Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Over the last 30 years, there has been a widely held belief, supported by data, in the predictive powers of the “slope” of the yield curve.[1] A steep yield curve implies economic expansion in months and quarters ahead. A flat or inverted yield curve implies economic weakness and heightened recession risks ahead. Although the traditional yield-curve analysis does not predict a recession, other equally persuasive indicators do.

The past is not always prologue for the future, so let’s ask the following question: Do those rules apply when the Fed has lowered the Federal Funds rate to unprecedented levels for over seven years and quadrupled the money supply? Questioning the value of traditional analysis is not only appropriate; it is necessary if one is to effectively perform economic analysis given the unique nature of central bank actions.

Traditional yield curve analysis

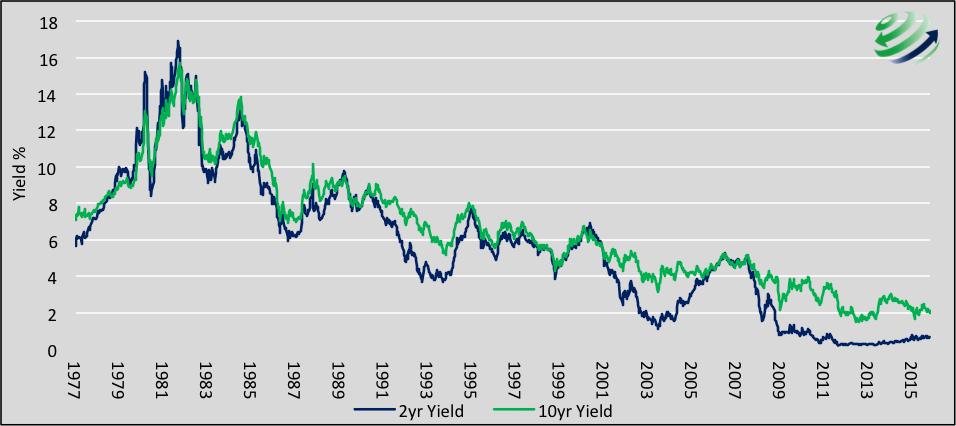

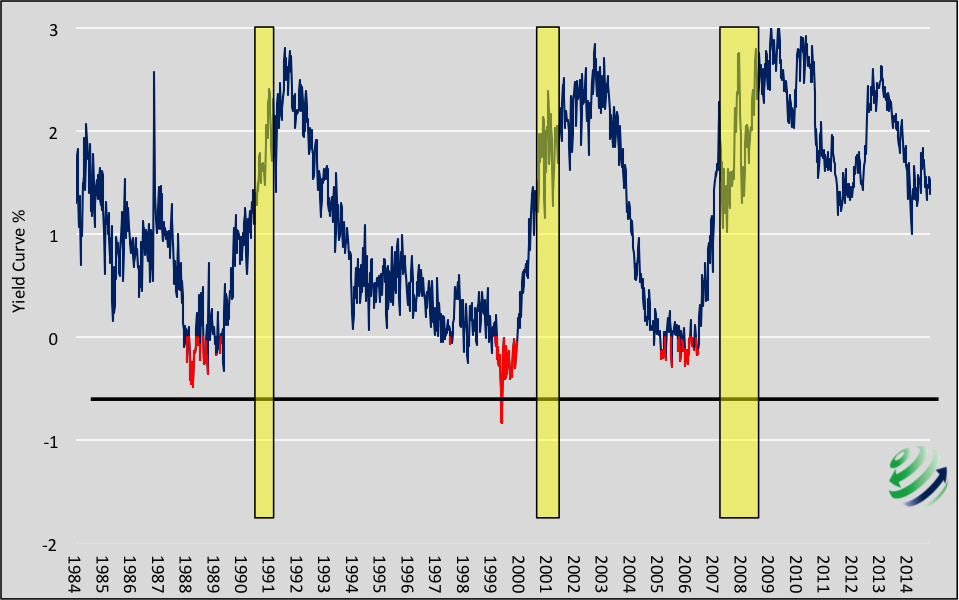

The graph below shows the slope of the yield curve and recessionary periods to demonstrate the predictive relationship. The first chart plots the yield on two-year Treasury notes and the yield on 10-year Treasury notes. The subsequent chart shows the difference between two-year Treasury Note yields and 10-year Treasury Note yields, otherwise known as the “2-10 curve.” To highlight the predictive nature of the yield curve, periods where the curve was inverted are plotted in red and recessions are highlighted with yellow bars.

