The strategic and tactical rigidity underlying modern portfolio theory (MPT) contributed to huge losses during the 2008 financial crisis. Diversification is the only MPT risk management technique, but diversification weakens as the need to be defensive increases, and it is at odds with striving for superior portfolio growth.

Defensive position rotation (DPR) is an alternative portfolio-construction philosophy that adapts to changing market conditions and can increase risk-adjusted returns over time. Two portfolio risk-management methods of DPR (“just-in-time” and “just-in-case”) preserve capital in down markets and avoid or hedge underperforming positions in up markets. This improves portfolio efficiency, as represented by higher Sharpe ratios. The potentially superior results of DPR allow portfolios to be judged by absolute-return performance standards: the intuitive standard used by most clients.

DPR tools and funds can help clients make higher-efficiency investment choices in the face of fears about past portfolio performance and future macroeconomic uncertainty.

I will review the failings of MPT and how DPR addresses them, and then describe how advisors can implement a DPR-based strategy on their own.

Modern portfolio theory and portfolio efficiency

In the realm of human activity, we widely observe adaptation to changing conditions. People use umbrellas when it begins to rain. Cars require frequent changes in spark timing, fuel-to-air ratio, valve timing, etc., to increase motor efficiency amid changing driving conditions . But I have not observed adaptive phenomena in the application of modern portfolio theory (MPT) to the management of portfolios of securities.

The rigidity of MPT, which requires a static asset allocation with periodic rebalancing and no adaptation to changing economic or market conditions, is based on the assumption that price changes of securities are random and can’t be predicted. MPT is based on statistical functions that do not include the time domain. Trends, if they exist, can’t be detected.

Without the ability to predict future prices or even to make an educated guess, MPT followers are left with diversification through asset allocation as the only risk-management tool. Asset allocation is only effective in protecting portfolios in times of dramatic market declines if asset classes demonstrate low correlation (independence of price movement). Since correlations may become very high during these dangerous times, protection is limited at the very time it is most needed.

While MPT’s goal is to generate market returns (for a given level of risk), diversification may limit (or even be a drag on) returns. A portfolio’s return is a weighted average of the returns of all the assets held. One way to improve average returns is to jettison under-performing assets. In MPT, this will not happen, because diversification is the foundation of the approach and is a justification for holding assets that are underperforming. Put differently, the MPT risk-management technique (diversification) can be at odds with striving for higher growth.

MPT’s fundamental assumptions of rational investor behavior (based on the efficient market hypothesis) are undermined by findings in behavioral finance showing that investors can be far from rational.

Defensive position rotation

As an advisor, I observed the loss of client wealth in the 2008 market decline, while I dutifully continued to rebalance their MPT-based asset-allocation portfolios. I had been using prudently asset-diversified and valuation-observant portfolios, but the crisis made a mockery of the entire process. As client wealth vanished, my clients (and I) questioned what I knew about guiding and protecting clients’ finances.

After the crisis, my concerns over market, interest-rate and purchasing-power risk (inflation) led me to an MPT-alternative: defensive position rotation (DPR).

DPR contrasts with MPT because it takes an active approach to capital protection. It is more sophisticated than MPT and may not be for everyone. Instead of relying on low correlations among assets, DPR addresses protection by adopting active methods, such as tactical flexibility, to preserve capital during declining markets. The emphasis is on how risk-adjusted returns are changing as the investment environment changes.

Efficiency, a measurable concept, describes how well inputs (time, effort, cost, etc.) achieve a task or output. Miles-per-gallon is an efficiency measure. For investment performance, a common measure of efficiency is the Sharpe ratio, which measures the excess return per unit of risk. DPR’s dynamic approach, which frequently revisits assumptions and allocations, has the potential to raise investment efficiency by giving greater return per unit of volatility (higher Sharpe ratios).

DPR can take several different forms. I’ll discuss two of the dominant ones: just-in-time and just-in-case.

Just-in-time protection

Just-in-time DPR protection is based on the assumption that price changes can have momentum and may be predictable. It says that market momentum, together with volatility, can be analyzed and may be predictive of future price movements.

