MLPs Will Weather the Storm

Pullback Provides Attractive Entry Point for Patient Investors

After six years of strong returns, MLP stocks suffered a 20% correction from their August highs to their recent January lows. This correction, spurred by the significant decline in oil prices, surprised many investors given the toll-road nature of MLPs. So what happened? And what should investors do now?

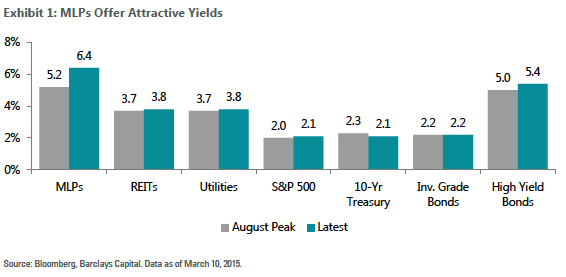

Years of surging share prices left MLP stocks with little margin for error. Over the past five years, MLP yields have ranged from 5% to 8% with an average of just over 6%. At the end of August 2014, the yield on the group had fallen to a record low of 5% and several high-fliers sported yields below 2% - lofty levels for yield-driven equities. These demanding valuations left MLPs vulnerable to a correction and the decline in oil prices injected volatility and concern into a sector that had seen little of either for many years.

As we begin 2015, this pullback has provided an attractive entry point for long-term investors who can stomach near-term volatility. The asset class has given back two years worth of gains and now offers attractive yields on both an absolute and relative basis. At 6.4% for the Alerian MLP Index, MLPs offer real yield in a world where attractive income is hard to come by.

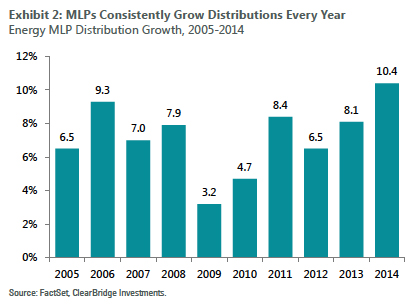

In the short term, MLP stocks may continue to fluctuate significantly. But, over the long term, MLP share prices will be driven by the companies’ fundamentals and their ability to grow distributions to investors. Despite the collapse in oil prices, we expect MLPs will continue to grow their distributions in 2015 and beyond – just as they have for the last ten years through ups and downs in the economy and the markets. MLPs even grew their distributions in 2009 during the depths of the financial crisis and during a time when oil fell from $140 per barrel to $40 per barrel. The pace of distribution growth will slow, just as it has during previous periods of turmoil, but we still expect distributions to grow.

As we put together our investment thesis for MLPs, it is important to remember that while oil dominates the headlines, it is not the only game in town. In fact, natural gas is actually the more important commodity for U.S. oil and gas producers, as gas constitutes 55% of total oil and gas production, compared to 37% for crude oil and 8% for natural gas liquids (NGLs), a resource that is found alongside oil and gas.

Generally speaking, MLPs get paid based on the volume of energy they handle, regardless of the price. So the key question to answer when underwriting an investment in MLPs is: what is likely to happen to production volumes over time? In spite of the decline in oil prices, we expect overall U.S. energy production to grow in 2015 and beyond. The drivers for oil and natural gas are different and the road for oil will be much bumpier, but we expect overall production volumes to grow over time.

Natural Gas Economics: Low-Cost Shale Gas Drives Higher Structural Demand for Gas

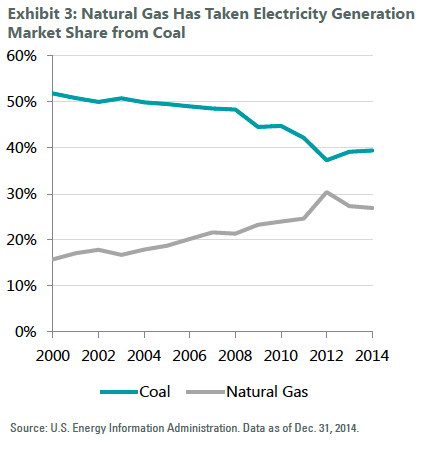

While today’s low oil prices have sparked concern about the outlook for the U.S. oil industry, it is precisely the advent of low-cost shale gas that makes the outlook for natural gas so robust. As the price of natural gas has declined, it has become cost competitive with coal as a fuel source for generating electricity. With competitive costs and a far better environmental profile than coal, natural gas has taken significant market share. Given America’s tremendous supply of low-cost natural gas and the environmental benefits of gas compared to coal, we expect this trend to continue.

