Active management failed miserably in 2014. Was it because managers were less skillful or because there were fewer opportunities to outperform? Michael Mauboussin’s research provides the answer.

Active management failed miserably in 2014. Was it because managers were less skillful or because there were fewer opportunities to outperform? Michael Mauboussin’s research provides the answer.

During the last 40 years, an average of 60% of equity funds underperformed the S&P 500. But, according to the SPIVA data, 86.4% of large-cap managers underperformed their benchmark in 2014. The percentages were not much better last year for mid-cap (66.2%) or small-cap (72.9%). Mauboussin says there are logical reasons for this – and there are metrics that will identify those periods that favor active managers.

Mauboussin is managing director and head of Global Financial Strategies at Credit Suisse. He is the co-author (along with his colleague Dan Callahan) of a recent research paper, Min(d)ing the Opportunity: Excess Returns Require the Chance to Apply Skill. This article is based on that paper as well as an email exchange that I had with Mauboussin.

Mauboussin’s central idea is that skill alone is not a predictor of success in active management; a second ingredient – opportunity – must be present. Last year’s failure was not because there were fewer active managers or because they lost their touch.

The poor results in 2014 were due to a lack of opportunity. Performance was too tightly clustered, and it was too difficult for skillful active managers to separate themselves from the pack.

According to Mauboussin, “In 2014, the opportunities were particularly limited, contributing to the relatively poor performance of active mutual fund and hedge fund managers.”

I’ll discuss the implications for advisors of Mauboussin’s research, but first let’s look at the findings in his paper.

Documenting the lack of opportunity

Active managers can succeed in three disciplines: market timing, security selection and portfolio construction, according to Mauboussin. He looked at how those three tactics correlated with outperformance to provide an insight for the opportunity set that active managers faced in 2014.

As readers of this publication would expect, there is little evidence that mutual funds can time the market. But documenting that difficulty is problematic, according to Mauboussin. He hypothesized that cash balances would inversely correlate with subsequent returns. Fund managers would load up on cash when they expected meager returns and would draw down cash if opportunities were ripe.

But the empirical data showed the opposite; there is a positive correlation between cash balances and subsequent one-year returns. That could be partly explained by the influence of fund flows on cash balances. Managers may be increasing cash if they anticipate fund redemptions, which historically have correlated with down markets.

The other way to measure the opportunity for market timing is through what Mauboussin called “trendiness.” If the market moves steadily in an upward or downward direction, it is easier to time the market than if it zigzags. Trendiness can be measured through the ADX index, which measures the strength (but not direction) of trends. The ADX was fairly strong in 2014, but there’s little evidence active managers were able to capitalize on that opportunity.

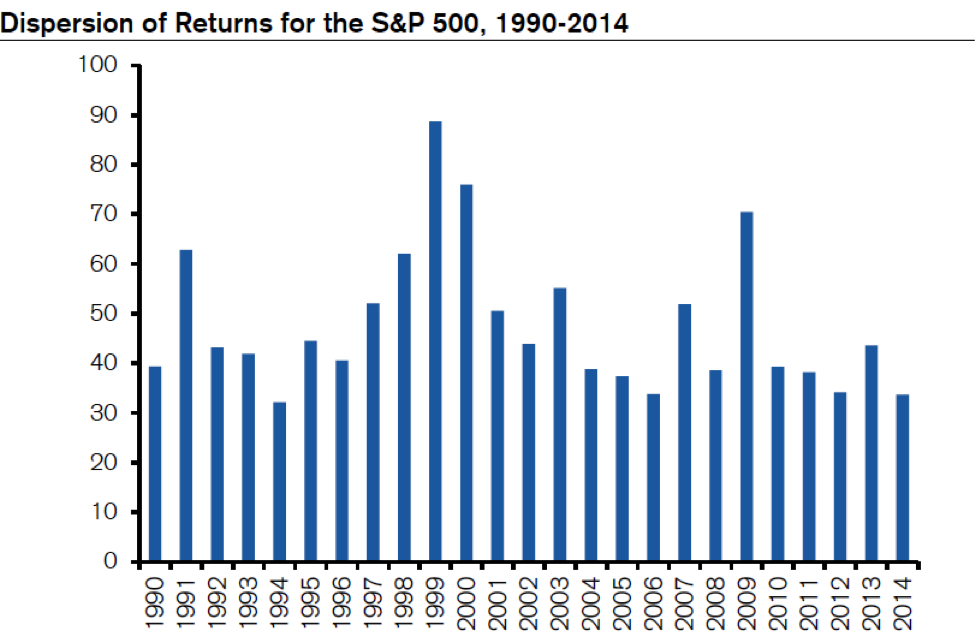

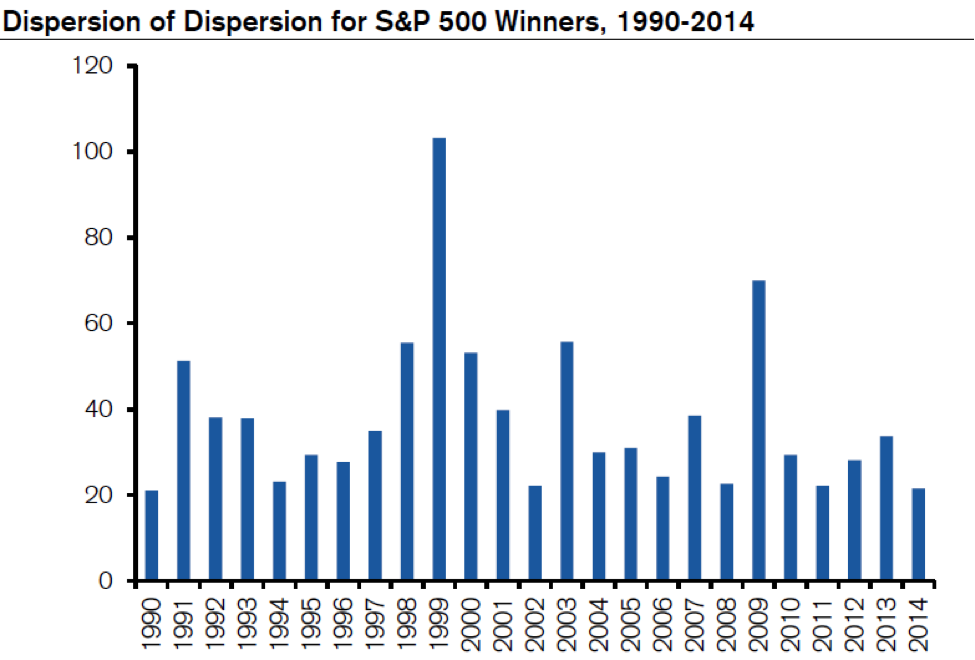

To find evidence of security-selection skill, Mauboussin turned to the Fama-French small-cap advantage. He found that “SMB” factor (the excess returns of small-minus-big stocks) correlated strongly with times when active managers outperformed. It wasn’t just small-cap managers, though, that did well. When SMB was high, all active managers did well because, according to Mauboussin, they held a disproportionate share of small-cap stocks.