Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

How do you drive a market-timer nuts? Remind them of the evidence against them. That is, the evidence of shifting and even reversing correlations between stock and bond returns that make it improbable - if not impossible - to use market timing to make profitable investment decisions.

Market timing is a fool’s game – academic research proves that. But journalists have to write about something, and anything that appears current will likely pass muster for a busy editor’s review. Reporters continually seek out opinions on the latest ups or downs of the market. Their questions are typically in the vein of, “Why is the market doing this or that? What are advisors doing about it? Does this tell us anything about the future?”

It is not difficult to find a wide variety of answers to those questions. For those who understand a little about probability theory, it is amusing to listen to the prognostications of active managers speculating why the coin turned up heads this quarter instead of tails. They are trying to explain random events – it is no wonder they have a hard time.

This is why market timing has always been, is and always will be a losing investment strategy for the long term.

To be a successful market-timer, you must not only predict what will happen but also when it will happen. For example, almost everyone agrees that interest rates will go up, but no one can accurately say when. Even economists who are willing to go on the record have a hard time predicting rates with accuracy (see this study).

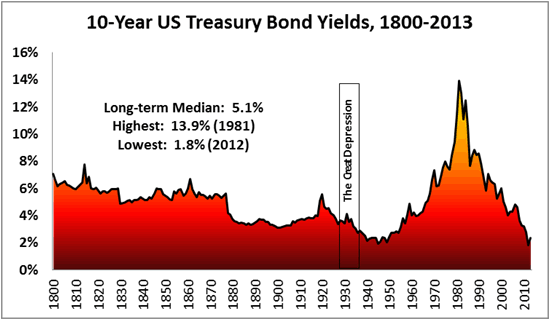

It is easy to see why rates are expected to rise – they cannot go much lower. Figure 1 shows the very long-term behavior of 10-year Treasury yields dating back to 1800. The past 30 years or so have provided great returns to bond investors, as rates fell from historic highs to historic lows. Since zero is the bottom line, we know that rates must rise (or at least not fall).

Figure 1

The price of fixed-rate bonds held in funds will fall as the rates rise, so total returns will never match what they earned over the past 30 years. All should beware any research based on the last 25 or 30 years when it comes to active bond trading. As PIMCO’s Bill Gross first mentioned in 2009, this “new normal” has and will continue to cause angst among active bond-fund managers. Because of the predicted continuing malaise of the global economy (see this study or this paper by the IMF), Gross’ catchphrase has morphed into “new neutral” due to what appears to be a global economic slow-down.

Given the volatility of cash flows into and out of bond funds in the past year, many investors are clearly puzzled as well. Some did not wait for rates to rise and got out before the market inflicted damage. Bond fund managers have been able to stay in business thanks largely to blind allegiance to modern portfolio theory (“Thou shalt have Y percent in bonds”) and their own marketing prowess.

But salesmanship will face a steeper uphill battle once rates begin to rise. Market-timers will have higher hurdles to jump, forcing active bond fund managers to scour the markets any way they can to stem their losses (which typically means speculating in riskier debt instruments).

Why has market timing become even more difficult than in the past? Part of the answer stems from the inherent unpredictability of the correlation between bond and stock returns.

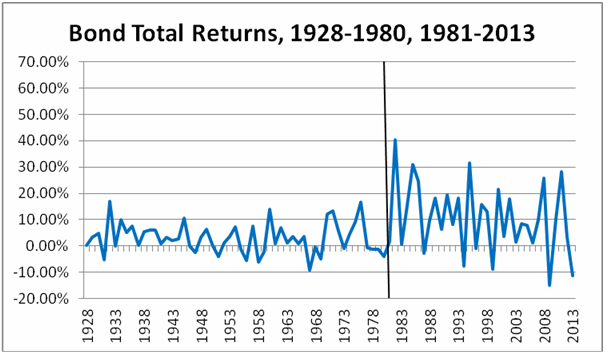

Figure 2 shows total returns for bonds (which includes appreciation or depreciation each year due to price changes) back to 1928 (published annually by Ibbotson). As can be seen, total returns for bonds rose to higher levels beginning in the early 1980’s due to the relatively steep decline in rates over the past 30 years. Total returns averaged 2.9% from 1928 to 1980, but increased to 10.5% in 1981-2013. Most bond funds in existence today were started after 1980.

