Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. This article originally appeared on the CFA Institute’s Inside Investing blog here.

Retail investors are pouring money into bank-loan funds at a record rate, and the longer term implications are cringe-worthy.

The rationale for investor interest has merit only on the surface. Interest rates are still at historically low levels, and investors are reticent to take on interest-rate risk in the form of longer duration bonds.

Bank loans, also referred to as floating-rate funds, are viewed by many investors as providing a modest source of income while generally free of interest-rate risk. Sounds great, right?

Unfortunately, this narrative is wrong, and the surge in popularity has created an extremely poor risk-reward outlook for holders.

Rise in popularity

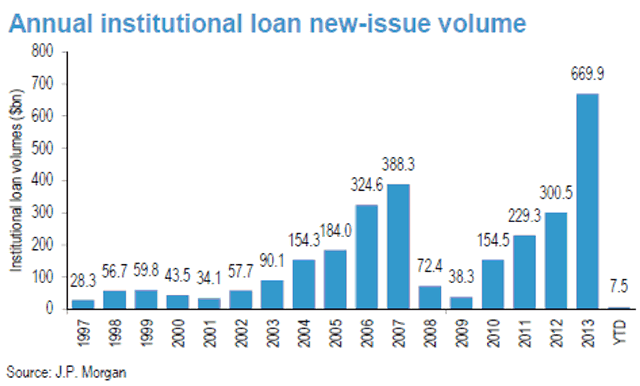

Investors are seeking refuge from potential rises in interest rates by piling in to bank-loan funds. New institutional loan issuance exploded in 2013 to approximately $670 billion, more than two times the amount issued in 2012 and well above pre-crisis levels.

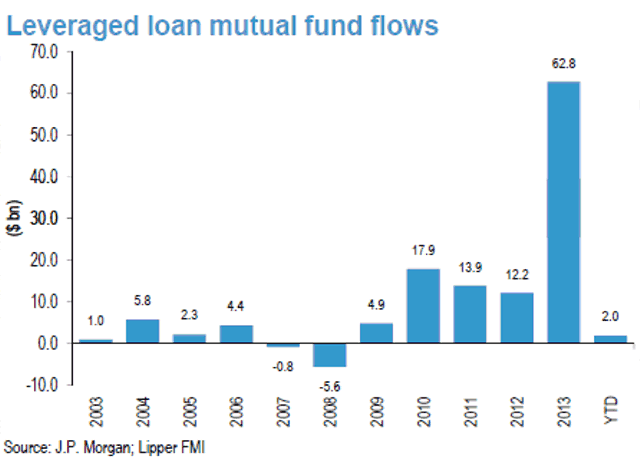

Leveraged-loan mutual-fund flows, as reported by Lipper below, show that retail investors jumped into this asset class in 2013: Inflows increased 5 times from the prior year to approximately $62 billion.

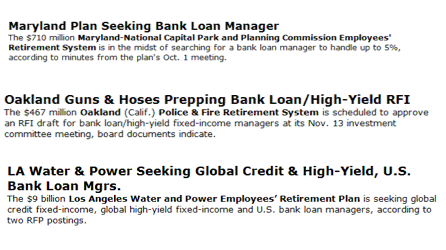

Institutions are equally bullish

The rise in popularity has extended well beyond retail investors, with institutional demand staying strong from pension funds and other money managers. A number of companies are seeking bank-loan managers, as shown below:

High demand causes managers to reach for yield

Given the large amount of inflows to their funds, bank-loan fund managers don’t have a lot of choice as to where they will deploy their capital. Large inflows have forced them to invest in new offerings even if the credit quality is lower.

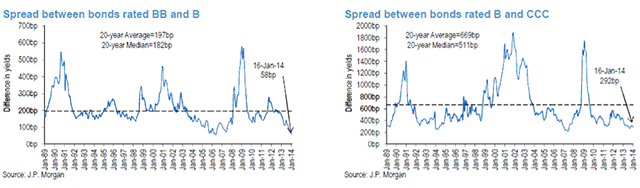

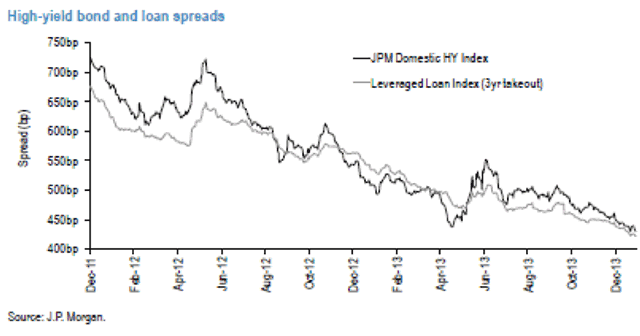

As shown below, the spreads between BB- and B-rated loans as well as between B- and CCC-rated loans are well below historical averages. Investors are willing to go down in credit quality to pick up incremental yield, but are they being properly compensated for this?

