Should the Fed raise interest rates? Some believe that ultra-low interest rates are good for investors because they drive up the prices of stocks and real estate, fattening household balance sheets. Others counter that zero rates are an insidious tax, transferring wealth from borrowers to lenders, distorting incentives and misallocating capital for individuals and government and making the American investor poorer over time.

Where you stand on the Fed raising rates is likely to depend on which of these two positions you support.

We think the latter. Zero interest rates – which translate to negative real interest rates after inflation – are a massive transfer of wealth from investors to governments and other borrowers around the world. We’ll show that the scale of the transfer is nearly $1 trillion per year in the U.S. alone and will argue that the zero-interest-rate policy lowers expected returns on stocks and real estate as well.

Low interest rates hurt more than just investors. Everyone suffers because low rates distort consumption and investment decisions, potentially causing economic growth to be slower than it otherwise would be. Initially, in 2008-2009, low interest rates were an element or consequence of a policy of liquidity injection needed to avoid a collapse of the banking system and serious depression. Since then, however, they have become a tool of stimulative macro policy with limited success.

They are disastrous as an ongoing strategy.

In 1973, the economists Ronald McKinnon and Edward Shaw, looking back on the post-World War II period, described the policies of those times as financial repression.[1] Inflation was high and accelerating, while interest rates lagged behind. Thus, while the real economy grew strongly, savers and bondholders were devastated. The resulting “capital strike” was one of the reasons that we subsequently experienced a decade of high inflation and high unemployment.

Some current commentators, including the celebrated economist Carmen Reinhart, say that financial repression has returned.[2]

But today’s version of financial repression is different from that of the postwar period. The voting public will no longer allow governments to inflate away their debt wholesale with bouts of high and unexpected inflation. But low inflation with even lower nominal rates will accomplish much the same over time by not paying the interest needed to compensate for inflation.

Negative real interest rates are a nefarious tax, punishing savers and depriving the economy of one of its primary sources of income. John Maynard Keynes’s 1919 warning of the effects of inflation apply to today’s era of financial repression: “By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens… [W]hile the process impoverishes many, it actually enriches some.”[3]

First, “just the facts, ma’am”

What has been the recent experience of interest rates and inflation? First, we need to distinguish carefully between nominal and real rates. The nominal rate is the stated rate expressed in annual terms; say, an interest rate of 2%. The real rate is the nominal rate minus inflation. For most savings, consumption and investment decisions, it’s the real rate that counts.

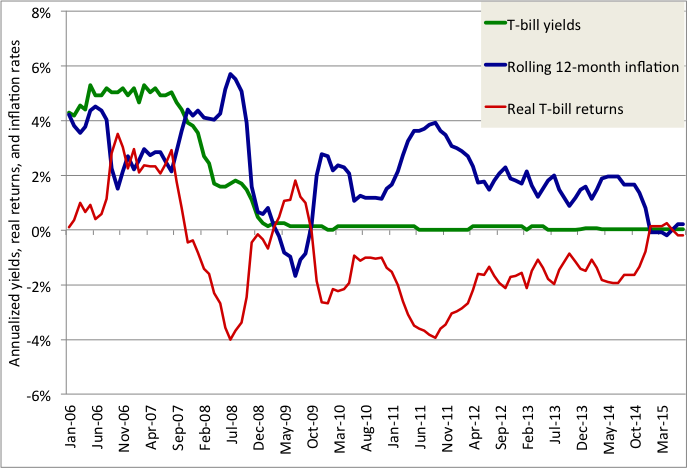

Exhibit 1 shows how the Fed responded to the unfolding severe recession of 2007-2009 and its aftermath. Nominal rates plunged from 4-5% in 2006-2007 to essentially zero over the last six years. Meanwhile, inflation has fluctuated around a six-year average of just under 2%. The real rate, then, has averaged just above ‑2% from mid-2009 to mid-2015. During the very recent past, January 2015 to the present, the real rate has been close to zero because inflation, dominated by falling oil prices, has also been zero.

Exhibit 1

Recent experience: Nominal and real short-term U.S. Treasury bill rates and inflation, January 2006-July 2015

Source: Constructed by the authors using data from Morningstar, FRED (the Federal Reserve), and the Bureau of Labor Statistics. Inflation is represented by the CPI-U-NSA.