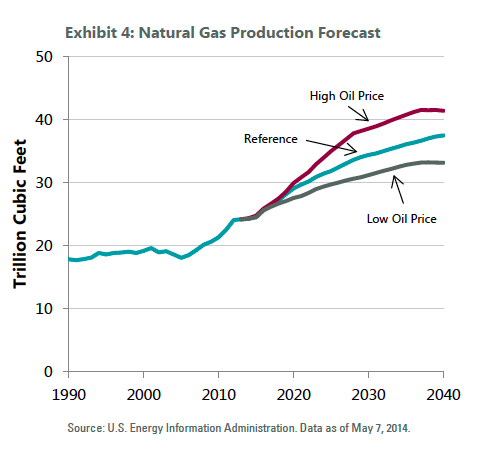

In addition to coal-to-gas switching, low-cost gas is driving renewed manufacturing activity and increased petro-chemical production, which further increase the demand for gas. And in a development that was unimaginable just a few years ago, shale gas has positioned the U.S. to become an exporter of natural gas in the form of liquefied natural gas (LNG). The first LNG export facility is set to come on line at the end of 2015 and others are expected to follow in the years ahead. The combination of all of these demand drivers results in a robust outlook for natural gas production regardless of the price of oil. This should also create strong growth for MLPs for years to come.

Thus, for natural gas, lower prices are actually driving increased demand for gas. Increased demand requires increased production and increased production means more infrastructure which will in turn drive growth for the midstream MLPs that ClearBridge favors.

Oil Economics: Framing Price Movements

While the recent short-term sell-off makes oil prices seem completely unpredictable and devoid of any underlying rhyme or reason, over the long term there is an underlying rationale to oil prices. Prices move within a range that at times of extreme surplus is driven down towards the cash cost of production and at times of extreme shortage is driven up towards the price which creates demand destruction. In the middle of this range lies the marginal cost of production – the price level which the market trends towards when supply and demand are in balance.

Today, the world is in a surplus position, which is driving prices towards the cash cost of production. The cash cost is a variable cost (e.g. it varies with the level of production) and excludes any overhead or sunk costs. Producers will not produce below their cash cost because they actually lose more money by producing that oil rather than just leaving it in the ground and doing nothing. Lower drilling activity reduces supply resulting in higher prices and a return to balance in the market.

The current oversupply resulted from the combination of strong U.S. production growth in 2012 (+15%), 2013 (+15%), and 2014 (+16%), and anemic demand growth due to the weak global economy. This left the oil market roughly 2 million barrels per day oversupplied against global demand of 92 million barrels per day. The magnitude of the oversupply is not particularly great. However, like all commodities, the marginal barrel sets the price of oil. With barrels struggling to find a home, pricing began to weaken in the back half of last year. From a recent peak of $107 per barrel, oil prices fell to a recent low of $45 per barrel.

Despite the perhaps exaggerated decline in the price of oil, self-correcting mechanisms are already starting to kick in. In just three months, the number of rigs drilling for oil in the U.S. has declined by 40% and will likely fall more in the coming weeks and months. Global rig counts are released with a lag, but they are likely falling along with the U.S. rig count. This will ultimately slow global oil production growth as new drilling is uneconomic at current oil prices in roughly two-thirds of global oil plays. Demand is also showing signs of life in the U.S. For example, gasoline demand is now clipping along at a 5% annual rate, a growth rate not seen since 2011.

