Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws cash flows from it over time. The lump sum is invested in assets with future nominal payouts that are either unknown (stocks) or fixed (bonds). The objective is to combine the stock and bond investments to produce an income that is as stable as possible over a predetermined time horizon.

Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws cash flows from it over time. The lump sum is invested in assets with future nominal payouts that are either unknown (stocks) or fixed (bonds). The objective is to combine the stock and bond investments to produce an income that is as stable as possible over a predetermined time horizon.

It is common to use a 30- or 35-year time horizon when planning cash flows from an investment portfolio for a newly retired 65-year old client. For simplicity’s sake, in this analysis I’ll assume the client is a single male (the results can easily be adapted to a female or married couple).

The main difference between pre-retirement and post-retirement planning is that the time horizon is much more certain during the accumulation stage. If the client is 50, then he has about 15 years before reaching retirement age. Once the retirement age is reached, however, he has no idea how long his final life-cycle stage will last.

I will show that an eminently effective way to fund retirement is through a deferred-income annuity (DIA), particularly if it is purchased through an IRA as a qualified longevity annuity contract (QLAC). First, I will examine the conceptual justification for DIAs and why they are favored by economists. I will then describe the advantages of purchasing a QLAC, including the ability to avoid required minimum distributions (RMDs).

A conceptual framework for funding retirement

Without knowing the exact time horizon, it is common to develop a plan that will provide a stable income for all but the longest-lived retirees. To estimate the safety of a retirement income plan, we can look at the 2012 Society of Actuaries (SOA) mortality table, which is appropriate for most higher-income planning clients (who will live longer than the Social Security average). If we choose a 30-year time horizon, then 16.6% of male retirees will outlive their assets. Choosing a 35-year time horizon means that 4.2% of males will outlive their assets. Joint mortality is a much higher 37.2% at age 95 and 11.9% at age 100 for same-age couples.

The only way to ensure nominal spending certainty is to invest in fixed-income assets (inflation-adjusted income certainty requires investing in Treasury Inflation Protected Securities). “Risk assets” (primarily equities) provide a higher expected future spending (how much higher is a function of the equity risk premium, which may be much lower today than in the past), but the tradeoff is volatility in future assets available for spending. For this reason, it is appropriate to fund essential spending with fixed income assets and discretionary spending with risk assets.

If we choose to fund 35 years of spending for our 65-year old retiree at $44,623 per year (I will explain later why I’m using this number), then we’ll need to create a ladder of duration-matched bonds that pay this amount in each future year of retirement. Today, a AAA-rated corporate bond is yielding exactly 4%. After 1% asset management fees, you’ll need to purchase $24,707 of 20-year duration corporates to fund $44,623 in spending at age 85. If you need greater security, you could invest in a Treasury bond yielding about 3%, which would cost $30,030 today after asset management fees.

What is the likelihood that your 65-year old client will be around to spend the $44,623 in 20 years? Only 60.2% of males will live to age 85. Let’s say you have nine male friends who each want to invest $24,707 in bonds today in order to spend $44,623 at age 85. Why not get together and each chip in 60% of $24,707, or $14,875? You’ll save 40% on the cost of funding income with bonds in your 85th year because your dead friends will be helping to support the living.

Each year the deal gets even better. At age 90, only 38.4% of men will still be alive. So you can reduce the cost of funding income today by 60%. At age 95, you can cut your cost by over 80%. Do you want to fund income to age 100? Then you can buy income for a 95% discount by pooling assets with your friends.

What is the tradeoff of pooling? Your friends who die early will be funding the spending of those who remain. Is this a significant tradeoff? Well, to be blunt, they’re dead so they don’t care. Their beneficiaries might care, but as I will show later, the risk of pooling to beneficiaries is actually negligible or even nonexistent.

Pooling is the right way to approach funding later life income with safe assets.

Deferred-income annuities

The benefit of pooling longevity risk isn’t a secret among economists. There is literally no debate among academics that deferred annuitization is the most efficient way to fund later-life income. For those who want to “geek out” on academic studies, these articles by Moshe Milevsky and Guan Gong & Anthony Webb are a good primer on the advantages of pooling through income annuities that begin later in life to reduce the costs of funding retirement spending.

How much more efficient is a later-life DIA than a bond-ladder strategy? In my previous example, I chose the number $44,623 because it is the amount of income a 65-year old male can receive from a $125,000 DIA sold as a QLAC. By comparing the cost of funding $44,623 in spending through a bond ladder to buying a QLAC, I can show how much less expensive it will be to fund later-life spending through a longevity annuity.

Let’s start with the cost today of funding spending from age 85 through 100 using a bond ladder. Recall that in the first year, you’d have to invest $24,707 at 3% (4% bond yield - 1% AUM advisory fee) in order to receive $44,623 in your 85th year. You’d need to invest $23,987 to receive the same income at age 86 and a little less each year down to $16,334 to fund income in the 99th year of age. The total sum needed today to fund these 15 years of retirement spending is $303,795. If you’d invested in safe government bonds earning 2% (3% - 1% AUM), then you’d need to set aside $393,581 today to fund spending over 35 years.