Financial repression in this century is thus represented by the space between the zero axis and the red real-rate line. That is the “tax” paid by savers due to the zero interest-rate policy. Actually, that is a low estimate of the tax because real interest rates are usually positive, representing a reward to the investor for deferring consumption.

[1] McKinnon, Ronald I. 1973. Money and Capital in Economic Development, Washington, DC: Brookings Institution. Shaw, Edward. 1973. Financial Deepening in Economic Development, New York: Oxford University Press.

[2] Reinhart, Carmen M., Jacob F. Kirkegaard, and M. Belen Sbrancia. 2011. “Financial Repression Redux,” Finance & Development, Vol. 48, No. 1 (June).

[3] Keynes, John Maynard, The Economic Consequences of the Peace, Harcourt, Brace and Howe, 1920, p. 205. We are also reminded of Lenin’s comment that the surest way to ruin a nation is to debauch the currency.

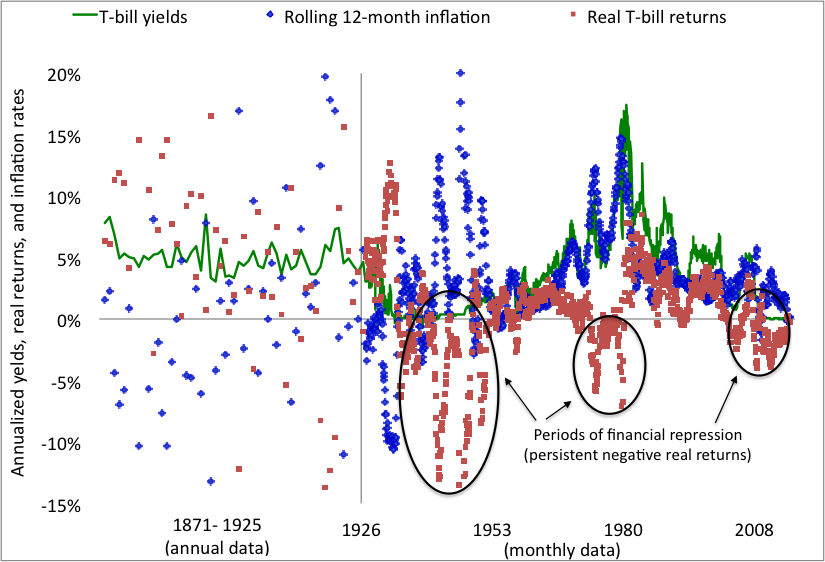

How positive are real rates historically? Exhibit 2 shows the same variables – nominal rates, real rates and inflation, back to 1871 when Robert Shiller’s data series begin.

Exhibit 2

Long-term experience: Nominal and real short-term U.S. Treasury bills and inflation, annually 1872-1926 and monthly 1927-July 2015

Source: Constructed by the authors using data from Morningstar, FRED (the Federal Reserve), the Bureau of Labor Statistics, and Robert J. Shiller. One-year bond yields are substituted for short-term (30-day and 90-day) yields over 1871-1926. Inflation rates are the CPI (CPI-U-NSA where available).

The exhibit looks complex, so a few words of explanation will help:

- As in Exhibit 1, green is the nominal Treasury bill rate, blue is rolling 12-month inflation and red is the real Treasury bill return.[4]

- The chart shows annual data from 1871 to 1925, then monthly data from 1927 to the present.

- Real Treasury bill returns averaged 1.02% over 1950-2006, 0.31% over 1927-2015 (the period covered by the Ibbotson studies) and 1.74% over the whole 1871-2015 period.[5] Nominal rates were much higher, consisting of the real return plus inflation.

- The ovals show periods of financial repression (red line persistently and significantly below zero) during World War II and the immediate postwar period, the Great Inflation years of the 1970s and early 1980s and recently.

- Between 1871 and 1926, the large amount of red above the zero axis shows that financial repression was rare during that period, and when it occurred it was due to high and unexpected wartime inflation, not low nominal interest rates. In fact, inflation was negative over most of the period, excepting World War I, which had high inflation, so fixed-income investors did extremely well in real terms.