During periods of imbalance in the industry, the market tends towards extremes. As prices hit these extremes, the market begins a self-correcting process that ultimately brings it into balance. In today’s environment, oil prices are below cash costs for many individual producers. These producers will shut in production thereby reducing the supply of oil. This reduction in supply will ultimately drive prices up and bring the market back into balance. Prices will rise until they reach the marginal cost of production at which point producers will begin to drill new wells because they can once again earn a sufficient return on that spend. Today, the global industry’s cash cost is about $40 per barrel and the level at which demand destruction sets in is around $150 per barrel. In the middle is the marginal cost of production at about $80-$100 per barrel.

As we think about the oil cycle, it is important to keep in mind that oil production from existing wells declines at about a 7%-8% annual rate, so new wells are constantly needed to replace the declining productivity of current wells. In a world that currently produces about 92 million barrels per day, that means adding 7 million barrels a day of new production each year just to keep production flat. As base production erodes and exploration activity is sharply curtailed, the oversupply will naturally cure itself.

Oil Economics: The Global Cost Curve

In previous periods of market surplus, Saudi Arabia, the world’s largest and lowest-cost oil producer, has reduced its production to maintain balance in the markets and thereby support oil prices. This time, the Saudis have maintained production levels, letting prices drop knowing that current low oil prices will drive higher-cost, less-profitable producers out of the market. Over time, the market will return to balance as these higher-cost producers are forced to shut down.

Below is a chart of the global cost curve which depicts the relative cost position of various oil-producing regions around the world. Specifically, it shows the price required for producers to break even in various geographies.

Saudi Arabia, the lowest-cost producer is at the left. Canadian Oil Sands, the world’s highest-cost producer, is at the right. The width of each column represents the amount of production for each resource. Saudia Arabia is able to produce about 10 million barrels a day and breakeven at prices as low as about $30 - whereas Russia is also able to produce about 10 million barrels but breaks even at a price of around $80.

There are several important takeaways from looking at the cost curve:

The current spot price of around $50 is unsustainable. At $50, only about 30 million barrels of production can break even. Global demand is around 92 million barrels a day, so this would result in a massive shortage of oil.

-

In order to meet global demand of 92 million barrels, the price will have to increase towards the marginal cost of production.

Canadian Oil Sands are the highest-cost producers in the world, putting them at serious risk for long-term capacity reductions and shutdown.

-

Many shale plays have breakeven levels well below $80 and therefore are likely to be active basins for the long term.

-

Russia, one of the largest producers in the world, is relatively high cost and thus is likely to see some market share loss as well.

U.S. conventional (non-shale) production is lower cost than Canadian Oil Sands but some portion of them could be backed out of the market over time.

-

Nobody can say with confidence, when this will work itself out. However, looking at the overall economics of the oil market, one can say with confidence that oil prices will ultimately recover.

Oil Economics: Understanding Where the U.S. Fits in the Global Cost Curve

As oil prices decline, oil producers rationalize their drilling activity. Companies will only drill wells that are economically attractive at the lower price levels, while suspending activity at those that require higher oil prices to make the math work.

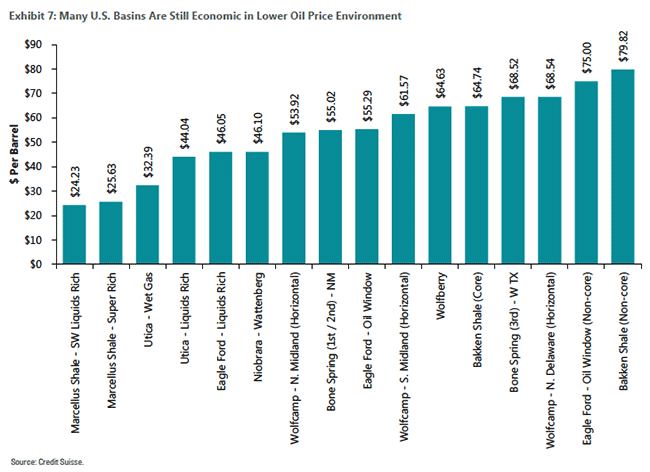

Taking a closer look at the cost curve within U.S. basins, one can see that many high-quality shale plays are still economical in the lower commodity price environment, which should help offset declining activity in the conventional plays that have fallen off the curve. U.S. drillers will be “high-grading” in this environment, focusing their money and their activity on their highest-return and most efficient acreage, while drastically reducing activity in their higher cost basins. This should help to maintain production levels as growth in their best areas offsets declines in other areas.

