Following a lackluster recovery that began in June 2009, many fear the U.S. is due for another recession, given that the average post-war economic expansion lasted five years. But we’re only in the “fourth or fifth inning of the business cycle,” according to David Rosenberg, who predicts growth in consumer and capital spending – and positive returns for U.S. equities.

“It takes a lot to shock the U.S. economy into a recession,” Rosenberg said. None of the factors that historically triggered a recession – such as a tightening move by the Federal Reserve – are likely over the next two years, according to Rosenberg.

Rosenberg is the chief economist and strategist at Gluskin Sheff, a Toronto-based wealth management firm. Prior to joining the firm in 2009, he was the chief economist at Merrill Lynch. He spoke in Boston on Feb. 27 at a lunch hosted by the Boston Security Analysts Society.

I’ll look at Rosenberg’s bullish U.S. forecast – including why he thinks unemployment data are misunderstood by many – and at his predictions for the equity and bond markets.

Two more years of growth

For Rosenberg, the central question is whether the U.S. economy will relapse into a recession. Once you answer that question, he said, you can debate the direction of the equity and fixed-income markets.

The U.S. economy is incredibly resilient, he said, and he agreed with the adage that a recovery never “dies of old age.” It takes a “negative shock” to start a recession, he said ‑- “and those always have the Fed’s thumbprint on them.”

A severe foreign-based shock is unlikely to derail U.S. growth, he said. Rosenberg noted that our economy and markets had good performance following the Asian crisis in 1997.

The U.S. economy endured the “mother of all fiscal shocks” last year, when fiscal policies raised marginal rates on income, dividends, capital gains and payroll taxes. Layered onto that was the sequestration. Collectively, those factors placed a 1.5% drag on GDP growth, a level that occurred only twice in the post-war period – in the 1960 and 1970 – and both times the U.S. went into a recession.

“It’s probably a miracle that we didn’t have a recession last year,” he said.

Forecasting growth is surprisingly easy, though, according to Rosenberg. “The work is already done,” he said. He relies on the Conference Board leading economic indicators (LEIs) – a “hodgepodge” of 10 data points, including building permits, factory workweeks, durable goods orders, initial jobless claims and the yield curve. When the LEI turns negative, he said, a recession ensues.

Right now, the LEI is increasing 5% year-over-year, he said, and heading upwards.

The steepness of the yield curve is the key metric within the LEI. When the yield curve inverts, Rosenberg said, “you get a recession.” But at a steepness of 260 basis points, the yield curve is “nowhere close to being inverted.”

“There’s no such thing as a sure thing, especially in this business, but the chances of a recession in the next year or two are close to zero,” Rosenberg said.

Rosenberg believes we are only in the fourth or fifth inning of the business cycle. His key point was that consumer spending is about to surge, which typically occurs mid-way through a business cycle.

Housing has peaked, he said, and that is the “quintessential early cycle indicator.” The driver of growth will transition to consumer spending, according to Rosenberg. Housing peaked in 1986, four years before the end of that cycle, and again in 2005, three years before that cycle ended. Housing may still surprise to the upside, Rosenberg said, as the employment picture brightens.

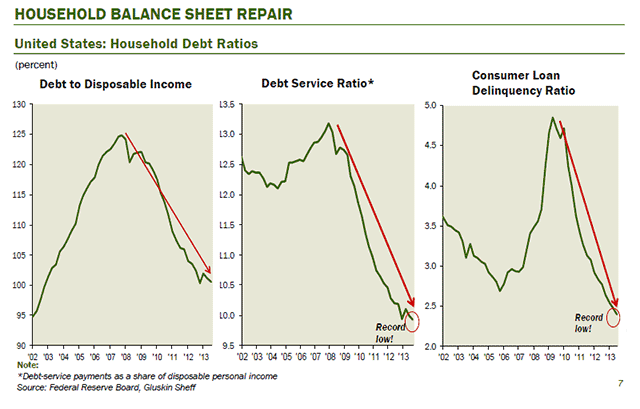

Consumers have de-levered, and that is what drives Rosenberg’s optimism. More than $1 trillion in consumer liabilities have “vanished,” he said. Various ratios, including debt-to-GDP and debt-to-income, have returned to pre-crisis levels. “We’ve come a long way out of this deleveraging cycle,” he said, “and that’s over.”

Behind the unemployment data

Rosenberg challenged those who have attributed the decrease in the U-6 unemployment rate from 10% to 6.6% to a decline in the labor-participation rate.

Government statistics show approximately 90 million people who have left the labor force because they are discouraged, which has driven down the labor-participation rate.

