“Economics is…a branch of…animal behavior.” – Walter L. Battaglia1

Behavioral finance is one of the great discoveries of our time, and the University of Chicago professor and

investment manager Richard Thaler is one of its principal discoverers. Misbehaving is Thaler’s

personal account of his discoveries, which influence the way assets are managed, policy is conducted and economic

theory is understood and taught.

Behavioral finance is the idea that investors do not act like the rational optimizers and profit maximizers that

neoclassical economics assumes them to be. (Behavioral economics, a related field also closely linked to Thaler,

studies irrational behavior in the real economy.)

Misbehaving is not an exceptional read. Thaler is not Michael Lewis or Peter Bernstein, weaving dry

concepts into magical prose. His book, constructed as a memoir, is workmanlike and informative with much to

recommend it. But the reader is unlikely to come away with a changed view of the world. Those interested in

revolutionizing their thinking on human behavior as it relates to investing should start with Daniel Kahneman’s

Thinking, Fast and Slow – a psychology book – and Hersh Shefrin’s Beyond Greed and

Fear, which delves deeply into the investment issues raised by behavioral finance.2 Read those

and add Thaler’s book as enrichment.

Misbehaving is one part personal history, one part brief against neoclassical economics, one part primer on

behavioral economics and finance and one part guide to practical applications. (The main applications are active

investment management, where investors’ predictable errors provide a framework for beating the market

and “nudge” policies, which are behavioral tricks intended to help people help themselves, for example

by saving more.) While Misbehaving does not hold together as a unitary book, it combines different aspects

of Thaler’s work into a single, accessible volume, and in that regard it succeeds.

A personal victory

Thaler’s journey through the economics profession was a curious one. As a young Ph.D. student, he attacked

head-on one of the most fundamental principles of conventional economics, the assumption that economic agents

(people) act rationally. Others who had taken this path did not get far. The late labor economist Sherwin Rosen,

unimpressed with Thaler, said, “We did not expect much of him.”3 Yet, some decades later,

Thaler ended up as president of the American Economics Association, the field’s most prestigious group. In

that sense behavioral economists have won – it has become socially acceptable to be one – despite the

persistence of the rationality assumption as the foundation of economic analysis.

Cognitive biases

Behavioral economics and behavioral finance are based on the observation that people do not process information

rationally. Instead, they suffer from cognitive biases, imperfections in processing that cause people to believe

things that aren’t true, misunderstand the consequences of even simple decisions and act against their own

interest. Thaler devotes several chapters to documenting these often amusing foibles.

For example, a plurality of people surveyed think that if they paid $20 for a bottle of wine, but it is now worth

$75, drinking the bottle costs them nothing (because they already paid for it), but dropping and breaking the bottle

costs them $75. If that is the best that people can do in assessing the costs and benefits of an action, no wonder

they misprice securities, invest in funds that have already gone up and fail to save enough for retirement! The

behavioral critique of rationality in economics and finance certainly has strong intuitive appeal.

Humans and econs

Thaler draws a sharp distinction between real people, who make mistakes – “humans” – and the

fictional agents of economic models, whom he calls econs.4 Econs are lightning-fast calculators who have

access to complete information about every situation, understand all of the ramifications of their decisions and

make each decision with an eye to maximizing utility, invoking a kind of enlightened selfishness.5 People

don’t behave like that, so it’s sensible to question what would happen to economic theories and

predictions if one drops the assumption that they do. That is the essence of Thaler’s contribution to

economics, and it’s a valuable one.

Yet Thaler overstates the faults of conventional economics. There may have been (and there still may be) economists

who believe that humans act like utility-maximizing genius robots, but I haven’t met one. More realistically,

economists tend to believe that economic models can be constructed as if people behave like econs, and that

such models are much more useful and accurately predictive than they would be if one had to drop the rationality

assumption. Without the rational-agent assumption, economics would be lost at sea, unable to make a prediction or a

policy recommendation – but that doesn’t mean the assumption is, or should be, realistic. A half-century

ago Milton Friedman famously argued that the test of a theory is the accuracy of its predictions, not the realism of

its assumptions, and that principle still holds.6

The “as if” critique, dismissed by Thaler, is actually relevant

Thaler, noting that he encountered the “as if” critique often in his early effort to persuade colleagues

of the behavioral view, is dismissive of it:7

One of the most prominent of the putdowns had only two words: “as if.” [T]he argument is that even if

people are not capable of…solving the complex problems that economists assume they can handle, they

behave “as if” they can… Even today, grunts of “as if” crop up in economics workshops

to dismiss results that do not support standard theoretical predictions.

While Thaler is dismissive of this concept, it deserves a fair hearing.