Financial repression and equities

When we estimate the effect of financial repression on the overall savings of the American public, it’s important to remember that equities and real estate make up large fraction of these savings – probably a majority, if equity in one’s home is counted. While it’s easy to calculate the loss from receiving, say, -2% instead of 0% in real return on one’s cash- and bond-type savings (money market funds and bank deposits), the effect on equities and real estate is more difficult to estimate.

To estimate the effect on equities, consider that the period of ultra-low interest rates has seen a large increase in equity prices and a healthy recovery in home prices. This doesn’t feel like repression; it’s more like a gift from the gods. Where’s the repression?

High prices mean low expected returns. What investors got over 2009-2015 in capital gains on equities they’ll slowly give back (in whole or in part) through lower future returns. This principle applies to houses too. It doesn’t matter if you are buying the equities or houses afresh today or you’ve held them through the last six years – low interest rates do little or nothing to boost the truly long-term returns of these assets, and with high returns already captured in the recent past, future returns have to be lower.[6]

If we assume (for lack of a better estimate) that the loss from financial repression in fixed-income assets is 2% per year relative to what it would be with a more typical and benign policy and that an amount half that large (1% per year) is lost by equity holders due to rich current pricing, we can estimate the size of the implied “tax” on savings. We leave out real estate.

[4] The real Treasury bill return is calculated as the nominal Treasury bill rate (yield) minus the rolling 12-month inflation rate (that is, the average of the current month’s and previous 11 months’ inflation rates). The result is called a real return, not a real yield, because the real yield is the expected real return and we do not have expected inflation data with which to calculate an expected real return. All of these numbers are presented in annualized form.

[5] The Ibbotson studies cover 1926 to the present, but it takes 12 months of data to calculate a rolling 12-month inflation rate, so the nominal T-bill data cover 1926 to the present, but the other series (inflation and real returns) cover 1927 to the present.

[6] One could debate endlessly, and there is a great deal of literature doing so, how much lower. We won’t enter into that debate here, although one of us (Siegel) intends to do so when updating the “CAPE Crusaders: Shiller-Siegel Shootout at the Q Group Corral” article next year. (This title refers to Jeremy, not Larry, Siegel.) We assume that future equity returns are 1% lower, compared to 2% lower for fixed income.

Size of transfer from savers to borrowers

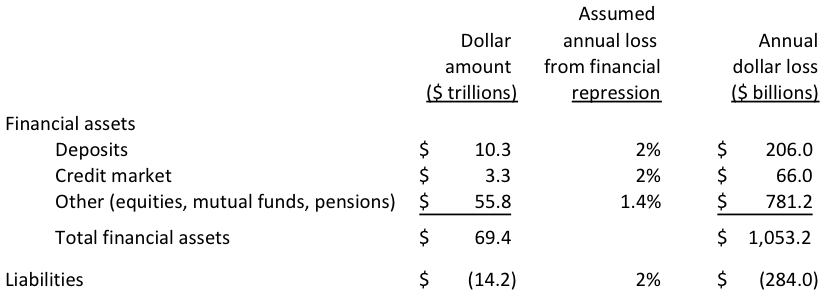

To find the implicit financial repression “tax” borne by savers, we multiply the “tax base” (the stock of financial assets owned by households) by the “tax rate” (our estimate of the annual percentage loss from financial repression), as shown in Exhibit 3.

Exhibit 3

Household and nonprofit balance sheet of the United States as of 1Q2015, excluding real estate, showing estimated annual income loss from financial repression

Source: Federal Reserve, Financial Accounts of the United States, Z.1, table B.101, 2015Q1 (households + nonprofits)

The “tax” base is the amount of savings, obtained from Federal Reserve data. We assume that the “other” category, consisting of equities, mutual funds and pensions, is invested 60% in equities and 40% in fixed income. Deposits, credit market investments and liabilities are assumed to be 100% fixed income.

For the “tax” rate, we assume a 2% annual loss from financial repression for fixed income and 1% for equities. Thus the blended “tax” rate for the “other” assets category is 1.4%.

Multiplying through and taking the total, we arrive at $1,053.2 billion per year – roughly a trillion dollars a year that is taken out of household balance sheets and transferred to others. That’s more than 5% of GDP!

This estimate is for the United States alone; moreover, the U.S. is not an island of financial repression. In fact, there is financial-repression contagion. The total loss for the world is much larger.