Rosenberg questioned those data, specifically the conditions under which those people are living. He speculated that they may be operating in the barter or underground economy or may have moved in with relatives or parents. He added that demographics should cause the labor pool to shrink, as 1.5 million people will turn 65 each year for the next 15 years.

But his critique of the data centered on the divergence among key indicators. He said there are currently 4 million job openings, signifying a strong demand for labor. One factor deterring job searchers is benefit programs. He cited a “controversial and provocative” Cato Institute study showing that, in 39 states, if one can “tap every state, local and federal benefit program, they can make as much money as an administrative assistant.”

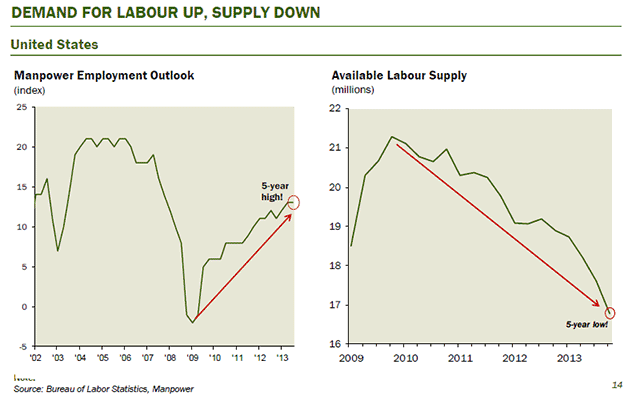

Rosenberg challenged the notion that there is a lot of slack in the labor market. According to BLS data, Rosenberg said those not in the labor force who say they are discouraged was down 14% year-over-year in 2013. Likewise, he said the household survey shows that the number of people who would take a job if offered one is up 10% over that period. The Manpower employment outlook shows the supply of labor was down 15% over that period. The available supply of labor, from the Bureau of Labor Statistics (BLS), is down 15% from a year ago.

With the demand for labor at a five-year high and its supply at a five-year low, Rosenberg said nominal wages will trend higher. He said data from the National Federation of Independent Businesses (NFIB) shows that the number of small businesses intending to increase labor compensation is at its highest point in this business cycle.

An increase in wages will depress profit margins, Rosenberg said, which reflects a reversion to the mean that many analysts have predicted. Rosenberg welcomed this, which he said represented a transfer of income from the part of the economy that has a 40% savings rate (corporations) to that with a 4% savings rate (consumers). That shift would create a “real multiplier impact on spending,” he said, for both consumers and corporations.

The 70% of the economy represented by the consumer will grow, according to Rosenberg, as will another 10% from capital spending. And the remaining 20% – government spending – will benefit from the end of fiscal tightening.

Rosenberg’s forecast for monetary policy and the markets

Rosenberg’s said his bullish forecast for the economy is only half the picture. Liquidity – “the oxygen for financial assets” – needs to be plentiful. “Get the economy right, get the Fed right, and I’ll tell you 90% of the time you will get your market call right,” he said.

The Fed will not tighten until unemployment gets below 6%, he said, which could happen in the second half of next year. It won’t attempt to flatten the yield curve until early 2016. The next recession won’t be until 2017, he said.

Right now, he said conditions are in the “sweet spot,” with easy monetary policy, albeit at a slower rate than last year, and a growing economy.

Given last year’s strong equity-market performance, Rosenberg said he was not surprised by the series of rolling corrections this year. “It probably will continue,” he said, and doesn’t expect a bear market.

Unlike during his days at Merrill Lynch, Rosenberg is no longer obliged to provide point forecasts for the market. But when pressed during the question-and-answer session, he predicted that the S&P would return 5% to 7% in 2014. He said it would be unusual to have a down year given economic and monetary conditions.

His forecast for bonds was far less rosy.

Rosenberg cited an article that appeared in the New York Times on Oct. 27, “Now, Some Fear Economy Needs More Inflation.” He asked, rhetorically, to whom the “some” refers.

“Do you know who it is?” he asked. “The people at the Fed.”

Former Fed chair Ben Bernanke said in his last press conference on Dec. 18 that “we are very committed to making sure that inflation does not stay too low.”

“These guys want inflation,” Rosenberg said. “I’m not saying they want crazy inflation, but they want more inflation than they already have.”

“I want to invest around that.”

The 30-year secular downtrend in long-term interest rates ended in July 2012, he said, when the 10-year note got to 1.43%. There have been – and will be – failed tests of that low, he said.

“But the secular down move in treasury yields is O-V-E-R, it’s done,” he said. “We have a whole new monetary policy, and I would not be betting against the Fed getting what it wants.”

Read more articles by Robert Huebscher