Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In June 2010, we recommended five strategies for a rising-rate environment, acknowledging that we had no idea when or how abruptly rates would rise. Indeed, rates fell since we wrote that article. But they are on the rise again. After reviewing how our original five strategies performed, we’ll now present our revised recommendations for investing as rates increase.

In our previous article, we offered five strategies that advisors could employ to shield portfolios from rising rates. In some cases, we argued, these five strategies would benefit from rising rates: ultra-short bond funds, international fixed income, floating-rate notes (i.e., bank loans), Treasury inflation-protected securities (TIPS) and real assets.

Overall, these strategies performed admirably between when we recommended them and today. Floating-rate notes, TIPS and our international fixed income recommendations have all outpaced the broader bond market since the article was published. Other recommendations, like gold and commodities, were underperformers, and our ultra-short bond recommendation held its value and paid a modest dividend, as we expected.

There is only one problem: Rates have yet to rise.

In fact, they have fallen (from 3.3% to 2.75% on the 10-year Treasury) since our article was published. Indeed, the bond bull market continued.

As we approach 2014, we are surprised that rates have remained so low for so long. There are various reasons for the low rates: the sluggish economic recovery, the Euro-crisis that monopolized headlines for most of 2010 and 2011 and the aggressively accommodative monetary policy of the Federal Reserve are a few.

The summer stress test

What then can we expect from these asset classes if and when rates eventually increase? And have our recommendations changed?

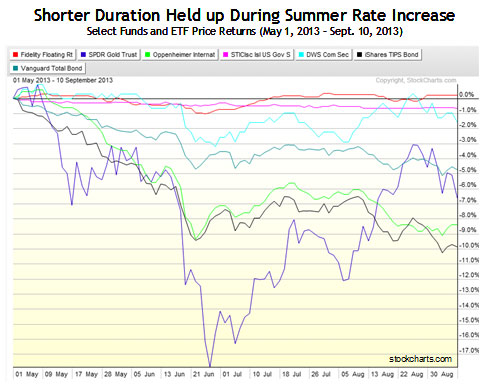

Fortunately, this summer’s “taper tantrum” provided a decent stress test of how these strategies will work in an environment of sustained interest-rate increases.

The chart below shows what the prices of our recommendations and Vanguard Total Bond ETF (a proxy for the bond market) did from May 1 through Sept. 10 of this year — when the yield on the 10-year Treasury moved from 1.66% to 2.96%. It would be unwise to draw broad conclusions that all of the movement in each fund was due to the move in interest rates. Nonetheless, the movement in rates certainly had a meaningful effect on most.

Clearly, short-duration funds like floating-rate notes and ultra-short government bonds held up very well, exhibiting very little volatility or correlation to the move in rates. TIPS had a very high sensitivity to rising rates. With minimal inflation, TIPS offer more risk in a rising-rate environment than most people realize – primarily because of their high duration. Gold and commodities moved, but the causes were a combination of rising rates and the dynamics of the commodities themselves.

What has changed?

While interest rates remain low, many other things have changed since our original article in 2010. First and foremost, asset valuations have changed quite a bit. Credit instruments no longer look like great values. In 2010, floating-rate loans were trading at about 90% of par. Stock valuations were also lower, with the trailing P/E on the S&P 500 near 15. Today, the trailing P/E is closer to 19 and floating-rate notes are trading only slightly below par.

Second, while yield spreads have not changed a lot in the last three years, the absolute yield has. Short-term bonds, floating-rate loans and high-yield bonds generally offered higher yields three years ago. So did stocks.

What to do now?

Given the potential Federal Reserve tapering and higher valuations, here are our revised five strategies for a rising-rate environment:

-

Keep duration short

This is the most obvious strategy for protecting a fixed-income allocation from rising interest rates. The trade-off, of course, is that lower maturity on a bond or bond portfolio generally translates into lower yield. Even so, the 10-year Treasury’s price declined almost 8% during the rate increase this past summer. Stretching for an extra percent of yield by increasing duration hardly makes sense given the potential for duration-related price declines.

While very little in fixed income excites us currently, there are a couple of low-duration asset classes that make sense. We remain committed to floating-rate notes. There is very little stress in credit markets, and corporate balance sheets remain quite healthy compared to history. There is little opportunity for capital appreciation due to the fact that this callable asset class is trading near par, but yield in the 4% range with virtually no duration risk is attractive. For floating-rate exposure, we like the Fidelity Floating Rate High Income FFRHX, which is more conservative, PowerShares Senior Loan BKLN, which is indexed, and Ridgeworth Seix Floating Rate High Income SAMBX , which is more aggressive.

Risk-averse investors will find incremental benefit in allocating some of their cash to high-quality, ultra-short bond funds like Ridgeworth Ultra-Short U.S. Government Bond SIGVX. This fund and funds like it are not as safe as cash, but for those willing to take a small amount of risk, the higher yield (0.66% as of Dec. 5) is worth it over a full market cycle.