Or you can simply buy a QLAC for $125,000 at age 65. If you want to be sure that a client will have enough money to fund nominal spending with a 4% failure rate (to age 100) with only government bonds, buying a QLAC will mean a savings of $268,581 today; or $178,795 if you invested in corporate bonds.

What does this mean to a retiree? He will have about $10,000 more to spend each year between the age of 65 and 85 with no reduction in failure rate. In fact, there is no failure rate because the money lasts as long as the retiree is still alive. That means that the 4% of male clients who live beyond age 100 will continue receiving the same nominal annuity payments. A longevity annuity is less risky and much less expensive than a bond ladder.

I said nominal, but QLACs can provide inflation protection, and products exist that can increase income payments by, say, 2% or 3% per year. This will reduce your initial income due to the $125,000 limit on QLACs. (By deferring income to later years, an inflation-adjusted QLAC might offer tax advantages, but that is beyond the scope of this article.) In order to compare apples to apples, I’m going to focus on comparing nominal bond investments to a QLAC, which consists of bonds wrapped in a pooling instrument through a DIA. Don’t get caught up on the nominal aspect of QLAC payments unless you would have invested your bond portfolio in TIPS. There is also evidence that spending in later life falls at about 1.5% to 2% per year even when healthcare costs are included. If you incorporate a health care risk hedging product (such as long-term care insurance) into a retirement income plan, then keeping nominal spending level will roughly match observed spending behavior.

How QLACs avoid required minimum distributions

Many of the economists who have researched the benefits of annuitization have been lobbying for ways to encourage retirees to buy annuity products – particularly to hedge against longevity risk. The U.S. Department of the Treasury deserves credit for pushing forward policy changes that incentivize the use of DIAs in IRAs.

The carrot to use DIAs is the avoidance of RMDs on IRA assets used to purchase a QLAC. Retirees can take up to 25% of IRA assets or $125,000, whichever is greater, and buy a QLAC that provides income later in retirement. Retirees can select a “return of premium” death benefit if they like (which reduces the efficiency of the QLAC). Payments can begin no later than age 85. Though they can begin earlier (say, 75 or 80), they are most efficient when they begin at age 85 since the mortality credit gains are the greatest.

The value of avoiding RMDs is not that great in a low bond-yield environment. But the impact will be much more important in behavioral terms for retirees because it allows them to avoid taking RMDs for 15 years. Annuitization is efficient to us eggheads, but the prospect of buying one can be unappealing to clients worried about not getting their money back if they die before age 85. The RMD avoidance feature of a QLAC provides a valuable way to increase an annuity’s appeal.

Estimating the benefit of avoiding RMDs is complex. Since we are comparing bond investments to bonds wrapped in an annuity, we have to assume that sheltered bonds will be withdrawn each year after age 70.5 from the IRA at a client’s income tax rate. Then the bonds, which we assume were to be used to fund later-life income, will need to be reinvested in a taxable account. But, you’ll end up paying taxes later on the payments from a QLAC. In an analysis I did with David Blanchett of Morningstar, we calculated that the savings at today’s bond rates from a $125,000 QLAC was about $10,000 at a 36% tax rate. This tax savings will, of course, increase in a higher bond-yield or higher tax-rate environment and doesn’t include the efficiency gains from pooling.

What if you don’t spend the QLAC income?

Some advisors may be considering the use of QLACs as a way to increase expected inheritance for clients who do not plan on spending any of the QLAC income. In a recent analysis, Michael Kitces called a QLAC in an IRA a “terrible way to defer the required minimum distribution.”

First, let’s revisit what a QLAC is. It is a bond portfolio that is wrapped in an annuity in order to pool longevity risk among retirees. In other words, it is a bond portfolio that is managed by an insurance company that then needs to spend resources to sell the product and manage the payments. Like any other insurance product, the net expected return on a QLAC will be less than the net expected return on the underlying investment (ignoring mortality credits). I don’t want my life insurance company paying out more than premiums it receives (plus the investment return on those premiums) because they’ll go out of business.

If you don’t value the pooling aspect of a longevity annuity, then all else equal you shouldn’t buy one. But the avoidance of RMDs provides an added edge that increases the net return on bond investments that are held within a QLAC. To estimate whether it makes sense to own a QLAC, the asset management expenses you’d pay on a bond portfolio managed by an investment advisor must be compared to the costs associated with managing the bond investments and providing income through an insurance company minus the RMD avoidance benefit.

Kitces used an internal rate of return of 8% to show that QLACs only made sense if a client lived to age 100. I’m assuming this IRR is net of AUM fees, which would mean a portfolio with an expected return of 9%. If I could locate a reasonably safe fixed income asset that paid 9%, I’d sell every asset I own to buy it. Unfortunately, insurance companies have to deal with the reality of today’s modest bond yields when constructing QLACs. And so do investment advisors who buy bonds at today’s rates.

This brings up another important point. Advisors who recommend the purchase of a QLAC should assume that the expense comes from the fixed income allocation within their client’s portfolio. In a $2 million investment portfolio with a 50/50 allocation, the new allocation (after purchasing a QLAC) should be $1 million in equities and $875,000 in bonds (or 53/47).

