Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

We recently saw an analysis from StarCapital that provided context for how the market over the last several years resembles the late 1990s and other periods when value strategies underperformed.

As we found their thesis to be compelling, we did our own analysis using the same source data to better understand and expand on their results.

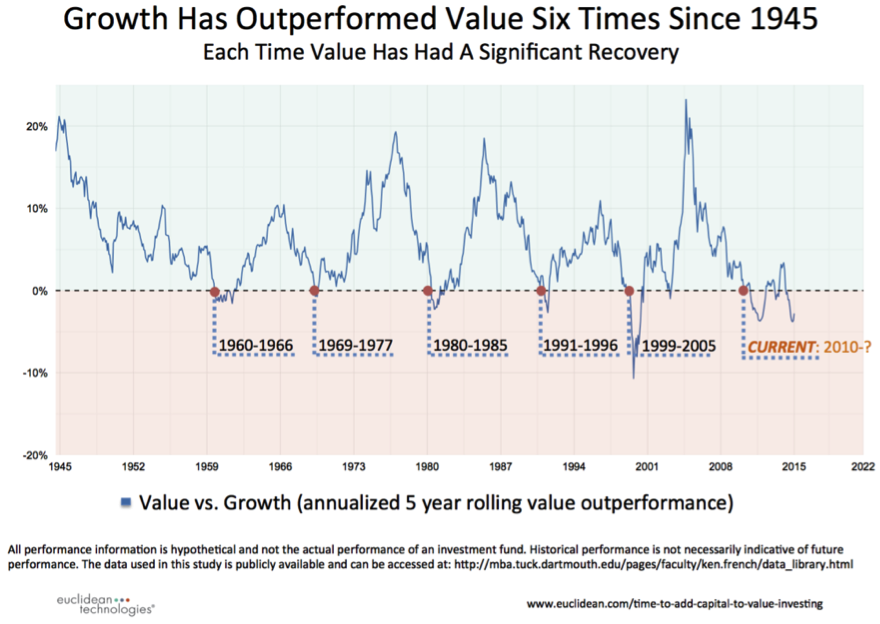

The chart above plots the trailing five-year annualized return of a hypothetical portfolio (the value versus growth portfolio) that goes up when value stocks are outperforming growth stocks and down when growth is outperforming value. The returns of this portfolio were constructed using data that can be found at Kenneth R. French’s website, where a value stock is defined as one having high book equity to market price. In this case, we are looking at the relative performance of the 20% least expensive (value) companies in relation to the 20% most expensive (growth) companies. All returns are compounded monthly.

The chart shows that value outperformed growth across most five-year periods and did so by roughly 5% annualized over time. This value premium has been observed and commented on by many investors and researchers. But, why does it persist over time? Value stocks are inexpensive in relation to things that are known about a company, like their earnings or book value. Growth stocks are expensive because investors expect those same things (earnings, book value, etc.) to quickly grow. We believe investors are not good at predicting the future, and they are prone to extrapolating recent results too far. Thus, value stocks – as they often are working through some form of hard times – may become over discounted. Likewise growth stocks – as they often have posted strong recent results – may have prices that reflect unrealistic future expectations. We believe this is a major reason that inexpensive stocks outperform expensive stocks over time.

Even so, it is obvious that value stocks do not always outperform. In fact, since World War II, there have been six distinct periods when growth outperformed value on a trailing five-year compounded return basis. We are currently in one of these periods; the last time this happened was during the dot-com era.

As shown in the above chart, during the previous five periods when growth outperformed value, value subsequently delivered very strong results over the next five-plus years. In the current cycle, the value rebound has not yet occurred. Why? Will such a rebound eventually occur?

We have an aversion to predictions and thus have nothing to say about when and why value might reassert itself. We do, however, believe in cycles. As Howard Marks says, "I think it’s essential to remember that just about everything is cyclical. There’s little I’m certain of, but these things are true: Cycles always prevail eventually. Nothing goes in one direction forever.”

For this reason, and because we embrace the logic of buying shares in companies at inexpensive prices, the state of this current cycle supports a decision to move capital away from growth-oriented strategies and into value-focused investments.

Would you like to reproduce these results in the R programming language and from the source data website? Click here to get the code that generates the first chart and here for the second chart.

Mike Seckler and John Alberg are the managers and founders of Euclidean Technologies Management, an investment firm that applies machine learning and systematic approaches to value investing. John and Mike have worked together for over 18 years; prior to starting Euclidean in 2008, John and Mike co-founded Employease, a software-as-a-service provider that was acquired by Automatic Data Processing (NASDAQ:ADP) in 2006.

Appendix

Historical results represented herein are for illustrative purposes only and are not based on actual performance results. The hypothetical portfolio and the associated returns do not reflect the effect of transaction costs, bid/ask spreads, slippage or management fees. Historical results are not indicative of future performance.

All results and the analysis described in the above post exclusively used data obtained from Kenneth R. French’s research data library hosted at http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

To construct the hypothetical set of returns representing the outperformance of value over growth, we used the particular data file at http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/ftp/25_Portfolios_5x5_CSV.zip. This dataset contains the returns of 25 portfolios. The portfolios, which are constructed at the end of each June, represent the intersections of five portfolios formed on size (market equity, ME) and five portfolios formed on the ratio of book equity to market equity (BE/ME).

In our analysis we constructed a hypothetical portfolio (the Value vs. Growth portfolio) that goes up when value stocks are outperforming growth stocks and goes down when growth stocks are outperforming value stocks. We calculated the monthly returns for the value vs. growth portfolio to be equal to the average of the five high BE/ME portfolios minus the average of the five low BE/ME portfolios in the dataset referenced above. All returns in our analysis are compounded monthly.

Differences between this analysis and the referenced similar analysis by StarCapital result from slight differences in methodology (e.g., the files in the data library the portfolio returns are constructed from and whether simple or compound returns were used to calculate trailing 5-year rolling returns, annualized returns and cumulative returns). In our case, we used compound returns throughout.

Read more articles by John Alberg and Michael Seckler