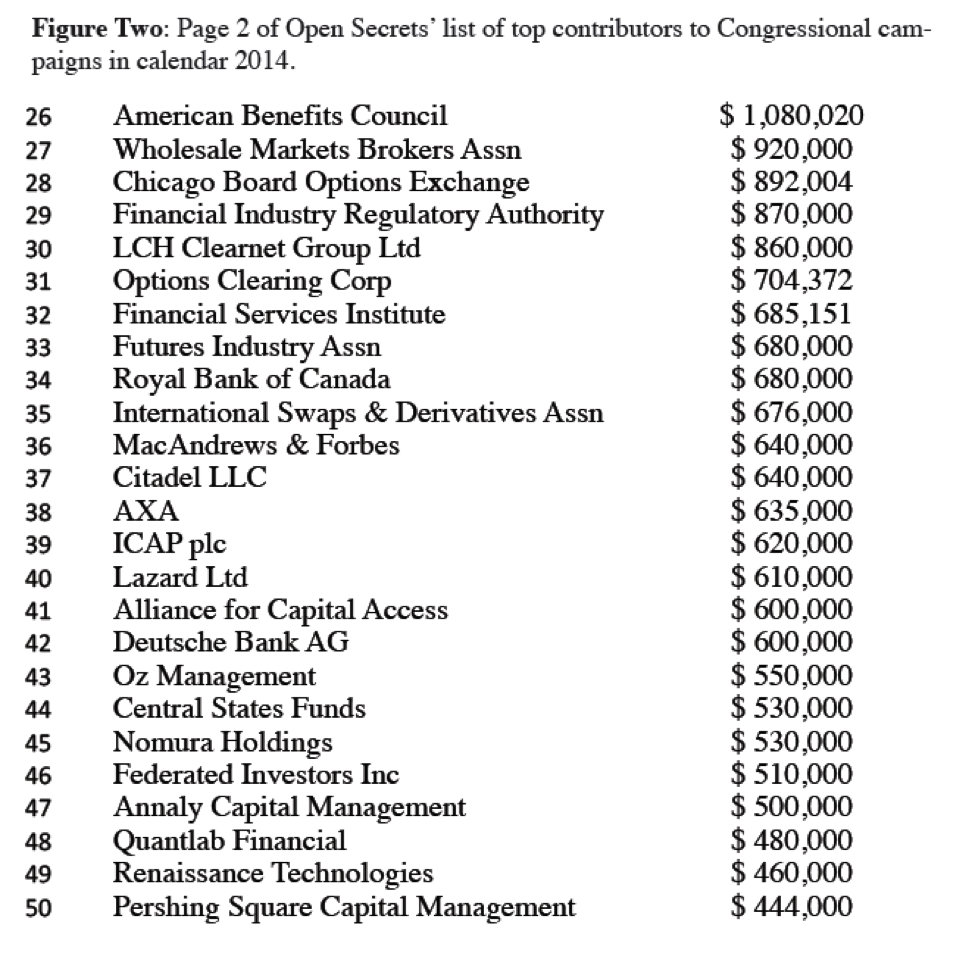

Figure one shows the largest 25 donors to Congressional campaigns, and Figure two shows the next 25. Ladies and gentlemen of the jury, if you scan this list, you might notice the Vanguard Group at number 11, and TIAA-CREF at number 15 are generally on the fiduciary professional side of the lobbying effort. But you will not find another supporter of consumer protection, or of clearly distinguishing professional investment advisors, anywhere on that list. The millions of dollars on the brokerage side of the ledger are balanced by a small $370,000 total contribution amount by TD Ameritrade (number 58 on the list) and an independent RIA called Fisher Investments at number 86 ($220,000 in contributions). The Financial Planning Association comes in at number 134 on this list, with $110,000 in total contributions.

Ladies and gentlemen of the jury, who do you think has the greater influence on Capitol Hill: the industry and its multimillion dollar contributions, or the profession with its mere thousands?

Of course, these amounts don’t add in the total number of dollars spent on armies of lobbyists. A recent graph compiled by the Huffington Post charted the number of meetings with regulators during the debate over the Dodd-Frank legislation, and found 1,793 meetings by representatives of the financial industry, plus 609 by legal professionals lobbying on behalf of Wall Street.

Pro-reform meetings, in total, came to 153.

A quick look at the regulators shows that they are largely led by people pulled from, and approved by, the brokerage industry. Among recent Treasury secretaries, we have Jack Lew, former COO of Citigroup. He was preceded by Tim Geithner, former president of the New York Fed, who famously was offered the COO job as Citigroup’s top executive. Mr. Geithner was preceded by Henry Paulson, former CEO of Goldman Sachs, and before that, John Snow, ex-CEO of CSX Corp. and a rare non-Wall Streeter in that post. Before that, Paul O’Neill, former chair of Alcoa Aluminum (another non-Wall Streeter) who succeeded Larry Summers, who earned $2.8 million as a consultant to Goldman, JP Morgan Chase, Citigroup, Merrill Lynch and Lehman Brothers. Before that: Robert Rubin, former co-chair of Goldman Sachs. Ladies and gentlemen, Wall Street insiders have clearly dominated White House regulatory and economic policy for the past 20 years.