This requires extracting signals from noisy market data. A brief summary of the price-momentum effect and its efficacy can be found in “Momentum in financial markets: Why Newton was wrong.”1 More detailed evidence of price momentum was presented by Narasimhan Jegadeesh and Sheridan Titman2 in a Columbine Capital white paper.

In contrast to MPT, which uses diversification to minimize risk, just-in-time DPR attempts to reduce risk by using quantitative analysis to avoid investing in losers and to move to defensive positions when no winners seem available. DPR investors seek to reduce losses during the worst periods of market loss, instead of staying invested through MPT’s policy of buy-and-hold. Capital preservation is a top priority for DPR.

Significantly increased efficiency is obtained by holding cash or otherwise defensive positions during market downturns. By emphasizing capital protection, DPR portfolios are more conservative as markets decline and more aggressive as markets improve. In essence, risk management is the major focus in DPR. DPR also does a good job of growing wealth through market cycles because steadier, less volatile returns compound more efficiently. Thus, risk management and growth are not at odds in DPR as they may be in MPT.

Just-in-time DPR is not market timing. DPR can be successfully implemented, while consistently timing the market is impossible. A quantitatively determined decision to enter or exit a market (or otherwise adapt to changing market conditions) is made after the market has turned. The current data after the turn leads to the trading decision. There is no attempt to anticipate the top or bottom of a cycle in advance. The strategy is trend-following rather than trend-predictive.

If price changes are random (as MPT assumes) and entry and exit decisions are made randomly, then the number of correct decisions will equal the number of incorrect decisions (or worse, if the decisions are based on emotions). The tactical methods used in a DPR-type portfolio are effective because the percentage of correct decisions is significantly greater than the percentage of incorrect decisions. A 2012 article by Jerry Miccolis and Marina Goodman presents an excellent example (dynamic asset allocation) of a just-in-time DPR strategy.3 Jeff Knight discussed another example based on risk parity.

Just-in-case protection

Just-in-case DPR protects portfolios in the event something bad happens. This is generally referred to as hedging: taking a position in one market to offset the risk of a position in another market.

In MPT, asset allocation uses hedging in the sense that different asset classes are chosen for their low correlations. In times of crisis, this may be too much to expect, as we saw in 2008. With just-in-case DPR, the hedge is chosen for its assumed strong negative correlation to the imperiled portfolio position. Its effectiveness depends on the strength of the negative correlation when the hedge is needed and on the cost of the hedge. Fund managers hedge in a just-in-time fashion: They increase the hedge in times when indicators are negative and reduce it when indicators are positive.

Many instruments can be used to hedge a portfolio position, including stocks, exchange-traded funds (ETFs), swaps, options, derivative products and futures contracts. Perhaps the most common are options-based hedges. A hedge may not work as intended if there is a mismatch between a portfolio position and its hedge, or if the hedge requires significant leverage. True hedging is conservative and is designed to reduce risk. It is not speculative investing and is more like buying insurance.

Measuring performance: Absolute return

With style-pure funds (the vast majority of funds), managers are obligated to stay invested in a benchmark-centric allocation. They generally have little flexibility to adapt to changing market conditions or use hedging techniques. Performance and risk management are measured relative to the benchmark in all markets. Thus, if the market declines 50% and, say, an equity-growth fund declines 20%, managers will celebrate, even though investors have suffered a 20% loss. This is not a client-oriented approach.

In contrast, DPR’s philosophy uses flexible risk-management techniques to reduce losses in declining markets and avoid underperforming positions in rising markets. This aligns with investors’ desires, because losses matter to investors.

DPR performance is measured by absolute returns, based on the rate of return over a relatively short period of, say, three to four years, regardless of market conditions. Successful absolute-return funds are, necessarily, managed using the DPR-type philosophy. This is the only way to meet performance targets regardless of market conditions. It is impossible to meet absolute-return goals using MPT strategies, so MPT managers don’t try.