2-year and 10-year Treasury Note Yields  Data Courtesy: Bloomberg

Data Courtesy: Bloomberg

The 2’s-10’s Treasury Yield Curve and Recessionary Periods Data Courtesy: Bloomberg

A simple deduction from the second chart is that when the yield curve, as measured by the 2-10 curve, has inverted the U.S. economy entered a recession within a relatively short period of time.

Based solely on the last 30 years and the slope of the curve today (1.42%), one would conclude that there is relatively little reason to worry about a pending U.S. recession. In fact, current levels are similar to those when recession typically ended and prolonged periods of economic growth began.

But Fed monetary policy has been far from normal. Investors therefore need to understand that the unprecedented nature of Fed policy and the fact that the Fed Funds rate has been pegged at zero since December 2008 plays a larger part in influencing the shape of the curve than in times past. This unprecedented posture by the Fed is distorting not only the price of money through interest rates but also economic activity. Prices of shorter maturity instruments, such as the two-year Treasury note, are heavily swayed by the monetary policy stance established by the Fed while longer maturity instruments, such as the 10-year Treasury, have been driven by the rate of inflation and economic activity. By keeping short rates artificially low through a zero Fed Funds target-rate policy, the Fed is heavily influencing short-term interest rates and causing the yield curve to be artificially steep. One way to test this theory is to use the Taylor Rule as an alternative Fed Funds target guide.

The Taylor Rule

The Taylor Rule, proposed by Stanford economist John Taylor in 1993, sets forth a prescriptive policy benchmark for the Fed Funds target rate based on the state of the economy using the rate of inflation and actual economic growth relative to potential growth. This formula not only suggests what Fed interest rate policy should be, but also serves as a useful measure of the aggressiveness of prior Fed policy.

Currently, the Taylor Rule says that the Fed Funds target rate should be approximately 2.85%. With current two-year Treasury yields at 0.60% and 10-year Treasury yields at 2.02%, the 2-10 curve is 1.42%. If the Fed were to follow the Taylor Rule and the Fed Funds rate were reset accordingly, the yield curve would become significantly inverted, with the assumption that two-year yields rise pro-rata with Fed Funds as is typical. In fact, the yield curve would be more inverted than at any time in the last 30 years and signaling an imminent recession. The chart below compares the current 2-10 curve versus a Taylor Rule-inspired curve.

Taylor Rule-Inspired Yield Curve vs. Traditional Yield Curve Data Courtesy: Bloomberg