-

Don’t constrain yourself

Having a broadly diversified core-bond position as part of your fixed-income portfolio still makes sense, but in a world where interest rates are no longer in secular decline, some changes to the core are appropriate. Though indexing is a very good approach in many asset classes, it presents a problem during a time of rising rates.Consider the Barclay’s Aggregate Bond Index, which measures the performance of the broad investment grade universe in the U.S. In 2007, government bonds made up about 40% of the index. When Freddie Mac and Fannie Mae were put into conservatorship in 2008, the “government backed” number moved closer to 80%. Managers who are tied too tightly to this benchmark and its relatively high Treasury duration will have difficulty should rates rise.

Allowing more leeway to strong, active fixed-income managers makes sense for a portion of the core. An unconstrained manager – one who isn’t tied closely to an interest-rate sensitive benchmark – has the freedom to dramatically lengthen or shorten duration or increase or decrease credit quality. They can get more conservative or more aggressive depending on the market environment.

Of course, as with all active strategies, for value to be added, the managers have to be right. And the way these funds are managed varies greatly. Two funds that we like after performing thorough due diligence are Scout Unconstrained Bond, SUBFX, which is more aggressive, and Goldman Sachs Strategic Income, GSZIX, which is more conservative.

-

Stay diversified

If every bubble, bust, shock and surprise in the history of investing has taught one single lesson, it is to stay diversified. Preparing for rising rates is no exception.

While we have a fair amount of conviction that rates will increase on average in the future, we could be wrong – or, as was the case with our 2010 article, we could be early.

Consider a few extreme cases. Most of us know people who liquidated portfolios into cash near the bottom of the last bear market, only to see it rise rapidly soon after. We all likely know people who lost most of their wealth by piling into tech stocks near their peak in 2000.

What about today? Investors shouldn’t rush out and put all of their money in stocks and floating-rate notes. While that strategy may do just fine for a while, an investor who does this would be trading one risk (interest-rate risk) for other risks (credit risk and business-cycle risk). Should we face a recession, stocks and lower-quality credit would suffer. From peak-to-trough in 2007-2009, stocks were down by more than half, and floating-rate notes fell by more than a third.

Diversification protects us from various risks, of which rising interest rates are only one.

Diversification also makes long-term planning more scientific and measurable than taking concentrated risks, because the range of likely outcomes (i.e., the bell curve and related Monte Carlo simulations) becomes tighter. Concentrated bets have binary outcomes. They either work or they don’t. You might gain 100% or more, or you might lose half or worse. Diversification narrows the likely range of future outcomes by decreasing the probable range of returns and volatility.

Unconstrained bond strategies are preferable to highly constrained bond strategies, but that doesn’t mean that investors should abandon core-bond exposure. We like floating-rate credit better than long-dated Treasury bonds, but investors shouldn’t completely abandon the Treasury market. Investors should overweight and underweight certain asset sub-classes and not make all-or-none choices. All-or-none investing decisions can lead to all-or-none outcomes, something every investor wants to avoid.

Summary

Will tapering of quantitative easing, economic growth or inflation expectations cause interest rates to increase? If so, will the increase be abrupt or measured? If it happens, when will it happen?

We don’t know when rates will rise, but we suspect that it will be sooner rather than later. The U.S. economy is improving, and the unemployment rate that the Fed is so intently watching is coming down. Inflation remains tame. With this mix, the Fed doesn’t face immediate pressure to taper QE or increase its benchmark short-term rate. Eventually, though, QE will wind down and rates will rise.

The strategies above will add value. A below-benchmark duration, a more flexible (i.e., unconstrained) fixed-income approach and some floating-rate exposure will serve as good complements to existing core-bond positions. TIPS and nominal Treasury bonds are very interest-rate sensitive and should make up a smaller part of the fixed-income allocation than has been historically accepted.

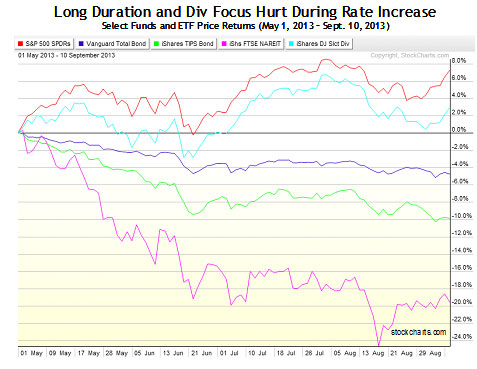

It makes sense to own equities in a low-inflation, stable-growth environment, but equity exposures should not come with too much interest-rate sensitivity. If the stress test of 2013 is any indication, rate-sensitive equities like mortgage REITs and high-payout-ratio stocks may underperform should a rising-interest rate environment take hold.

Stay diversified. There are risks other than rising rates, like equity-market risk, credit risk, regulatory risk, currency risk and longevity risk. A long-term investment plan should find the right risk-and-return mix to meet each investor’s goals.

Kane Cotton, CFA, is chief investment strategist of the Capital Allocation & Management program at Bellatore Financial, Inc. Jonathan Scheid, CFA, is president and chief investment officer of Bellatore Financial, Inc., an innovative turnkey asset management provider in San Jose, CA. More information about Bellatore can be found at www.bellatore.com.

Read more articles by Kane Cotton, CFA and Jonathan Scheid, CFA