General consensus is that the Federal Reserve (Fed) will hike interest rates in September or thereafter — the first US rate hike in more than a decade. It’s no surprise investors are concerned about whether it will cause a replay of 2013’s “taper tantrum,” the dramatic sell-off in so-called risk assets that hit emerging markets particularly hard when the Fed announced it would begin scaling back its quantitative easing (QE) program. In our view, Asia is now at less risk of a similar reaction.

What’s different?

When the Fed does actually start to tighten policy this time, why would Asian markets react differently? While limited inflation risk following the collapse of commodity prices makes a big difference, other fundamental reasons also account for why Asia is better off today than in 2013. Among them:

- Larger foreign exchange (FX) reserves. The post-2013 steps taken by India and Indonesia have made a big difference — both countries have boosted their FX reserves by about 25%.1 Moreover, there is greater confidence in reform and policy agendas in India and Indonesia. Globally, China has the largest FX reserve at $3.7 trillion, while seven out of the 10 Asian countries outside of Japan have FX reserves that exceed that of the US.2

- Monetary easing flexibility. Subdued inflation risk is keeping the door open for many central banks to ease policy if necessary, mitigating concern about a Fed rate hike cycle constraining monetary easing in the region. In some cases in the past, high inflation in Asia prevented central banks from easing policy to support their economies. This was the case in 1994, when inflation was rising rapidly as asset prices were climbing. This time, however, inflation is expected to remain low in Asia, given weak commodity prices, early stage recoveries and ongoing structural reform agendas in major countries.

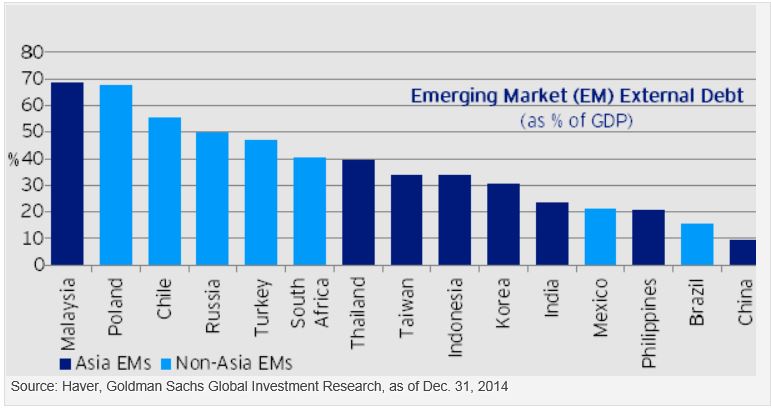

- Debt positions. When rates rise in the US, investors have historically tended to shift their money into US assets, drawing down their holdings in riskier developing economies. Only Indonesia and Malaysia have foreign holdings of local currency that are quite high.3 On the other hand, a high dependence on external funding can increase a country’s vulnerability to funding and currency risks. Excluding Hong Kong and Singapore — whose currencies are tied to the US dollar — and Malaysia, Asian countries have much less external debt exposure compared with most non-Asian emerging markets, as the chart below shows.

Asian markets in general have lower external debt

- Current account balance surpluses. Current account balances in Asia have also significantly improved since the US QE ended in the second half of 2013. India, Indonesia and Thailand were dealing with large deficits in 2013.4 While this is still the case in Indonesia and India, Indonesia’s current account deficit has narrowed from -3.2% of gross domestic product to -2.9%, while India’s went from -4.3% in 2012 to -1.1%.4 Out of the 10 Asian economies outside Japan, eight have current account surpluses.4

- Softening US dollar. The rise in German bond yields and concerns over the US economy have played roles in driving down the US dollar versus major currencies in recent months. Looking ahead, stabilizing oil prices and positive regional economic signs could keep lifting interest rates in the European Union, holding back US dollar strength. That’s definitely welcome news in Asia because a strong US dollar seldom bodes well for capital flows in the region.

Asian markets better positioned this time

While the environment of dollar strength has been in place since early July last year, Asian currencies have fared relatively well compared with their non-Asian peers. The primary drivers behind this have been:

- Positive policy and reform efforts in Asia.

- Improving economic fundamentals.

- Better trade terms, as most Asian countries are commodity importers.

- Lower external debt exposure.

Given significant improvements the past couple years in FX reserves, current account positions and policy flexibility, we’re confident Asian markets are better positioned to withstand any short-term deterioration in global sentiment when the Fed decides to hike rates.

For more extensive analysis, read the Insights titled Asia Much Better Positioned to Buffer Effects of Fed Tightening.

- Source: Bloomberg L.P., March 2015

- Source: TradingEconomics.com, March 2015

- Source: Morgan Stanley Research, March 2015

- Source: Haver, Goldman Sachs Global Investment Research, February 2015

Paul Chan

Investment Director and CIO

Asia Ex Japan

Paul Chan is a portfolio manager with Invesco.

Mr. Chan entered the industry in 1990 and joined Invesco in 2001 as an investment director and head of Hong Kong Pensions. Previously, he was deputy regional director at AIGIC (Asia) Limited, where he managed regional portfolios and chaired the regional stock selection committee. Prior to that, he held positions with William Mercer Limited (Singapore), Morgan Stanley Asset Management (Singapore) and Merrill Lynch Asset Management (Hong Kong) Limited.

Mr. Chan earned a BS degree in economics from the University of Manitoba. He is a CFA charterholder.

Read more blogs by Paul Chan on Invesco Blog

Important Information

Contagion is the likelihood that significant economic changes in one country will spread to other countries.

Quantitative easing (QE) is a monetary policy used by central banks to stimulate the economy when standard monetary policy has become ineffective.

Inflation is the rate at which the general price level for goods and services is increasing.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The performance of an investment concentrated in issuers of a certain region or country is expected to be closely tied to conditions within that region and to be more volatile than more geographically diversified investments.

The dollar value of foreign investments will be affected by changes in the exchange rates between the dollar and the currencies in which those investments are traded.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

| NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

Asia better positioned to handle a hike by Invesco Blog