What are we to make of this transfer? We look at the assets of the household sector because households consist of actual people; non-household agents in the economy, chiefly businesses and governments, exist to serve households. Thus it is households that ultimately matter in measuring the magnitude of financial repression.

Where does this transfer go? When we look back at Exhibit 3 we see that roughly $284 billion goes right back to households, mainly due to mortgage debt. We might think this should be netted out, giving only $769 billion as the size of the transfer from households. But this ignores the critical fact that much of the $284 billion is a transfer, from one set of households (savers and investors) to another (mortgage borrowers). Wealth and income transfers may or may not be an appropriate policy goal, but opaque transfers as a consequence of monetary policy are exceedingly bad public policy.

Some of the transfer is effectively a tax in that it goes to the government, the result of low rates for federal, state and local and agency securities. We estimate this to be roughly $190 billion.[7]

A part of the transfer is an effective subsidy to banks that hold deposits paying interest below inflation. In fact, after the financial crisis, zero interest rates were one method whereby the government aided bank recapitalization.

The most important thing to remember, however, is that this transfer from savers to borrowers distorts prices and impairs the effective functioning of our economy. Decisions about the price of goods and services today versus the future are some of the most important we make as consumers, workers and investors – decisions about whether and how much to invest in education, work, leisure, retirement, or productive businesses. When prices are distorted, we are all pushed to behave in inappropriate ways.

What a mess. It will take teams of PhDs years to unravel all the distorted incentives, capital misallocations and foregone savings opportunities that emerge from the financial repression of the early 21st century.

The case against raising interest rates

Any recommendation to raise interest rates needs to acknowledge that many well-informed people are against raising rates.[8] We need to understand the arguments behind that opposition and assess the costs and benefits of lower versus higher rates.

We have seen that there are costs to the current zero interest rate regime. Conventional economic wisdom says that these costs are the necessary burden we bear to avoid the calamity brought by higher rates. The claimed benefits of low rates are twofold: first, low rates generate inflation and forestall deflation (the effect of which is purported to be disastrous, through increasing the real value of an already crushing debt burden). Second, low rates stimulate growth and were necessary to repair the economy following the 2007-2009 financial crisis.[9]

The changing nature of monetary economics

The problem with this conventional wisdom – that low rates both generate inflation and stimulate the economy – is that it may not be correct. Some of those economists who have most eloquently advocated for the importance of money in our economy have also warned of the limited power of monetary policy.

Consider Milton Friedman, the prime exponent of monetarism in the 20th century and the economist who, with Anna Schwartz, argued convincingly that “the Fed caused the Great Depression."[10]

Nonetheless, Friedman himself said, "[W]e are in danger of assigning to monetary policy a larger role than it can perform, in danger of asking it to accomplish tasks that it cannot achieve, and, as a result, in danger of preventing it from making the contribution that it is capable of making."[11]

John Cochrane, Distinguished Fellow at both the University of Chicago and the Hoover Institution and a successor to Friedman as a serious monetary theorist, strikes the same tone in a recent blog post: “Monetary policy is a lot less powerful than most people think it is. Bad monetary policy can screw things up. But our growth doldrums are not the result of monetary policy, nor can monetary policy do a lot to change them.”[12]

We need to take seriously the words of thinkers such as Friedman and Cochrane because they have thought carefully about money and are themselves strong advocates of the importance of money in economics. And there are reasons – based on both theory and recent experience – to question the conventional view that low rates can both generate inflation and stimulate growth.

[7] We estimate, very roughly, that the U.S. public holds (directly and indirectly) $3,850 billion of federal debt, $2,370 billion of state and local debt and $3,200 billion of agency and GSE debt for a total of $9,430 billion. The estimates for the first quarter of 2015 are calculated by the authors from Federal Reserve Z.1, tables L.209, L.210, and L.211. We assume that households hold (mostly indirectly through intermediaries) any securities not held by banks, the monetary authority or the rest of the world. This may somewhat overestimate the household holdings, but we do not think dramatically. Further, the number for state and local is somewhat underestimated (since the amounts held by banks and the rest of the world include municipal securities issued by corporations).

