Misunderstanding Buffett

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn November 2013, Connecticut-based money management firm AQR published a paper considering how to construct a quantitative model emulating the way Warren Buffett has selected his investments and generated attractive long-term returns. As we believe AQR’s conclusions do not represent how Buffett actually invests, we considered how we might build a "Buffett model" in a different way.

AQR’s quantitative approach to Buffett-style investing

AQR’s Buffett model builds on a long lineage of research initiated by Eugene Fama and Kenneth French. The starting point of their work was the capital asset pricing model (CAPM) and the hypothesis that, because markets are efficient, greater returns can only be achieved by taking on greater risk. Risk in the CAPM — and to efficient-market adherents — is defined as beta, or the volatility of investment returns when compared to the market.

Fama and others noted outperformance in certain investment strategies that could not be explained solely through the use of beta, and so they searched for other factors that helped explain their observations. One of their findings was called the "value factor," which showed that by weighing companies with high ratios of book value (shareholders’ equity) to market value (market capitalization), one could explain a large portion of the excess returns. Another finding was that smaller companies tended to deliver higher returns than larger companies and that these excess returns could not be explained using beta alone.

Fama and others augmented the CAPM with the value and size factors to create a new "three-factor" model to better explain historical market returns. In their minds, there should be very few sustainable sources of outperformance against a benchmark constructed using these three factors.

One substantial challenge to their views, however, was that Buffett’s returns and the returns delivered by certain other value investors from the Graham-Dodd school of investing were persistently stronger than could be explained by the three-factor model. As a result, researchers at AQR attempted to augment the three-factor model to see if they could explain Berkshire Hathaway’s historical performance.

AQR’s Buffett model

AQR attempted to show that its Buffett model for weighting stocks, when deployed with 1.6X leverage, explains much of Berkshire Hathaway’s historical performance.

We will summarize four core attributes of the AQR model and contrast them with how we perceive Buffett actually invests, thus highlighting ways we think AQR’s model could be improved. The first attribute consists of Fama’s original "value" factor. The other three represent, in part, how these researchers augmented Fama’s three-factor model in an attempt to emulate Buffett’s returns. Our understanding of these four characteristics of the AQR model can be summarized as:

-

Value: The ratio of a company’s book value to its market value.

-

Quality: The composite of a variety of features, including profitability measured in multiple ways and the proportion of earnings paid out to shareholders, all viewed in the context of a company’s growth, volatility of returns and balance-sheet leverage. Companies with high marks on this composite are considered quality companies and are given positive weights in AQR’s simulated portfolios. Companies with low marks are considered junk companies and are given negative weights. This factor is termed quality minus junk.

-

Betting-Against-Beta: Building on research that suggests low-volatility stocks have produced higher risk-adjusted returns than high-volatility stocks, the AQR researchers adopted a factor termed “betting against beta.” In this context, companies with high betas (high volatility in their share prices) are given negative weights. Companies with low betas are given positive weights.

-

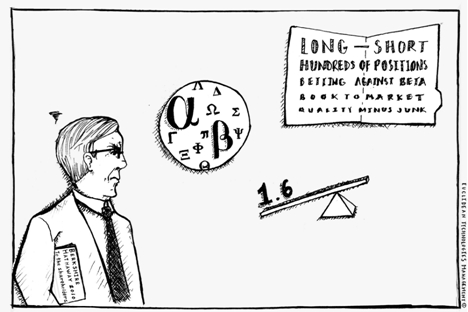

Leverage: Berkshire operates with leverage in the form of deferred taxes and low-cost insurance float. AQR found that if a model constructed on the above three factors is leveraged by 1.6, it would show similar historical returns to those realized by Berkshire Hathaway from 1976 to the present. AQR found Berkshire’s actual historical leverage to be generally consistent with 1.6X.