Net interest margin

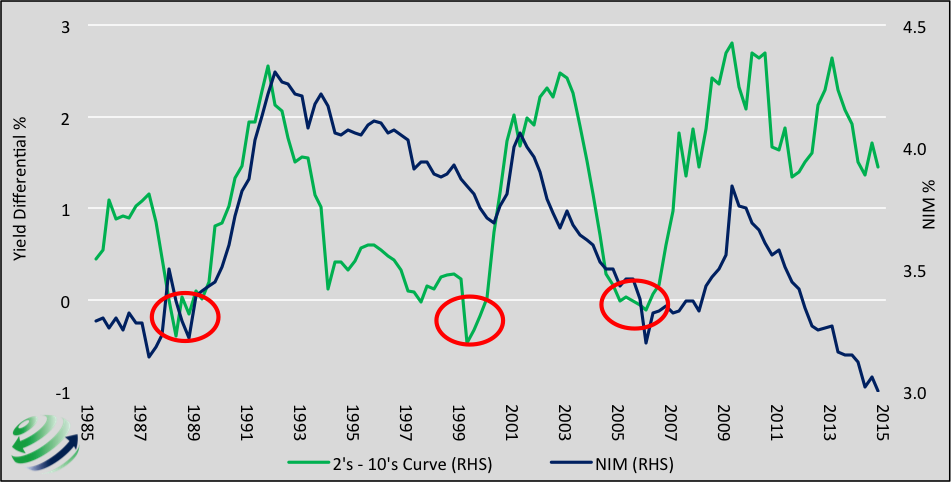

Another yield curve-derived tool used to assess the economic outlook is the net interest margins (NIM) for of financial institutions, predominately banks. Banks generate a substantial portion of their income from the difference between the yield at which they borrow and the yield at which they lend. The inputs to the NIM from a financial statement perspective are interest income minus interest expense. Historically, when the yield curve flattens, the ability of banks to generate income is challenged because the rate at which banks borrow converges towards the yield earned on loans and investments (NIM declines). When NIM contracts, banks lend less, constricting economic growth and flattening the yield curve. This self-reinforcing cycle is usually broken when the Fed lowers the Fed Funds rate, which steepens the yield curve and increases NIMs. The chart below compares the relationship of the 2-10 curve and NIM. The red circles emphasize periods where the yield curve was inverted, which ultimately led to recessions.

Clearly a strong correlation exists between the slope of the yield curve and NIM. The chart also reflects that although the 2-10 curve remains steep today, bank NIMs have declined to their lowest levels in over 30 years and are below those associated with an inverted yield curve preceding U.S. recessions.

NIM vs. Traditional Yield Curve Data Courtesy: Bloomberg

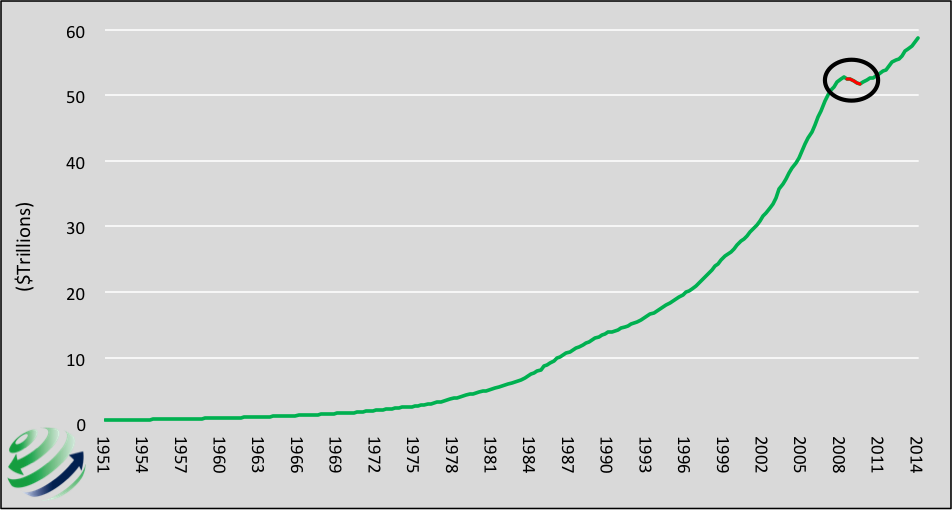

In the world of a zero interest rate policy, NIM may be a more valid indicator of future economic activity. In other words, economic forecasts based on the shape of the traditional curve may not be as relevant given the unprecedented monetary policy actions of the Fed. Very low levels of interest rates are squeezing bank profits, which is one of the key drivers of lending activity and a primary determinant of economic activity. Growth of the U.S. economy, even at today’s below-trend pace, is more dependent than ever on a continuation of credit growth. If bank lending activity is challenged as a result of declining NIM, the NIM will serve as a useful indicator of potential economic weakness. The graph below serves as a reminder of what happened in 2008, the only time credit growth declined in the last 65 years – the U.S. experienced the largest financial crisis since the Great Depression.

Total Outstanding Credit Data Courtesy: Bloomberg

Conclusion – Debt drives growth

Economic growth for the last 30 years has been increasingly funded by debt. For this scheme to continue, there must be increased incentives for the private sector to lend money. Since 1985 the incentive to lend, measured by NIM, has never been worse.