The SEC, meanwhile, is currently chaired by Mary Jo White, formerly an attorney at Debevoise & Plimpton, which famously represented JPMorgan Chase in a variety of civil lawsuits – and she is by far the most independent-of-the-brokerage-industry chair we will encounter in our trip through recent history. She succeeded Elisse Walter, a former senior official of the NASD and FINRA, who succeeded Mary Schapiro, a former chairperson of the NASD and FINRA. Before Schapiro, the SEC was chaired by Christopher Cox, a former member of Congress who was known to be a champion of financial services deregulation. Before him: William Donaldson, founder of DLJ Securities, who succeeded Harvey Pitt, who had previously served as a securities attorney who specialized in representing Wall Street firms.

It would be hard not to notice the cozy relationship between Wall Street firms and the top securities regulator and policymaker in Washington, D.C. But the relationship goes further, deep into the staff at the SEC. Regulatory capture on 100 F Street, NE takes the form of an unwritten but visible offer: “If you [the staff person] play ball with your decisions and regulatory proposals, you will receive a reward when you leave in the form of a seven-figure salary for lobbying and legal work.” This practice is so common that it has a colloquial name in Washington circles; it is called “the revolving door.”

There have been various efforts to measure the extent to which this particular door revolves, but perhaps the most comprehensive is the 2013 report by the Project on Government Oversight, which found that from 2001 through 2010, 419 ex-SEC staffers filed 1,949 disclosure statements, disclosing that they planned to represent their new employers (or, in many cases, Wall Street clients of the law firms they joined) in matters pending before the SEC. One wonders how there can be that many “pending matters” (a delicate euphemism for regulatory infractions) over that short a time period, much less that ex-staffers would be addressing so many.

But here’s the punch line: These statements only have to be filed for the first two years after a staffer leaves the SEC, and it is not a requirement for all ex-staff members. To the extent that the filings don’t cover representation in matters two years after the staffer leaves office, or activities of staffers who are exempt from the filing requirement, the nearly 2,000 manifest conflicts of interest among current and former regulators represent an undercount of the actual impact of the revolving door.

In all 1,949 representations (plus others undisclosed), the dynamic is roughly the same: the staffer talks with people he or she has worked alongside for years, unruffling feathers, using friendship and camaraderie built up over years to mitigate the normal, logical impulse to apply the rules fairly and appropriately to the infractions. The revolving door is a forgiving door for an industry that routinely transgresses the regulatory boundaries – and that almost certainly means that our defendant is systematically creating lighter consumer protections for its own benefit.

Ladies and gentlemen of the jury, would you say that the ability to purchase lighter consequences for harming the public is in the best interests of the public and the American economic system? Or not?

What is FINRA?

But the organization that most closely “regulates” the Wall Street firms is FINRA, the Financial Industry Regulatory Authority. FINRA bills itself as a self-regulatory organization of the brokerage and broker-dealer world, and it has famously applied for the job of inspecting RIA offices on behalf of the SEC.

But is FINRA what it says it is? Or is FINRA, instead, an advocate of the brokerage industry masquerading as a regulatory body, which imposes its rules primarily to make sure that a predatory business model doesn’t go so far that it sparks outrage and a backlash in the public and Congress? That, ladies and gentlemen, is for you to decide. Let’s examine the evidence.

In a particularly well-researched column, attorney and college professor Ron Rhoades notes several instances where FINRA (and the NASD, its predecessor organization) seemed to act as an abettor rather than regulator of Wall Street activities later considered nefarious. One example is the price-fixing policies of the market-making member firms in the mid-1990s. Rhoades quotes then-SEC chair Arthur Levitt stating that the evidence showed that the NASD “did not fulfill its most basic responsibilities,” and “simply looked the other way” as these profitable, illegal activities mounted. The same column notes that FINRA failed to take any regulatory action at all regarding the derivatives scandal and the massive, costly failure of packaged securities like CMOs that led to the 2008-9 Great Recession – before or after the crisis. This led the Alliance for Economic Security to bluntly conclude, in its January 4, 2010 proposal for new rules, that “FINRA is not a reliable regulatory authority.”

Other examples cited include failure to regulate the conflicts of interest where securities analysts at the large Wall Street firms were issuing reports that were more in the interests of the investment banking department’s sales activities than in strict accuracy, where the analysts (famously including Henry Blodget) contradicted their own reports in emails to some of their customers. In fact, FINRA never took action in those cases; they were brought to light and ultimately prosecuted in a landmark settlement by the state securities regulators and the SEC.