Using these attributes and several others, the AQR model constructs what would effectively be a long-short portfolio representing hundreds of positions. The AQR model would take a long-position in companies that earned a net positive weighting when using these factors. Other companies would have net negative weights across these factors, and AQR would be short those companies. These holdings would be periodically rebalanced to reflect companies’ shifting fundamentals and prices. When AQR calculates the returns this model would have achieved in the past, and amplifies them using 1.6X leverage, the AQR model shows estimated returns that resemble Berkshire’s superior record.

Our sense of how Buffett invests

We do not believe Buffett invests in the manner described by AQR. Moreover, we believe one could do very well with a model that reflects the qualities Buffett articulates in his letters to Berkshire Hathaway’s shareholders. Doing so might also address a potentially dangerous conclusion from the AQR paper: that one must lever-up a "Buffett-like" portfolio by 1.6X to do well over time.

Our hypothesis is this: Except when managing very large amounts of capital (as Berkshire now must do), one could demonstrate simulated returns approaching AQR’s results without the extreme leverage requirement. We’ll share our thoughts on how Buffett’s investment style differs from AQR’s assumptions, and then we’ll discuss how one could test this hypothesis.

Value

AQR’s value factor (the ratio of a company’s book value to market value) is a remarkably crude measure for assessing whether a company’s shares are being offered for more or less than they are worth. Perhaps this is why Buffett talks about book value as a measure of limited worth when estimating the intrinsic value of a business.1 After all, book value reveals very little about the operations of a company. It makes no distinction between a pile of cash and a company with productive assets, great products and loyal customers.

Instead, when evaluating intrinsic value, Buffett focuses on understanding the amount of cash that a business can generate and distribute to its owners. He calls this “owner earnings.” In Berkshire’s 1986 letter to shareholders, he writes:

These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges … less (c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. … Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since (c) must be a guess - and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes.

Because estimations of a company’s future owner earnings are always approximate and imprecise, Buffett repeatedly discusses the importance of looking for opportunities with wide margins of safety. In his 1992 letter, Buffett writes:

We insist on a margin of safety in our purchase price. If we calculate the value of a common stock to be only slightly higher than its price, we're not interested in buying. We believe this margin-of-safety principle, so strongly emphasized by Ben Graham, to be the cornerstone of investment success.

In our own research and simulations, we found that buying companies at very low prices in relation to their demonstrated earning power would have yielded better results than using book-to-market. Perhaps AQR’s Buffett model could become more robust by swapping the traditional Fama value factor for one that embraces the owner-earnings measure and margin-of-safety principle that Buffett describes as being at the core of his investment approach.

- “Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life. … We regularly report our per-share book value, an easily calculable number, though one of limited use. The limitations do not arise from our holdings of marketable securities, which are carried on our books at their current prices. Rather the inadequacies of book value have to do with the companies we control, whose values as stated on our books may be far different from their intrinsic values.” Berkshire Hathaway Owner’s Manual, Warren Buffett, June 1996.

Quality

When assessing the quality of a business, AQR employs quite a few metrics that collectively assess a company’s profitability, growth, safety and payout ratio. Buffett cares deeply about the quality of the businesses he owns, and we expect he would want to understand much of what AQR includes in its quality assessment.

We believe, however, that one does not need to take a “kitchen sink” approach to defining business quality and that doing so may actually dilute what is most important. In a 1992 letter to shareholders, Buffett seems to approach the question of business quality in a much simpler way:

Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return. The worst business to own is one that must, or will, do the opposite – that is, consistently employ ever-greater amounts of capital at very low rates of return.

In the context of thinking like an owner, we believe that Buffett cares deeply about the magnitude and resiliency of a company’s long-term return on capital. Return on capital is simply the relationship between the earnings a company generates and the amount of capital tied up in its business. For example, a company that can consistently deliver 20 cents for every $1 in capital employed would show a robust 20% return on capital. To Buffett, this would be a higher-quality business than another that delivered a lesser yield or showed deteriorating, or inconsistent, returns on capital. Moreover, this yield relationship between earnings and invested capital allows Buffett to view a prospective investment in relation to all other potential uses for capital, be it the purchase of real estate, a bond, shares in a public company, or — in his role as Berkshire’s CEO — the various operating divisions of Berkshire Hathaway.