[9] One intriguing part of the case against raising interest rates is that highly indebted governments can’t afford to pay higher rates. In this view, low rates are the Fed’s contribution to solving the government debt problem – the other side of the effective tax generated by negative real rates. When U.S. entitlement spending is projected through the baby boomers’ retirement years without modifying benefit formulae, government debt mushrooms at typical interest rates but is more well behaved at very low rates. The purpose of monetary policy, however, should not be to support the government, but to support the people.

[10] This is hyperbole, but only slightly. More accurately they argued (in Friedman, Milton, and Anna J. Schwartz, A Monetary History of the United States, Princeton University Press, 1963) that mistakes in Federal Reserve monetary policy turned what would have been a severe recession into the Great Depression of the 1930s. Ben Bernanke, when a member of the Board of Governors of the Federal Reserve but before being appointed chairman, went so far as to say: "Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You're right, we did it. We're very sorry. But, thanks to you, we won't do it again." Bernanke, Ben S., “On Milton Friedman's ninetieth birthday,” Conference to Honor Milton Friedman, University of Chicago, November 8, 2002, http://www.federalreserve.gov/boarddocs/speeches/2002/20021108/default.htm

[11] Friedman, Milton, Presidential Address to the American Economic Association, American Economic Review, March 1968, vol. 58, no. 1.

Surprises in the effects of monetary expansion on inflation and growth

Consider our experience over the past seven years. Rates have been pegged at zero. Conventional economic theory predicts that such a peg would lead to unstable inflation, but in fact inflation has been remarkably stable, trending slightly downward. Further, conventional wisdom would predict that low rates would produce higher inflation – again not what we have witnessed. Importantly, as described by Cochrane in his “Doctrines Overturned” blog post, recent developments in macro theory indicate that raising rates may (at least in some circumstances) generate higher inflation.[13]

Finally, conventional wisdom would predict that zero rates and the resulting negative real rates would be highly stimulative and, while the economy has grown, it has not been spectacular. Of course, it is possible that, without low rates, growth would have been significantly lower.

If low rates are not the macroeconomic panacea economists predicted, then the danger of higher rates may also be lower than we have thought and must be weighed against the obvious and present costs of low rates.

Arguing in favor of higher rates, Cochrane has written,

All current macroeconomic theories start with the same basic story: when interest rates are higher, people consume less today, save, and then consume more in the future. Higher real interest rates mean higher consumption growth.[14]

For those who care about the future beyond the next few quarters, higher real interest rates are to be desired. Rather than trying to maximize current consumption or production as measured by quarterly GDP data, we should be trying to maximize wealth, which is (by simple accounting identities) the present value of all future consumption.[15]

But our core objection to near-zero interest rates is more basic: they don’t treat creditors and debtors fairly. If we want healthy levels of saving and investment and a future that is better than our recent past, we have to have healthy rewards for saving and investment. A permanent bias in favor of debtors (including governments) and against creditors is the wrong way to go.

Conclusion: Growth is the answer

Growth profoundly influences everything. It drives stock prices, the debt/GDP ratio and even bond prices and currency values through the mechanism of the market assessing a government’s ability to pay its debt.[16] We are already facing a headwind or decrement to GDP growth from the slowing of population increase.[17] Technological change, which shows little or no sign of slowing, is the main driver of per capita GDP growth; but poorly designed incentives and thoughtless policies can interfere with the translation of technological change to economic improvement. There is every reason to encourage growth and no reason to restrain it.[18]

Growth is also good for democracy and free markets. Good fortune is always unevenly distributed, so when growth is slow, the less fortunate suffer disproportionately. And if a large proportion of the population does badly and rebels, the populist policies they typically demand make growth even slower.

Investors prosper when the economy prospers. Equity investors prosper by holding a claim to the change, on the margin, in aggregate wealth.[19] Fixed-income investors benefit from real interest rates that are high enough to reward savers and spur them on to greater savings and investment. Investors want both the real interest rate and the equity risk premium to be higher than at present, so they benefit, as we all do, from policies that stimulate long-term growth.

We want change. We want adaptation. We don’t want the stasis and misallocation that financial repression brings.