The proper way to compare a non-annuitized strategy to a QLAC strategy is to compare the IRR of the QLAC payments to the IRR of the expected inheritance amount using an all-bond strategy after taxes. Again, this is only for clients who are absolutely certain that they will never spend any of their annual QLAC distributions and place no value on receiving guaranteed lifetime income. In this calculation, one must multiply the survival probability by the amount that will be received in the future once taxes are withdrawn.

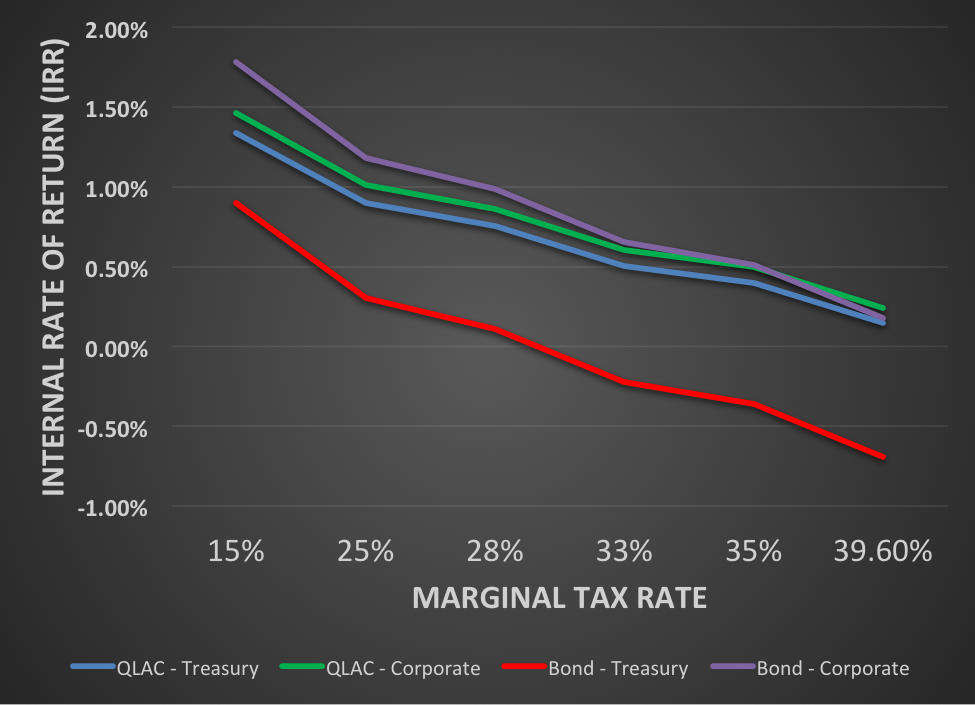

To do this as precisely as possible, I relied on one of my doctoral students, Jake Williams, to collect current yields at various durations for bond investments. We assumed that the bond investments are held in an IRA and then taxed as ordinary income when withdrawn. Once withdrawn, the bonds are held in a taxable account until death. Using the SOA mortality tables, we projected the distribution of when people will die and how much they will receive in an inheritance. The QLAC will only begin making payments at age 85, so anyone who dies before age 85 will receive none of their initial $125,000 investment. After age 85, the QLAC will be taxed as ordinary income. We ran the simulations for corporate and Treasury bonds and included QLAC simulations reinvested in both Treasury and corporate bonds.

As the figure shows, the IRR on a ladder of corporate bonds provides a higher expected net bequest than a QLAC reinvested in corporate bonds until the client reaches the 35% marginal tax rate. Beyond a 35% rate, the client will have a higher inheritance with a QLAC than if they had never purchased a QLAC. Compared to a ladder of Treasury bonds, a QLAC will provide a higher bequest at all tax brackets. In other words, the RMD benefit is enough to offset the costs of managing the annuitization pool at the 35% tax bracket for corporate bonds. If you were investing in Treasury bonds, you’d always have a greater inheritance with a QLAC.

The bottom line is that QLACs provide no tradeoff in terms of reduced bequest if a client is in the 35% marginal tax rate. Below a 35% tax rate, the tradeoff of purchasing a QLAC is modest and likely far below the insurance benefit provided by a financial instrument that pays income for life.

I’ve been an advocate of partial annuitization in retirement income planning strategies for a long time. The advent of QLACs simply increases the benefit of buying a DIA with IRA assets. To the extent that most clients will receive the significant benefit of longevity protection at little or no cost in terms of expected inheritance, there is little justification for not using one in a retirement-income plan.

Michael Finke is a professor and director of retirement planning and living in the personal financial planning department at Texas Tech University in Lubbock, Texas.

Read more articles by Michael Finke

Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws cash flows from it over time. The lump sum is invested in assets with future nominal payouts that are either unknown (stocks) or fixed (bonds). The objective is to combine the stock and bond investments to produce an income that is as stable as possible over a predetermined time horizon.

Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws cash flows from it over time. The lump sum is invested in assets with future nominal payouts that are either unknown (stocks) or fixed (bonds). The objective is to combine the stock and bond investments to produce an income that is as stable as possible over a predetermined time horizon.