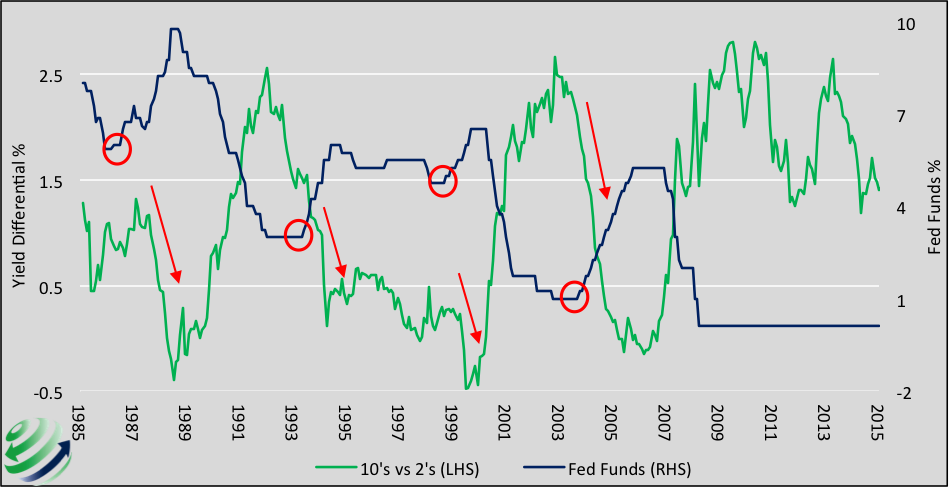

The Fed is currently contemplating raising short-term interest rates. If they follow through, the effect on NIM will slow economic growth. Historical periods of rate increases have corresponded with a flattening of the yield curve. The chart below highlights periods when the Fed initiated rate increases (red circles) and the corresponding reaction of the yield curve flatter (red arrows). Raising short-term rates, all else equal, will increase bank borrowing rates and further reduce NIM.

Fed Funds Rate and Corresponding Yield Curve Changes Data Courtesy: Bloomberg

The bottom line is that NIM and the Taylor Rule-adjusted curve are both flashing warning signs of economic recession while the traditional yield curve signal is waving the all-clear flag. Given the Fed actions of the last several years – a sustained crisis-driven policy of zero short-term rates and multiple rounds of quantitative easing – investors must adjust for distortions to traditional indicators. Using the shape of the yield curve as an indicator of the economic outlook requires more supporting evidence for validation. In this case, NIM and the Taylor Rule-adjusted curve contradict the traditional curve’s signal for the economic outlook.

If the Fed raises interest rates, it would be inconsistent with its prior actions. In fact, it would be a desperate effort to re-load the monetary policy gun as opposed to a signal of domestic economic strength. Not only is this a departure from the past, it would lead many to question the Fed’s motives. Blind trust and confidence in the Fed has propelled markets much higher than fundamentals justify.

Michael Lebowitz is the founding partner of 720 Global, an investment consultant specializing in macroeconomic research, valuations, asset allocation and risk management. Our objective is to provide professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and marketing. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. 720 Global research is available for re-branding and customization for distribution to your clients. For more information about our services please contact us at 301.466.1204 or email [email protected]

[1] The slope of the yield curve is a simple calculation comparing interest rates of various maturity terms. Traditionally, the slope of the yield curve is measured by the difference between interest rates of shorter-term government debt, such as the 3-month Treasury Bills or 2-year Treasury Notes, and long-term government debt such as 10-year Treasury Notes and 30-year Treasury Bonds.

Read more articles by Michael Lebowitz

Data Courtesy: Bloomberg

Data Courtesy: Bloomberg Data Courtesy: Bloomberg

Data Courtesy: Bloomberg Data Courtesy: Bloomberg

Data Courtesy: Bloomberg Data Courtesy: Bloomberg

Data Courtesy: Bloomberg Data Courtesy: Bloomberg

Data Courtesy: Bloomberg Data Courtesy: Bloomberg

Data Courtesy: Bloomberg