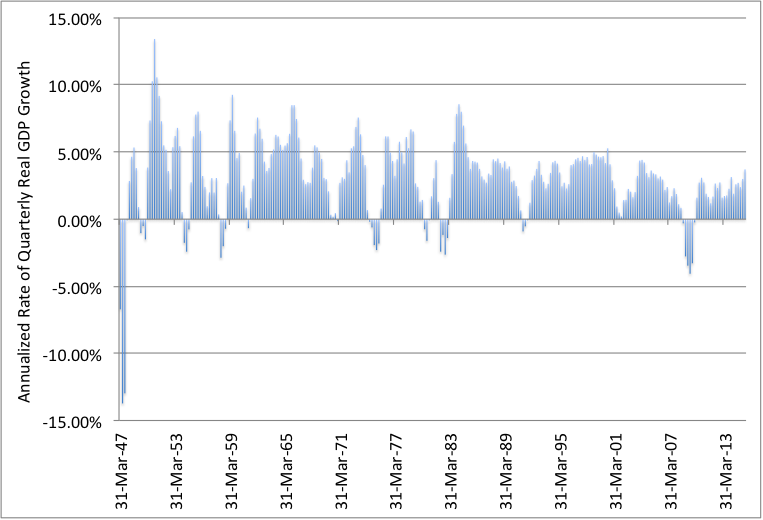

Such policies include normal interest rates for normal times. We’re close to being in normal times. For some two centuries, the United States has enjoyed 1.8% per year productivity growth (real per capita GDP growth). That is our benchmark for normal times. Real overall GDP growth consists simply of productivity growth plus population growth. At the current population growth rate of 0.7% per year, our benchmark for normal times translates to 2.5% real GDP growth.

Exhibit 4 shows U.S. real GDP growth, quarterly (but stated as annual growth rates), from 1947 to the most recent quarter.

Exhibit 4

Real U.S. GDP growth, stated as annual rate, quarterly 1947-2015

Source: http://www.multpl.com/us-real-gdp-growth-rate/table/by-quarter using U.S. Bureau of Economic Analysis data.

Look at the last few years in Exhibit 4: we’re averaging just about 2.5%. The world after 2011 looks a lot like the world before 2007. In terms of monetary policy, let’s return to what President Warren Harding liltingly called “normalcy.” The right word is normality, but his enthusiasm sometimes got ahead of his vocabulary, and his coinage stuck. Right now, we could use some of Harding’s enthusiasm, a big dose of normalcy and an end to financial repression.

Laurence B. Siegel is the Gary P. Brinson director of research at the CFA Institute Research Foundation, and an independent consultant. Thomas S. Coleman is executive director of the Center for Economic Policy at the Harris School of Public Policy, University of Chicago. The authors may be reached at [email protected] and [email protected].

[15] What got one of us (Siegel) to think about writing this article in the first place was a comment on Cochrane’s blog at http://johnhcochrane.blogspot.com/2013/03/fun-debt-graphs.html, by a University of Belgrade Ph.D. student, Vladimir Andric:

Dear Professor Cochrane:

You are arguing that growth is a solution to the U.S deficit problem. However, it seems to me that you are treating GDP growth as exogenous. In other words, it is not the spending that is high, but rather the growth that is low. But, maybe, the growth is low because spending is high. A paper by Alesina et al. (2002) investigates the impact of fiscal policy on profits and investments in OECD countries. The authors argue that public spending, especially its wage component, has a sizeable negative effect on profits and business investment.

Cochrane replied, “How refreshing. Most of my other commenters seem to be Keynesians who think more spending = more growth. I agree, substantially less spending in the right places could increase growth.” Alesina’s paper is at https://www.aeaweb.org/articles.php?doi=10.1257/00028280260136255

[18] See also Sexauer, Stephen C., and Bart Van Ark. 2010. “Escaping the Sovereign-Debt Crisis: Productivity-Driven Growth and Moderate Spending May Offer a Way Out.” Executive Action Series, Conference Board, New York. Drawing on the work of the Nobel Prize-winning economist Gary Becker and the University of Chicago professor Kevin Murphy, these authors show that the public-debt problem is greatly ameliorated by rates of long-term economic growth in excess of the growth rate of government spending. Their work was discussed in Advisor Perspectives, June 9, 2015.

[19] This claim is shared with human capital holders (who receive higher wages), governments, and others, but changes in overall wealth flow through to equity holders very directly.

Read more articles by Laurence B. Siegel and Thomas S. Coleman