When meeting with representatives of MPT-based funds, I have noticed an increased emphasis on up- and down-capture ratios. This may be a response to the poor performance of many style-pure funds in the 2008 financial crisis. Drawing attention to these ratios is a way to show that a fund manager is trying to distinguish between being aggressive and defensive, despite having a high correlation to a market benchmark. Successful DPR funds attain better long-term performance not by having wonderful up-capture ratios, but by having exceptionally low down-capture ratios. This reflects their emphasis on protecting capital and underscores the fact that protecting for downside risk compounds growth more effectively over time.

Most MPT portfolios fare decently in secular bull markets (e.g., 1980-2000), but in secular bear markets (2000 to present), it is like planting spring crops in the winter: Lots of waiting is necessary. The secular bear market may continue (and another equity bubble may pop), but absolute-return strategies (DPR) will better serve clients whose definition of the long run is more time than they are willing to wait.

This is especially true for clients who are close to retirement. Negative returns expose them to sequence of returns risk. Traditional retirement-portfolio advice is based on MPT and the belief that the best estimate of future returns is the long-term average of investments, without any consideration about whether markets are relatively cheap or expensive at the moment. There is strong evidence that future returns will be lower when starting valuations are high, and vice versa.

For a new retiree, DPR can lower the probability of not running out of money. For example, using MPT, a person retiring in early 2000 (when valuations were high) would be given the same asset-allocation portfolio as a similar person retiring in early 2003 (when valuations were low), despite the fact that they faced very different futures and outcomes in retirement. Using DPR to design a retirement portfolio can reduce this problem because the strategy continuously considers market valuations and where they are likely headed.

Managing a portfolio versus a mutual fund

Mutual funds are usually the main ingredient in an MPT portfolio. Let’s say an asset allocation calls for a position in large-cap value (LCV). One wants the LCV fund in this space to be pure, containing no bonds, real estate, commodities, cash, etc. This is why most funds are style-pure. The widespread availability of style-pure mutual funds is one reason it is easier to construct a portfolio using MPT than DPR. In MPT, the style-pure mutual fund ingredients and the asset allocation recipe are made for each other. Implementing buy-and-hold and diversification strategies through asset allocation is not difficult.

On the other hand, it is harder to manage a just-in-time DPR portfolio using style-pure funds. Remember the two key DPR principles: avoiding underperforming positions (losers) and taking defensive positions in weak or declining markets. Avoiding losers could involve a sector or style rotation. Moving to a cash or defensive position and back again when appropriate is difficult. So many people fail at it that the practice is generally considered dangerous and ill advised. Style-pure mutual funds will rarely take a defensive stance (e.g., move to cash) to become more conservative, even if doing so would improve performance.

How, then, does the advisor implement the second key principle of DPR? The answer lies in two complementary directions:

- From a simplicity standpoint, few mutual funds apply the DPR philosophy, but some do. Those funds that do try to increase their Sharpe ratios by avoiding losers and by being appropriately defensive and protecting capital in down markets. Thus, an advisor who wants to partially or completely leave MPT but still use mutual funds now has an opportunity to do so.

- From a flexibility standpoint, I found that there are numerous technical analysis tools capable of implementing DPR principles, including MetaStock, TradeStation, FastTrack, SectorSurfer and others. While implementation of DPR typically requires writing custom algorithm scripts, selecting trading indicators and manually tuning indicator parameters, this tedious task is automated by some of these tools. SectorSurfer’s design inherently supports DPR principles by automatically selecting the single best-trending security (of up to 12 securities) to own at any given time during rising markets indicating when to move to cash as a defensive position in the event of declining market. This approach allows the use of style-pure funds in a DPR portfolio and can produce impressive alpha and Sharpe metrics. Prudent investing generally requires diversification. This method of sequentially owning the one best position at a given time is called serial diversification.

Applying DR for client portfolios

The advisor’s job is to manage portfolios and clients, both of which are harder to do now than before 2008. The fear that came with 2008 experience is still vivid in clients’ minds. Behavioral economics reveals that this fear leads clients to perceive risk as higher than it is and to take actions that are contrary to their long-term goals. Meir Statman explained this phenomenon in detail.4

I have found that explaining DPR to fearful clients helps them take actions that are consistent with their long-term goals. There are three reasons for this positive outcome:

- DPR gives clients more confidence in the portfolio-management process, because it is common sense to adapt to changing market conditions.