And, of course, the most famous example of FINRA’s regulatory talent for looking the other way is the Bernard Madoff scandal, where the former non-executive chairman of the NASDAQ stock exchange conducted the largest Ponzi fraud in American history right under the noses of FINRA’s regulatory supervision for at least 28 years.

Finally, FINRA is also a lobbying organization, landing at number 29 on the aforementioned 2014 campaign contributions list, with $870,000 spent to promote the securities industry. When brokerage firms are caught in transgressions and fined by FINRA, they are obligated to pay fines to the same organization that lobbies on its behalf. What other industry in America gets to make a lobbying donation whenever they’re forced to disgorge ill-gotten profits?

In hearings, FINRA touts its independence from the brokerage industry, and points to the fact that its board consists of 10 “industry” members and 12 “public” ones. So the industry is outnumbered and outvoted whenever the board meets to decide how to regulate (and lobby for) the wirehouse community. Right?

Ladies and gentlemen of the jury, I invite you to look more closely as these 12 “public” members of FINRA’s Board of Governors, and see if some of them might have closer ties to the industry than the term “public” might imply.

The list includes:

- Josh Levine, former managing director at Deutsche Bank;

- William Heyman, former CIO of Travelers;

- Brigitte Madrian, the AETNA-endowed chair at Harvard;

- John Schmidlin, ex-head of technology at JPMorgan Chase;

- Robert Scully, former Senior Executive at Morgan Stanley;

- Leslie Seidman, former VP at JPMorgan;

- Elisse Walter, former FINRA vice president;

- Kathleen Murphy, President of Personal Investing, a Fidelity Investments subsidiary; and

- Randal Quarles, Managing Partner and Co-Founder of The Cynosure Group, former partner with the private equity firm Carlyle Group.

Nine of the 12 “public” members of the FINRA board are not what a reasonable person would describe as disinterested members of the investing public. A more logical headcount would say that 21 of the 24 board representatives represent the industry, and that FINRA’s activities are controlled by a board made up of current and former industry executives – and all claims to the contrary are at best misleading.

The verdict and the penalty

Ladies and gentlemen of the jury, this is certainly an abbreviated case against Wall Street. A more comprehensive case would bring up a longer list of scandals, more examples of stubborn opposition to the fiduciary standard over a period of decades, the ubiquitous advertisements that tout Wall Street’s superior advice despite the prohibitions of the plain law of the land and, whenever a customer tries to hold his broker to the fiduciary standards of RIAs, the claim in FINRA’s own arbitration system that the broker was merely acting as an agent to facilitate the customer’s own wishes.

I believe I have made my case with the facts and circumstances presented here. But I would also tell you that there are many more facts – and many more details– that could have been added to the brief.

In the interests of time, I am going to stop here and ask you to deliver a verdict.

At the beginning of my prosecution, I said that the defendant is charged with deliberately using deceptive business practices, operating a cartel, undermining consumer protections, engaging in anti-competitive behavior against the emergent financial advisory profession, exerting undue and improper influence on Congress and the regulators, raking in excess profits and thereby harming the American economy that it originally was created to benefit.

If you were to find my prosecution persuasive, and deliver a guilty verdict, then I hope you won’t be shocked when I ask for the death penalty. I would ask that your verdict deliver us a society and economy that doesn’t include brokerage firms at all.

Is this excessive? The question can be reframed: Are there other parties who can do the jobs that Wall Street currently performs better, more ethically, more efficiently and more beneficially to our economy as a whole? If we deprive our economic system of Wall Street’s services, are we harming, or helping it?

In that regard, I would invite you to consider that we have plenty of locally-based lending institutions that can be relied on to pick up the utility service of moving capital where it is most needed – at a very small fraction of the cost. We have the Internet for selling bond issues and new IPO shares to the public – should Wall Street’s Congressional stranglehold ever be lifted. This, too, would reduce costs, in this case practically to zero – certainly an improvement over the current 25% and higher.

We have discount brokerage firms to provide consumer investors with access to the capital markets, and fiduciary, SEC-registered financial advisors to provide investment advice and asset management services.

I would question whether the global economy needs complex derivative investments and creative pools of debt, and would ask whether the global markets would properly function if they were deprived of Wall Street’s helpful innovations that Warren Buffet has labeled “financial weapons of mass destruction.”

I’m humbly asking the jury to consider the death sentence for the defendant because nothing short of that will free the American economy from its persistent, powerful and profitable mischief.

I await your verdict.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com. Or check out his Insider's Forum Conference (for 2016 in San Diego) at www.insidersforum.com.

Read more articles by Bob Veres