While fewer wells will be drilled in 2015 than in 2014, we do not expect oil production to decline for the year. Oil production should continue to increase because (1) there is a lag effect between when prices decline and drillers respond, (2) the run rate of production volumes at year end 2014 is substantially above the average for the year which provides a sizable cushion and (3) there are still a reasonable number of basins that are attractive at current prices. In fact, the Energy Information Administration projects U.S. crude production to increase to 9.3 and 9.5 million barrels per day in 2015 and 2016, respectively, compared to 8.7 million barrels per day in 2014.

The Outlook for 2015

MLPs will likely continue to remain volatile as long as oil prices remain depressed, and may not trade up significantly until oil prices stage a sustained recovery. We do not know when that will happen, but we know that it will happen. In the meantime, investors in MLPs get paid to wait with a current yield of 6.4% and the prospect for continued albeit slower growth. In spite of the significant decline in oil prices, we expect oil and gas production volumes in the U.S. to be up in 2015, driving continued growth for MLPs. For investors who can stomach short-term volatility, now is an attractive entry point for the asset class.

Putting the Current Oil Situation in a Historical Context

While studying history is always instructive, we do not believe that the current situation is directly comparable to the oil collapse of the 1980s or 2008/2009. The collapse of the 80s had its roots in the energy price shocks of the late 1970s. The surging price increases of the late 1970s caused global oil demand to fall by 8% from 1979 to 1985 (roughly 64 million barrels a day of demand in 1979 to 59 million barrels per day in 1985). At the same time, global oil production capacity moved higher, leaving the oil market oversupplied by approximately 16 million barrels per day (or 27% relative to demand). Oil prices subsequently plunged from $30 per barrel in 1985 to $10 per barrel in early 1986. Given the magnitude of the oversupply, oil prices did not regain $30 per barrel until 1990.

The current oil market is similar to that of 1985/86 in that the price decline was a result of oversupply. However, the magnitude of the oversupply in 1985 at 27% of demand is not comparable to the oversupply in 2014/15 at 2% of demand. Barring a deep and prolonged global recession, normalized demand growth for oil should alleviate most, if not all, of the current oversupply within a year or two.

In 2008/09, oil prices plunged from $140 per barrel to below $40 per barrel due to weakening demand given the global financial crisis. Global demand for oil declined by close to 2% in 2009. Yet, as should happen with oil economics, the oil price collapse spurred demand growth for oil. 2010 oil demand was up almost 4% over 2009. While oil prices never regained the previous $140 per barrel, they did more than double in 2009 and $100 per barrel was achieved 15 months later.

About the Authors

Michael Clarfeld, CFA

Managing Director, Portfolio Manager

- 14 years of investment industry experience

- Joined ClearBridge in 2006

- Member of the CFA Institute

- Member of the New York Society of Security Analysts

- BA in History from Duke University

Chris Eades

Managing Director, Portfolio Manager

- 22 years of investment industry experience

- Joined ClearBridge in 2007

- BA from Vanderbilt University

ClearBridge Investments

620 8th Avenue, New York, NY 10018

www.ClearBridge.com

Past performance is no guarantee of future results.

Copyright © 2015 ClearBridge Investments. All opinions and data included in this commentary are as of March 10, 2015 unless noted otherwise and are subject to change. Past performance is no guarantee of future results. The opinions and views expressed herein are of the ClearBridge Investments, LLC MLP portfolio management team and may differ from other managers, or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.