But along with a higher average, bond returns became much more volatile after 1980. From 1928-80, the standard deviation was about 5.7% (maximum 16.8%, minimum -9.2%). But from 1981 to 2013, the standard deviation more than doubled to 13.1% (maximum 40.6%, minimum -14.9%). The difference in volatility before and after 1980 can be clearly seen in Figure 2.

Figure 2

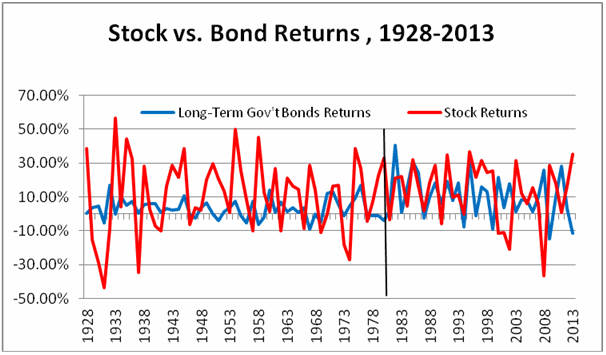

Figure 3 overlays Figure 2 with a chart of long-term equity returns (CRSP Total Market Index). It is clear that stock volatility has not changed much over time. But the change in the pattern of bond returns is much more evident. Indeed, they became nearly as volatile as stocks. From 1928 to 1980, the standard deviation for returns on bonds was 5.7%, stocks, 22.1%. But from 1981-2013, the standard deviation for bond returns was 13.2%, stocks, 17.4%. That means bond returns jumped from being only about 26% as volatile as stocks to being 76% as volatile – nearly tripling its relative volatility. In hindsight, this higher volatility is pretty clear, but at the time, few people recognized it. Bond funds were still sold as the “safe” investments.

A very discerning observer will note something else in Figure 3. The correlation between bond and stock returns from 1981-95 was positive. But starting about 1995, this pattern reversed itself. Returns began to move in opposite directions: Increases in stock returns correlated with decreases in bond returns. This reversal again created problems for market-timers who rely on repeating patterns, not changing patterns.

Figure 3

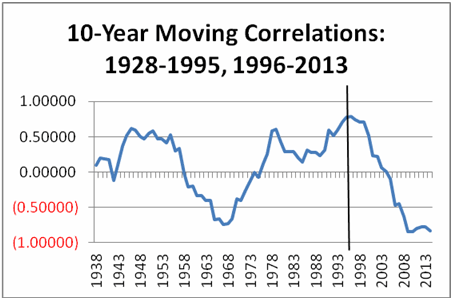

Let’s look at the correlation between stock and bond returns directly. The long-term average correlation from 1928 to 2013 is very low, clocking in at -2% (from 1928-2011, it was 0). But Figure 4 plots the correlations over all 10-year rolling periods back to 1928 and reveals that they actually followed a meandering pattern over time.

This is one reason why successful market-timing based on those variables has always been elusive. From 1975, the correlation between stock and bond returns turned positive and remained positive, reaching a peak in 1995 of about 79%. This is a strong positive correlation. But in 1995, the correlation began to drop dramatically, and they turned negative in 2004. This is a reflection of the reversal of movements discussed above. The correlation remained negative and averaged about -81% in 2008-2013. When will the correlation again begin to reverse itself? Nobody knows.

Figure 4

Given the ever-changing nature of the relationships between stocks and bonds, is it any wonder that “experts” are having a hard time making sense of where the market is headed in the next quarter? Is it any wonder that bond fund managers – trying to save their jobs – are getting more desperate by opening alternate or “unconstrained” bond funds that can invest in nearly anything? Passive managers must be chuckling among themselves.

Investing in the long run is best served by a passive strategy that buys index funds and holds onto them as part of an overall lifetime financial plan. Financial planners have been saying that for a long, long time.

Stephen J. Huxley, Ph.D., is chief investment strategist and Brent Burns is president of Asset Dedication, LLC, a registered investment adviser located in San Francisco, CA.

Read more articles by Stephen Huxley, Brent Burns