In this context of return on capital, concepts in AQR’s model — such as a company’s payout ratio or its rate of growth — can be good or bad. From a long-term investor’s perspective, neither of these alternatives (to reinvest or pay out earnings) proves to be inherently better than the other. Instead, our research supports what common sense might suggest: A company is most effective when it deploys capital at the highest rate of return. That returns on capital trump growth and payout ratio in Buffett’s analysis seems to be supported by what Buffett wrote in 1984:

You should wish your earnings to be reinvested if they can be expected to earn high returns, and you should wish them paid to you if low returns are the likely outcome of reinvestment.

And in 1992:

Growth benefits investors only when the business in point can invest at incremental returns that are enticing - in other words, only when each dollar used to finance the growth creates over a dollar of long-term market value. In the case of a low return business requiring incremental funds, growth hurts the investor.

In a linear model, such as what AQR employs, growth and payout ratio are considered increasingly "good" as they increase in value. However, as Buffett describes, things are not so simple or linear. Perhaps exploring the non-linear relationships between measures of growth, payout ratio and profitability could yield powerful insights that would allow one to more closely emulate the trade-offs Buffett describes. At the very least, adopting a quality measure that focuses more directly on the persistency and magnitude of a company’s return on capital would reduce the complexity of the AQR model while also increasing alignment with Buffett’s investment style.

Beta as risk

We doubt Buffett employs a "betting-against-beta" strategy or that he even considers the beta of a stock when investing. Buffett thinks like a business owner. Whether he owns 100% of a company or just a few shares, his mindset is that he has a claim on the long-term economics of that business. Thus, for Buffett, beta — the relative volatility of a company’s share price — matters only in the sense that it reflects the stock market’s tendency to periodically provide opportunities to purchase good companies at attractive prices.

This view is well articulated in the section titled Common Stock Investments in his 1993 letter to Berkshire’s shareholders. We excerpt a small section here but encourage you to read the section in its entirety.

Academics, however, like to define investment "risk" differently, averring that it is the relative volatility of a stock or portfolio of stocks - that is, their volatility as compared to that of a large universe of stocks. … For owners of a business - and that's the way we think of shareholders - the academics' definition of risk is far off the mark, so much so that it produces absurdities. For example, under beta-based theory, a stock that has dropped very sharply compared to the market - as had the Washington Post when we bought it in 1973 - becomes "riskier" at the lower price than it was at the higher price. Would that description have then made any sense to someone who was offered the entire company at a vastly-reduced price?

In fact, the true investor welcomes volatility … a wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses. It is impossible to see how the availability of such prices can be thought of as increasing the hazards for an investor who is totally free to either ignore the market or exploit its folly.

With these words and his allusions to Benjamin Graham’s Mr. Market2 over the decades, our sense is that any true effort to model Buffett’s investment activity must exclude beta when evaluating potential investments. Price volatility has meaning to Buffett only when the market provides the opportunity to either buy a quality company at such a discount that there is an acceptable a margin of safety or sell a company at a fulsome price. Those opportunities are already captured in the interplay between the concepts of value and quality previously discussed.

- See Letter to Berkshire Shareholders, Warren Buffett, 1987.

Long-short portfolio construction and 1.6X leverage

The AQR paper explains that the long-only back-test of the company’s Buffett model shows worse performance than the long-short construction. The implication is that, in order to replicate the results of the AQR model, you would need to manage a portfolio that has hundreds of positions, both long and short.

But what could be further from how Buffett invests? We see no evidence in his letters that Buffett has established short positions. Instead, we find that he has done well with a fairly concentrated long-only portfolio of wholly and partially owned companies. In this context, AQR’s approach has engineered a replication of Buffett’s performance that seems to materially deviate from the cause-and-effect relationship underlying Buffett’s long-term success, which could be summarized asselective and sustained investing in good companies, when offered at low prices, yields good long-term investment results.