It is hard to overstate the beauty and power of neoclassical, rationality-based economics as an explanation for the

world as we see it (or “theory of everything”). Once you’ve grasped the importance of tradeoffs,

incentives, competition, cooperation, decision-making on the margin and so forth, you see these principles in

everything, including non-human realms such as biological evolution.8 Yet behavioral economics says that

the founding principles of conventional economics, especially the assumption of rationality, are, in some sense,

wrong. If that is the case, we can’t rely on the intuition provided by conventional economics, about the real

economy, financial markets or much of anything else.

For example, conventional (neoclassical) economics says that companies increase their production until the marginal

cost of a unit of production equals marginal revenue. By asking corporate managers, Thaler found that many companies

don’t even know that their marginal cost varies with the amount produced, nor do they maximize profits by

setting output at the optimal level. Instead, they try to sell the greatest number of units they possibly can.

Does behavioral economics, then, overturn this foundational idea, that companies set marginal cost equal to marginal

revenue? Yes and no. “Sell as much as you can” is a pretty good – not perfect – heuristic

for getting close to the profit-maximizing level of output because of the limits placed on “as much as you can”

by competitors’ production and pricing, alternative uses for the money and consumers’ limited ability to

pay. There will be some waste, some unsold goods, but not a lot! And there will be some waste with the marginal-cost

method, too, because of error in estimating the proper level of output.

At any rate, companies will learn pretty quickly not to make massive, repeated mistakes in determining output

because, if they do, investors will allocate capital elsewhere, driving the poorly-run company’s stock price

down or running the company out of business (which is exactly as it should be; markets are a machine for allocating

capital to its best use, unforgiving of poor management). The economy functions as if conventional

economics is its set of operating instructions, even if that isn’t precisely true.

From behavioral economics to behavioral finance

As Thaler points out, finance is the branch of economics where behavior is most likely to be rational because

financial markets tend to be liquid, transparent, deep, continuous and subject to arbitrage. Thus, it was in finance

that the discovery of behavioral anomalies was most surprising and most vigorously resisted.

Still, the anomalies are there, and there are many of them. Thaler recounts many anecdotes familiar to readers of

other behavioral finance literature. Among them are the stocks of 3Com and Palm, linked by crossholding, which were

priced in such a way that, by using a long-short strategy, 3Com could theoretically be purchased at a negative

price; the inconsistency of the prices of Royal Dutch and Shell, which are claims on the same corporate assets; the

existence and persistence of value and small-cap anomalies that violate the CAPM; and many others. By the time

Thaler is done, you would have to be immune to logical reasoning to believe that market prices, always and

everywhere, reflect fundamental value.

The dogmatism of (some) academics

But today’s investors are unlikely to appreciate the extent to which academics in the 1970s, when Thaler began

his quest, shut out all attempts to show how or why markets might be inefficient. As Thaler notes, most papers that

challenged efficient markets were rejected outright by prestigious journals, and the few that were accepted were

accompanied by “abject apologies [from the authors] for the results.”9 It was as though the

authors had announced to their preachers that they had ceased to believe in God.

It is right for the proponents of a good theory to defend it from flaky, flat-Earth attackers. But, in the case of

efficient versus inefficient markets, there were good arguments on both sides. The academic community should be

embarrassed by the long delay between Fama’s groundbreaking 1964 study showing that markets are likely to be

efficient and the wide acceptance of market efficiencies in the 1990s; it was one of the worst examples of

groupthink ever.10

Thaler and his behavioral compatriots, of course, had much to do with this shift in attitudes. Part of the shift

came from the persistence of well-trained academics, such as Thaler, in poking holes in efficient markets –

and part of it came from the obvious success of practitioners in exploiting inefficiencies, culminating in the

hedge-fund craze of the last 20 years.11 Readers interested in the history of financial thinking will

find Thaler’s account of this transition, and of his role in it, valuable.

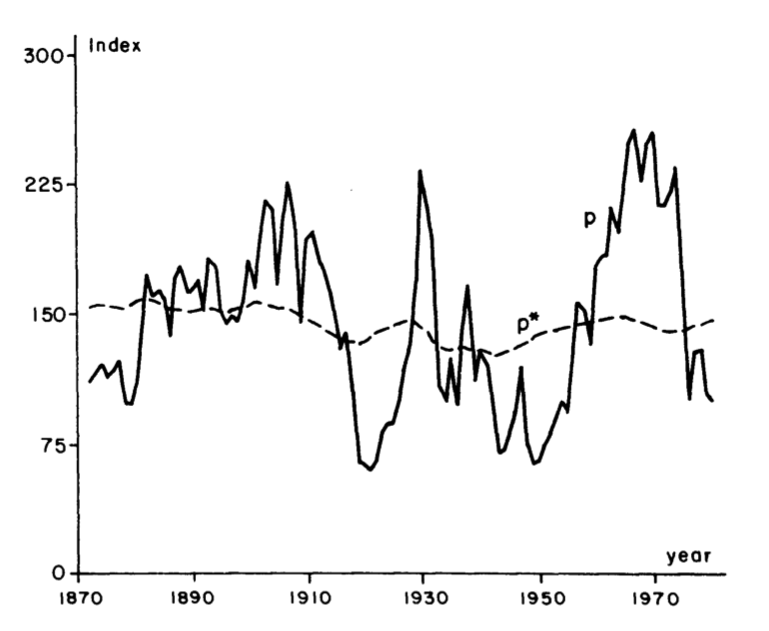

Beating the market

The beginnings of behavioral finance, and of Thaler’s story, rely heavily on Shiller’s [1981] finding