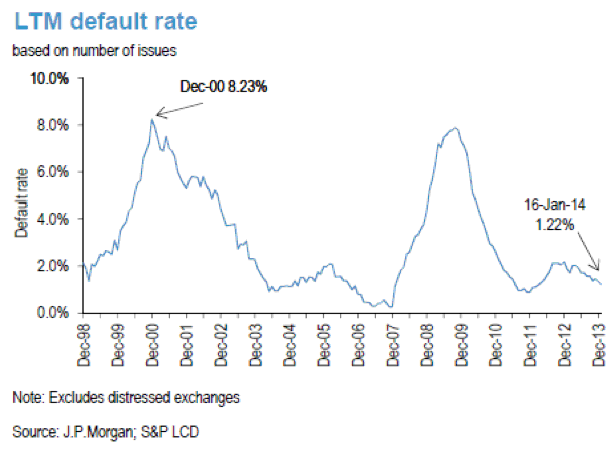

With default rates at near historic lows, investors haven’t had to worry too much about bankruptcies. Now that credit quality is arguably worse, and the compensation for taking on incremental risk is at all-time lows, what will happen to prices and returns when a cyclical downturn occurs? Historically, a large percentage of high-yield bonds and leveraged loans don’t get paid back but are refinanced instead or suffer default.

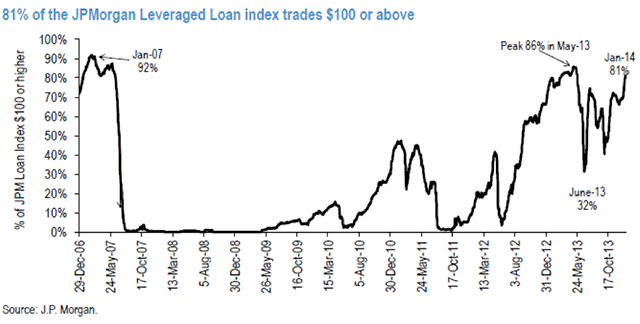

81% of the leveraged-loan index trades at par or higher

Leveraged-loan prices have rallied substantially since the financial crisis. As of this month, 81% of the JPMorgan leveraged-loan index trades at $100 (par) or higher.

This leaves a very negative asymmetric (or negatively convex) return profile for the loan prices. Loan prices are capped on the upside due to call features, while they lack protection on the downside. Simply earning the coupon is fine, but investors need to understand that their upside is capped.

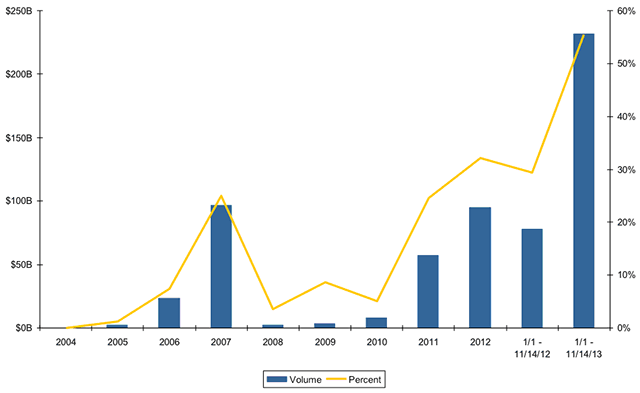

Covenant-lite loan volume exploding

The chart below shows new-issue first-lien covenant-lite loan volume by year. Covenant-lite deals are not bad in and of themselves, but they’re missing a layer of protection that other deals offer. The provisions in these covenants, which allow investors to bring issuers to the negotiating table sooner in cases of trouble, can mean the difference between default and recovery.

The coupon won’t actually float right away

A little-known fact about leveraged loans is that many are priced at what’s called “LIBOR floors.” This means that while the underlying loan might be priced at three-month LIBOR + 300 basis points, it might have a floor of 4.00%. This means that three-month LIBOR, currently at approximately 24 basis points, would need to rise 76 basis points before the coupon adjusts higher.

So if short rates, including the three-month LIBOR, rise 50 basis points, many of these loan coupons will not adjust higher. The result of such a scenario is that the prices would fall, while investors would require a similar margin over three-month LIBOR as they did before rates rose.

Overall, the risk- reward characteristics for leveraged loans are very skewed to the downside. Historically low defaults, the illusion of coupons resetting higher in lock-step with interest rates and modest current income have caused investors to pour money into bank loan funds at a record pace. Unfortunately, the prospective returns given those factors and worsening credit structures leave investors vulnerable to interest-rate and credit risk that they do not realize exists.

David Schawel, CFA, is based in Raleigh Durham NC and works as a fixed-income portfolio manager. His blog is Economic Musings and you can follow him on twitter at @davidschawel.

Read more articles by David Schawel