Adding to this concern is the big difference between the relatively low-risk leverage Berkshire enjoys with insurance float or deferred income taxes and the high-risk leverage that comes when investing on margin. If, in fact, one must invest in public stocks with 1.6X leverage to achieve Buffett-style returns, then attempting to execute on AQR’s findings seems like a risky proposition in any respect. Buffett sums this point up well in his 2010 letter:

Unquestionably, some people have become very rich through the use of borrowed money. However, that's also been a way to get very poor. When leverage works, it magnifies your gains. Your spouse thinks you're clever, and your neighbors get envious. But leverage is addictive. Once having profited from its wonders, very few people retreat to more conservative practices. And as we all learned in third grade - and some relearned in 2008 - any series of positive numbers, however impressive the numbers may be, evaporates when multiplied by a single zero. History tells us that leverage all too often produces zeroes, even when it is employed by very smart people.

We believe that if AQR more closely modeled how Buffett invests, it would not need to use 1.6X leverage to demonstrate the returns it seeks, at least not until the fund had an amount of capital approaching Berkshire's (currently in excess of $200 billion) to manage and compound. It is important to remember that Buffett did quite well as an investor without leverage during the 1950s, 60s and early 70s — the days of the Berkshire Partnership and before Berkshire Hathaway had a substantial insurance operation providing the relatively low-risk leverage Berkshire has more recently employed.

Another way to build a Buffett model

When seeking insight from historical data, keep in mind the difference between correlation and causation. Quantitative analysis yields sustainable insight only when it identifies explainable cause-and-effect relationships that are likely to persist into the future. Buffett has provided an incredible body of work in his letters to investors regarding how he invests. The concepts at the core of his approach include owner-earnings, margin-of-safety, Mr. Market, return on capital and low-risk approaches to leverage. These concepts have enabled him to find good companies offered at good prices and deliver strong long-term investment returns.

If you believe that the future will resemble the past such that one could do well by pursuing the same cause-and-effect relationships underlying Buffett’s long-term success, then crafting your investment style after his makes sense. It seems, however, that the AQR approach deviates very far from Buffett’s investment principles.

We believe one can borrow from Buffett’s methodology to create successful approaches to systematic investing. We propose an alternative characterized by the following differences from the AQR model:

-

We would begin with the principles of intrinsic value, margin of safety and return on capital that most closely align with Buffett’s well-documented investment philosophy.

-

We would use more sophisticated tools than the linear regression techniques employed by AQR. Today, tools like machine learning allow for exploration of a much larger universe of both linear and non-linear models. These tools allow for the possibility of finding models that better emulate the subtleties of Buffett-style investing. For example, as shown earlier, Buffett writes in his letters that growth and payout ratio are not necessarily good or bad, with the answer depending on the context of the company’s returns on capital. Non-linear models provide the flexibility to find subtle but potentially crucial trade-offs between a company’s various operating qualities that Buffett may have found helpful when investing.

-

We would make a greater effort to verify the cause-and-effect relationships underlying our results. To this end, we would perform out-of-sample testing to validate that the factors and models that appear successful during one period of history are not the result of chance correlations. Much like in school, the goal should not be memorizing answers to specific questions. Rather, it should be the comprehension of important principles that allow one to solve future problems. By learning the best way to express Buffett’s investment principles on a subset of companies from the past and then testing those insights on new companies, we would evaluate whether we found random correlations in the data that are unlikely to persist or whether we were on track to uncover the seemingly timeless cause-and-effect relationships underlying Buffett’s long-term success.

We believe that by embracing these qualities, one can construct a system that more closely emulates the timeless principles underlying Buffett’s success and have a more robust, and less risky, basis for achieving attractive long-term returns.

Mike Seckler and John Alberg are the managers and founders of Euclidean Technologies Management, an investment firm that applies machine learning and systematic approaches to value investing. John and Mike have worked together for over 18 years: prior to starting Euclidean in 2008, John and Mike co-founded Employease, a software-as-a-service provider that was acquired by Automatic Data Processing (NASDAQ:ADP) in 2006.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All