- DPR portfolios do not resemble MPT-assembled rigid portfolios of style-pure funds that led to client fear in the post-2008 environment.

- The absolute-return performance standard of DPR is consistent with the intuitive standard used by most clients.

I have used DPR funds and the SectorSurfer tool for the last four years with good results, although I don’t recommended it for everyone because of its complexity. I diversify among funds to find the correct return-risk balance for each client. My clients are pleased and relieved to know that in times of large market declines they may be protected more than they were in 2008 and that over time they will not be holding underperforming asset classes for the sake of diversification. This transition to DPR requires client education, especially for those who are devoted to high-alpha performance in strong bull markets.

Illustration A is a scatter diagram showing return and risk characteristics for a number of common benchmarks. The diagram is for the five-year period ending June 29, 2012, so it fully includes the market drop of the 2008 crisis and the subsequent bull market. The shaded oval represents the general location of the DPR funds that I use, and the non-shaded oval encompasses the location of some popular balanced funds based on MPT. The DPR funds are generally to the northwest of the traditional funds and benchmarks because their Sharpe ratios are higher than style-pure funds. I generally try to use DPR funds that have Sharpe ratios close to 1 or higher.

Illustration A

Comparing Risk/Return Characteristics

MODERN PORTFOLIO THEORY Balanced Funds and Benchmarks

DEFENSIVE POSITION ROTATION (shading)

Based on 5 Years ending 6/29/2012 (to fullyinclude the 2008 market drop)

Illustration A shows the benefits of effective implementation of DPR philosophy and the potential for increasing investing efficiency. Some investors who used MPT during and after the crisis may have recovered what they lost in the downturn. The lower efficiency of MPT may mean that they would be better off today had they not experienced such a large decline.

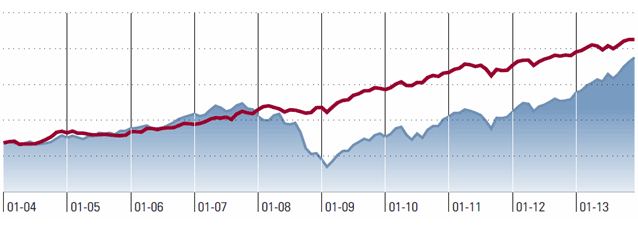

Illustration B shows a 10-year (2004-13) comparison of the S&P 500 total-return index (blue) and a portfolio (red) of eight, equally weighted DPR mutual funds. The illustration was created in Morningstar Advisor Workstation (MAW). The portfolio results are net of a 1% asset management fee. This illustrates the lower volatility using DPR philosophy. Illustration B does not represent back-testing, since MAW does not allow this. The illustration shows what might have happened if I had implemented DPR with mutual funds starting in 2004. (Securities-licensed readers may request a list of DPR mutual funds I have compiled by contacting me at [email protected].)

Illustration B

|

|

Portfolio |

SP500 |

Annualized Return |

8.27% |

7.41% |

Standard Deviation |

6.38% |

14.62% |

Sharpe Ratio |

1.05 |

0.47 |

There are a variety of online technical analysis tools available to advisors who want to implement DPR using traditional funds or stocks and ETFs. Here is a brief list: MetaStock, TradeStation, FastTrack, SectorSurfer and imarketsignals.

The mutual-fund industry is creating new DPR-type funds, recognizing that too many clients lost faith in industry doctrine after their experience in 2008. These DPR funds, the DPR on-line analysis tools mentioned and the innovations to come will be influential in changing the practice of retail portfolio management. They will make advisors’ portfolio-management services more client-centered, client-friendly and financially effective, because adapting to dynamic challenges is a positive part of human nature.

Dale van Metre is a registered representative advisor with Ameriprise Financial Services Inc. and a member of FINRA and SIPC.

The views expressed here reflect the views of Dale Van Metre as of May 27, 2014. These views may change as market or other conditions change. Actual investments or investment decisions made by Ameriprise Financial and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances.

Past Performance is not a guarantee of future results.

Diversification can help protect against certain investment risks, but does not assure a profit or protect against loss.

Read more articles by Dale W. Van Metre, Ph.D., CRPC®, APMASM