that stock indices fluctuate much more than can be justified by subsequent changes in fundamental

value.12 (See Exhibit 1, created by Shiller but reprinted in Misbehaving, comparing actual

levels of the S&P 500 with hypothetical fair values calculated by discounting all future dividend payments,

where the calculation is done as if those future dividends had been known with perfect foresight.13)

Do Stock Prices Move Too Much? Comparison of Detrended Real Stock Prices with Hypothetical Perfect-Foresight Prices

Based on Future Dividends, 1871-1979

Source: Shiller (1981), p. 422.

I believe that stocks fluctuate more than is justified by changes in fundamentals – the crash of 1987 is a

case in point – but Shiller’s argument is not a fully convincing one. Stock prices are present values

and, as such, are exquisitely sensitive to changes in both the discount rate (which Shiller’s study takes into

account) and the expected long-term growth rate (which it does not take into account). In the 1930s and, to

some extent, the 1970s, it looked as though economic and earnings growth would be permanently much lower than

before. In the 1960s and 1990s, growth was expected to be much higher than before. Nobody had perfect forecasts or

even tolerably good ones. Of course stock prices fluctuated more than they would have if good long-term growth

forecasts had been available!

Today, stock prices are fairly high while growth is widely expected to be slow. Should equity owners sell? I did,

prior to the crash of 2008, and I now regret my decision every time the market hits a new high. I’m also

afraid to get back in. It’s difficult to time the market, even if behavioral finance teaches us that the price

is not always right.

Value versus growth

If stock prices overreact to changes in information – a hypothesis strongly supported by Thaler – then

one should be a value investor. Good news causes a stock to become overpriced, even after taking into account the

increase in fundamental value caused by the news, and you should sell the stock; likewise, bad news causes a stock

to become underpriced and you should buy it. A value strategy will take advantage of this effect.

But Thaler also indicates that stock prices can underreact. If that is the case, then you should be a momentum

investor! The reason is that good news, not fully incorporated in the stock price, will cause the stock to rise

further after you’ve bought it.

So…which is it? The verdict seems to be that stock prices both overreact and underreact, and it’s hard

to tell which is which in any given situation. Stock prices, instead of being right all the time (the efficient

market hypothesis), will be wrong much of the time. If that is the case, you should mostly be a value investor since

wrong prices are a mixture of too high and too low, and value strategies overweight the low ones. This intuition has

been vindicated by decades of value-stock outperformance although the value effect is highly variable and cannot be

relied on in any short or even medium-length time period. Nor is there any assurance that the value advantage will

not be arbitraged away as more capital flows into such strategies.

Nudge

The last chapters of Misbehaving recap Thaler’s effort, with co-author Cass Sunstein, to help people

achieve their savings goals and otherwise improve their lives.14 This effort, labeled “libertarian

paternalism” by the authors, has begun to transform defined-contribution retirement savings. The idea is

counter to the top-down, regulatory impulse of government and seeks to improve people’s behavior as judged

according to their own criteria. This last part is important.

Behavioral scientists have discovered that small influences or “nudges” can have big results. An example

is Thaler and Benartzi’s [2004] “Save More TomorrowTM” plan which, in a test site, increased

employee savings for retirement from 3.5% to 13.6% in just four years by asking employees to commit to save part of

their future raises.15 Since the normal cost of a traditional pension is only 15% of payroll, this plan

could achieve the savings needed to help make DC plans work as well as DB plans (although the needed investment

return at a savings rate of 15% is higher than one can reasonably expect under current market conditions).

Other “nudges” are having similar success in other areas, such as getting taxpayers in the U.K. to pay

their taxes more promptly to avoid penalties. The idea is not new; the speed limit is basically a nudge, rarely

enforced but widely followed within a standard error of about 9 miles per hour. But libertarian paternalism, in an

era when government is not widely trusted but people desperately need help in achieving many different goals, is a

concept with promise.

Conclusion

Misbehaving is a welcome addition to the literature on behavioral economics and finance. Its benefit to

investors is indirect because it is a book on economic concepts, not investment strategy. Moreover, as a memoirist

telling a tale of scientific discovery, it helps to be a natural raconteur like the great Richard

Feynman.16 Thaler’s storytelling is drier and more matter-of-fact. But those wishing to round out

their general knowledge of important topics that affect investors will benefit from reading Misbehaving.

Read more articles by Laurence Siegel